配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 本期无新增 - 中国供应商海外项目 · 表 A — 本期无新增 - 供应商档案 · 表 B — 本期无更新 - 锂价历史 · 表 D — 06-09 行已追加(SMM 最新 Date 6 月 8 日,T-1 正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

Muswellbrook Solar Farm & Battery(NSW,135 MW+100 MW/300 MWh):EPC 合同授标 Bouygues/Equans · PV Magazine Australia,2026-06-08

瑞典国际可再生能源开发商 OX2 旗下澳洲首个 IPP 项目 Muswellbrook Solar Farm & Battery 完成 EPC 合同授标,由 Bouygues Construction Australia + Equans Solar & Storage Australia 联合体以交钥匙方式承接全程实施。

规格与背景: - 光伏:135 MW(约 30 万块 PV 面积,覆盖 482 公顷);BESS:100 MW/300 MWh(3 小时) - 选址:NSW 猎人谷 Muswellbrook 煤矿经环境修复后的棕地(Idemitsu Australia / Muswellbrook Coal 前矿区) - 预计年发电约 347 GWh(供数万户家庭) - 竣工目标:2028 年,设计运营寿命 40 年;峰值用工约 200 人 - 融资安排行:MUFG(债务安排行 + 承销行);已签长期混合 PPA(光伏+BESS) - 承包商背景:Bouygues/Equans 此前完成全澳最大太阳能场 Culcairn(440 MW,NSW)及 Goorambat East(250 MW,VIC),具备成熟本地施工资源池

→ 对 PG 的影响:棕地开发+融资安排行 MUFG+长期 PPA 三位一体是当前澳洲大型新能源项目的标准可融资结构;Bouygues/Equans 在 NSW 的 EPC 资源积累说明欧洲系大承包商在澳洲已有显著规模优势,PG 在同区域项目 EPC 招标时需将此类资源作为报价基准对比。

来源:PV Magazine Australia(2026-06-08)

Enervest × Billion Watts JDA:50 MW/200 MWh 分布式 10 站组合(NSW+VIC) · Enervest 官网,2026-06-03

澳洲储能开发商 Enervest(曾签下 Octopus Australia Hanworth BESS、NSW Roadmap Round 5 项目)与台湾 Billion Electric(3027.TW) 旗下 Billion Watts 签署联合开发协议(JDA):

→ 对 PG 的影响:台湾系工业资本(Billion Electric 具备电力电子制造背景)与本地开发商组合的模式正在澳洲分布式 BESS 市场快速复制,sub-5 MW 配电侧 BESS 较大型 BESS 的电网接入路径更短、审批阻力更小;对 PG 旗舰大型项目无直接竞争,但将加剧本地 DNSP 对接资源与 EPC 人力资源的竞争。

来源:Enervest 官网(2026-06-03)

CIS Tender 8(4 GW/16 GWh):截至 06-09 仍在评估,Australian Energy Week 为本月最后主要公告窗口 · ASL/DCCEEW,持续跟踪

ASL 官网截至 06-09 早仍维持「Bids are currently being assessed」。联邦能源部长 Chris Bowen 预计在 Australian Energy Week(06-09~12,墨尔本) 期间发表主旨演讲,是「2026 年 6 月公布」承诺在本月最集中的正式发布机会。Tender 10(NEM 可调度储能,下一批大储招标)亦预计本月开放注册,Tender 8 结果落地后两招标窗口将同步运行。

NSW LTESA Tender 9(12 GWh,≥8h)注册截止倒计时:距今 13 天(06-22 届满)。注册是提交投标的硬性前置条件,错过无法补办,PG 若有 NSW 项目意向须本周内确认内部决策。

→ 对 PG 的影响:Australian Energy Week 是本月 Tender 8 结果最高概率公告窗口,需实时监控 ASL 官网及能源部长演讲公告;Tender 9 注册窗口 13 天倒计时构成本周内部决策硬节点。

今日无新增重大政策动态

本期覆盖窗口内,AEMO、AEMC、AER 均无新规则发布或重大咨询公告。持续跟踪项目:

→ 对 PG 的影响:本周 Australian Energy Week 亦是联邦政策宣示密集窗口,任何针对 CIS Tender 8 之外的新储能政策宣布同样值得实时跟踪。

今日无新增 ≥100 MWh 海外项目公告

SNEC 2026(06-03/05)闭幕后第 4 个工作日,本期信源 / LinkedIn 扫描未见 BNEF 储能 Tier 1 中国厂商(彭博 Tier 1 储能榜 56 家,口径见表 B / Tier 1 名单)发出 ≥100 MWh 新海外项目正式公告。展后合同披露窗口通常延续 2-4 周,预计本周内将有更多披露。

SNEC 整体签约规模参考(EnergyTrend 06-08):SNEC 2026 展会期间,不完全统计储能签约合计超 92.7 GWh,覆盖多家 BNEF Tier 1 储能厂商;其中 CATL、Hithium(已于 Issue 17/18 完整报道)为最大宗,SNEC 后续合同公告将持续追踪。

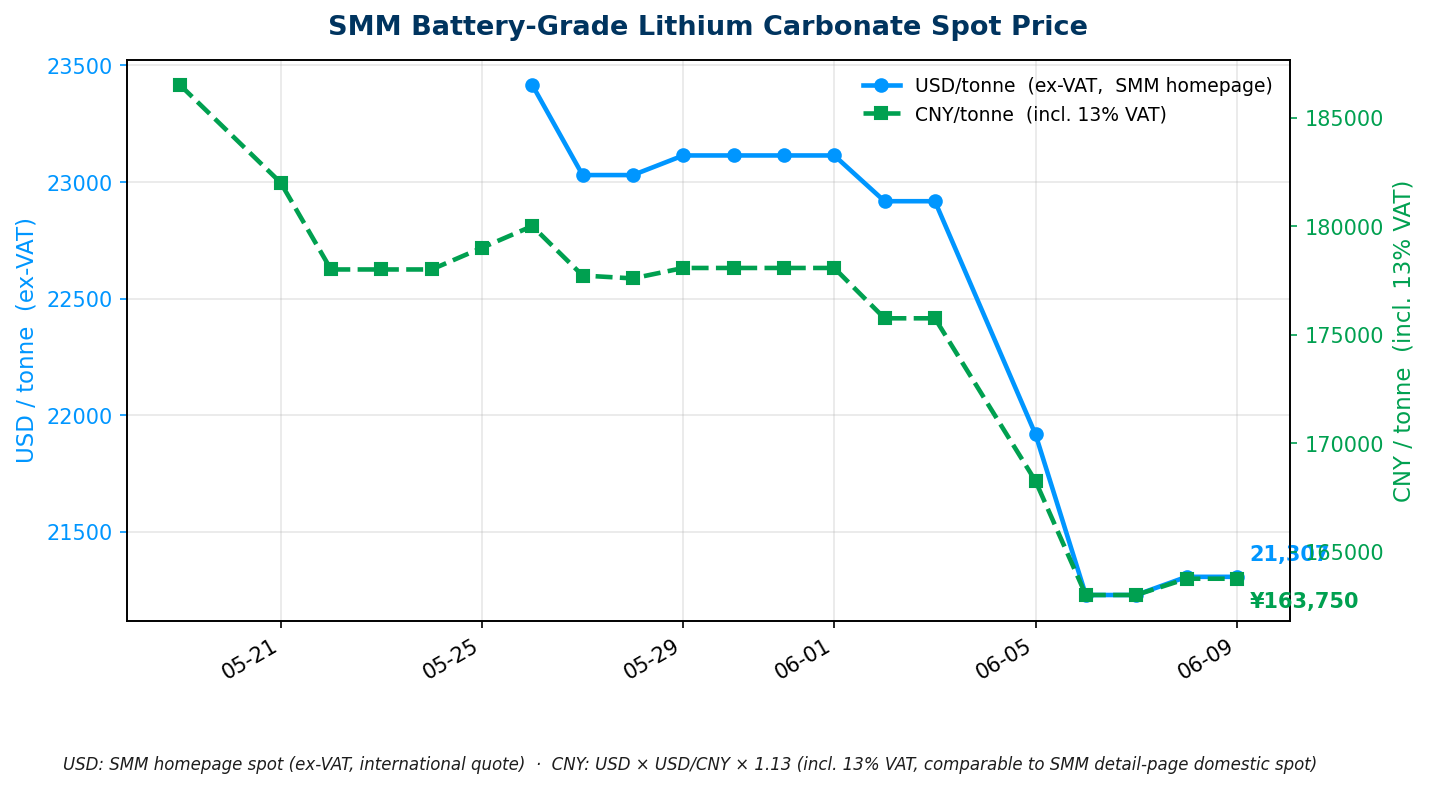

今日价格(口径:2026-06-09 北京时间 07:01 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 21,307.38 / tonne(0,持平) / CNY 163,750 / 吨 | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 8 日(SMM 约 10:10 发当日值,7:00 抓为 T-1 是正常);CNY 含 13% VAT 官方精确均价 |

走势分析:磨底格局延续,本月两大变量未落地

上周(第 23 周)GFEX LC2609 累跌 -8.5%,周一(06-08)现货小幅反弹至 CNY 163,750(+750)后趋于平稳。现货价仍处各机构磨底区间(卓创 CNY 158,000-172,000 / 长江有色 CNY 155,000-165,000)上沿,三重压制延续:①仓单累库(约 55,000-60,000 手);②5 月产量放量(约 62,100 吨,+27.9% MoM);③月初买盘清淡。

本月两大关键变量(观察截止节点)

两项变量本周均无新进展,待 6 月底前关注。

→ 对 PG 的影响:现货磨底格局与供需博弈态势延续,PG 采购框架锁价时点维持「Bald Hill 7 月首产数据落地后、同步关注枧下窝 06-30 申请结果」判断不变。趋势图如上,近一周价格区间 CNY 163,000-163,750,波动收窄。

来源:SMM-Li-LC-001 Avg(metal.com API);完整台账见 活表 D

SVOLT SNEC 2026:6.29 MWh 工具规模容器 + 371Ah CTR 架构,签约 8 GWh · PV Magazine,2026-06-08

SVOLT Energy Storage 在 SNEC 2026 发布全场景储能解决方案,工具规模旗舰为 6.29 MWh 集装箱(371Ah 叠片短刀电芯,单体 1,187 Wh):

C&I 系统:285 kWh 一体机(371Ah 热复合叠片,AI-BMS 可提升运维效率最高 60%,-30°C 至 55°C 工作温度范围)。

→ 对 PG 的影响:SVOLT 6.29 MWh 容器与当前行业 6.25-6.26 MWh 新基准高度吻合,CTR 架构消除模组层降低 BOS 成本;8 GWh 展会签约 + 中东意向合作说明 SVOLT 正积极开拓英语国家市场,是 PG 未来采购的潜在短名单候选。其 371Ah 电芯平台在 C&I 侧已实现 GWh 级交付,工具规模属新品,交付记录待跟踪。

来源:PV Magazine(2026-06-08)

华为 SNEC 2026 发布新构网型组串式 PCS,声称 RTE 97.8% · LinkedIn SNEC 2026 Highlights / Huawei 官方,2026-06-03

华为数字能源在 SNEC 2026 发布下一代 Smart String 构网型(Grid-Forming)PCS 平台,核心技术参数:

背景:AEMO 已要求 2026-10-28 起所有新并网 BESS 具备构网能力;澳洲电网构网型 BESS 需求的政策确定性使该技术参数成为采购规格书的核心条款。

→ 对 PG 的影响:华为 RTE 97.8% 若经独立第三方实测验证,将使同等装机容量的 BESS 全生命周期净发电量提升显著,直接影响 LCOS 计算和 IRR 假设;PG 在 2026-2027 年 RFQ 文件中可将构网型 + RTE ≥97% 作为技术规格门槛,以锁定最优设备并作为银行 lender 技术评估的加分项。

来源:LinkedIn SNEC 2026 Highlights(含 Huawei 97.8% RTE 披露)(2026-06-05)·佐证 Huawei 官方 SNEC 页

Google × Intersect Meitner Energy Center:1 GW+ 风光储同址数据中心正式破土(德州) · Google Blog / Power Magazine,2026-06-04

Alphabet 全资子公司 Intersect Power 与 Google 联合在德州 Panhandle(Gray & Roberts 县)启动建设 Meitner Energy Center,这是继 Haskell 县 Quantum I+II(640 MW+1.3 GWh BESS,2026 年 6 月投运)后第二个 Google-Intersect 能源同址数据中心:

→ 对 PG 的影响:Google-Intersect 模式在德州 GW 级落地,向全球数据中心运营商传达清晰信号:大规模 BESS 是 AI 算力基础设施的必要组成,而非成本项。澳洲 AIDC 容量预测 2030 年从 1.4 GW 增至 3.2 GW,PG 在有条件同址布局的项目中(如邻近大型数据中心的 NSW/VIC BESS 选址),可引用 Google-Intersect 模式构建「AIDC 能源稳定性供应商」的差异化叙事,提升 offtake 谈判吸引力。

来源:Google Blog(2026-06-04)· Power Magazine(2026-06-04)

本期暂缺

2026-06-08 Daily Briefing(Modo Energy)无澳洲/NEM 专项内容(涵盖北美、英国、全球市场动态,无 NEM 专题文章)。

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Supporting live tables (updated daily by this research system): - Australia Projects Supply Chain · Table C — No new entries this issue - China Suppliers Overseas Projects · Table A — No new entries this issue - Supplier Profiles · Table B — No updates this issue - Lithium Price History · Table D — 09 Jun row added (SMM latest Date: 08 Jun, T-1 normal); trend chart refreshed

Full project supply chain BOM: Table C.

Muswellbrook Solar Farm & Battery (NSW, 135 MW+100 MW/300 MWh): EPC Contract Awarded to Bouygues/Equans · PV Magazine Australia, 2026-06-08

OX2's first Australian IPP project, Muswellbrook Solar Farm & Battery, has awarded its EPC contract to a joint venture of Bouygues Construction Australia + Equans Solar & Storage Australia under a turnkey arrangement. OX2 entered Australia as an international renewable energy developer.

Specifications and background: - Solar: 135 MW (~300,000 PV panels, 482 ha); BESS: 100 MW/300 MWh (3-hour) - Site: Former Idemitsu Australia / Muswellbrook Coal brownfield site (previously an operating open-cut coal mine, environmentally rehabilitated) - Projected annual generation: ~347 GWh (tens of thousands of Australian households) - Commissioning target: 2028; 40-year design life; peak workforce ~200 - Debt arranger and underwriter: MUFG; long-term hybrid PPA (solar + BESS) signed - Contractor track record: Bouygues/Equans delivered Australia's largest solar farm to date, Culcairn (440 MW, NSW), and Goorambat East (250 MW, VIC)

→ For PG: Brownfield site + MUFG debt arrangement + long-term PPA is the standard bankable structure for large Australian new energy projects in 2026. Bouygues/Equans' established NSW EPC resource pool sets a cost benchmark PG will face in competitive EPC procurement for projects in the same region.

Source: PV Magazine Australia (2026-06-08)

Enervest × Billion Watts JDA: 50 MW/200 MWh Distributed Portfolio (NSW+VIC) · Enervest official, 2026-06-03

Australian energy developer Enervest has signed a Joint Development Agreement (JDA) with Billion Watts, a subsidiary of Billion Electric Co. (3027.TW), to advance a 50 MW/200 MWh portfolio of sub-5 MW distributed storage assets:

→ For PG: Taiwanese industrial capital (Billion Electric's power electronics background) + local developer model is replicating rapidly in Australian distributed BESS. Sub-5 MW distribution-connected assets face shorter interconnection queues and lower regulatory friction than PG's large-scale projects — no direct competition, but shared EPC labor resources and DNSP relationship bandwidth will tighten.

Source: Enervest official (2026-06-03)

CIS Tender 8 (4 GW/16 GWh): Still Under Assessment; Australian Energy Week Is Final June Window · ASL/DCCEEW, ongoing

ASL website as of 09 Jun morning still shows "Bids are currently being assessed." Energy Minister Chris Bowen is expected to speak at Australian Energy Week (09-12 Jun, Melbourne), representing the last concentrated formal publication opportunity within the government's stated "June" commitment. Tender 10 (NEM Dispatchable, next large-scale BESS tender round) is also expected to open for registration in June — once Tender 8 results land, both tender windows will run concurrently.

NSW LTESA Tender 9 (12 GWh, ≥8h): 13 days to registration deadline (22 Jun). Registration is a hard prerequisite for bidding; missed registrations cannot be remediated. PG must confirm an internal go/no-go decision this week.

→ For PG: Australian Energy Week is the month's highest-probability announcement venue for Tender 8 — monitor ASL website and minister's keynote. NSW Tender 9 registration deadline is a 13-day hard decision node.

No major new policy developments this period

AEMO, AEMC, and AER issued no new rules or major consultation notices within this coverage window. Ongoing tracked items:

→ For PG: Australian Energy Week is also a high-density federal policy announcement window beyond CIS Tender 8 — any new storage-related policy signal from the minister warrants immediate review.

No new ≥100 MWh overseas project announcements this period

Four working days post-SNEC 2026 (03-05 Jun), this period's source/LinkedIn scan surfaced no new formal overseas project announcement meeting the ≥100 MWh threshold from any BNEF Tier 1 storage manufacturer (the 56 China-HQ'd names on Bloomberg's Tier 1 storage list; scope per Table B / Tier 1 list). Post-show contract disclosure cycles typically extend 2-4 weeks after a major exhibition.

SNEC 2026 aggregate signing context (EnergyTrend, 08 Jun): Estimated total SNEC 2026 storage agreements exceeded 92.7 GWh across exhibitors, a new exhibition record. Tier 1 manufacturer post-SNEC announcements will be tracked as they emerge.

Today's Price (collected at 07:01 Beijing Time, 2026-06-09)

| Grade | Latest Price | Scope |

|---|---|---|

| Battery-grade lithium carbonate (SMM) | USD 21,307.38 / tonne (0, flat) / CNY 163,750 / tonne | SMM-Li-LC-001 Avg; SMM latest Date: 08 Jun (SMM publishes at ~10:10 daily; 07:00 capture is T-1 — normal); CNY incl. 13% VAT official average |

Market Commentary: Grinding-Bottom Formation Continues; Two Key June Catalysts Pending

After last week's (Week 23) GFEX LC2609 cumulative decline of -8.5%, Monday's (08 Jun) spot price saw a modest rebound to CNY 163,750 (+750) before stabilizing. Spot price remains at the upper end of institutional grinding-bottom ranges (Zhuochuang: CNY 158,000-172,000; Yangtze Nonferrous: CNY 155,000-165,000), with three structural pressure lines continuing: ① GFEX warrant inventory accumulation (~55,000-60,000 lots); ② May production surge (~62,100 t, +27.9% MoM); ③ Slack spot demand at month start.

Two Key June Catalysts (Observation Deadlines)

Neither catalyst has new development this week; monitoring continues.

→ For PG: Grinding-bottom formation and supply-demand dynamics unchanged. PG procurement timing remains "wait for Bald Hill's July first shipment data, monitor Jianxiawo's 30 Jun application outcome before locking framework contract price." The 7-day price range has narrowed to CNY 163,000-163,750 — volatility compression, not structural direction change.

Source: SMM-Li-LC-001 Avg (metal.com API); complete ledger at Table D

SVOLT SNEC 2026: 6.29 MWh Utility Container + 371 Ah CTR Architecture, 8 GWh Signed · PV Magazine, 2026-06-08

SVOLT Energy Storage launched a comprehensive multi-scenario portfolio at SNEC 2026, with the flagship utility-scale product being a 6.29 MWh container (371 Ah stacked short-blade cells, 1,187 Wh per cell):

C&I system: 285 kWh all-in-one (371 Ah thermal-composite cells, AI-BMS improving O&M efficiency by up to 60%, -30°C to 55°C ambient).

→ For PG: SVOLT's 6.29 MWh container aligns with the emerging 6.25-6.26 MWh industry baseline; CTR architecture reduces CAPEX by eliminating the module layer. 8 GWh of SNEC agreements plus Middle East market intent signals active English-market expansion — SVOLT is a candidate for PG's future procurement shortlist. Track delivery record validation as product is newly launched.

Source: PV Magazine (2026-06-08)

Huawei SNEC 2026: New Grid-Forming String PCS, Claiming 97.8% RTE · LinkedIn SNEC 2026 Highlights / Huawei official, 2026-06-03

Huawei Digital Power launched its next-generation Smart String Grid-Forming (GFM) PCS platform at SNEC 2026:

Background: AEMO mandates grid-forming capability for all newly connected BESS from 28 Oct 2026 — GFM specifications are now procurement requirements, not differentiators.

→ For PG: If Huawei's 97.8% RTE is independently verified, it translates to meaningfully higher lifetime net generation per unit of installed capacity, improving LCOS and IRR calculations. PG's 2026-2027 RFQ documents should explicitly specify GFM capability and RTE ≥97% as technical thresholds — lenders' technical advisers will increasingly reference such benchmarks in due diligence.

Source: LinkedIn SNEC 2026 Highlights (2026-06-05) · Supporting: Huawei official SNEC page

Google × Intersect Meitner Energy Center: 1 GW+ Wind-Solar-Storage Co-Located Data Center Breaks Ground (Texas) · Google Blog / Power Magazine, 2026-06-04

Alphabet subsidiary Intersect Power and Google have commenced construction on the Meitner Energy Center in Gray and Roberts Counties, Texas Panhandle — the second Google-Intersect energy-first co-located data center campus (following Haskell County's Quantum I+II: 640 MW solar + 1.3 GWh BESS, scheduled to begin operations June 2026):

→ For PG: Google-Intersect Meitner at GW-scale in Texas sends an unambiguous signal to global data center operators: large-scale BESS is a required component of AI computing infrastructure, not a cost item. Australia's AIDC capacity is projected to grow from 1.4 GW to 3.2 GW by 2030 (AEMO). For PG projects with potential co-location adjacency (NSW/VIC BESS sites near major data center corridors), the "AI energy stability provider" narrative modeled by Google-Intersect offers a compelling differentiation framework for offtake negotiations.

Source: Google Blog (2026-06-04) · Power Magazine (2026-06-04)

Not available this period

The 08 Jun 2026 Modo Energy Daily Briefing contained no Australia/NEM-specific content (covered North America, UK, and global markets). No new NEM-specific research articles were published in this coverage window.

This research brief is automatically compiled daily by the PGSH internal research system; sources are cited for each item. Project progress, policy developments, price data, and institutional views listed are for internal reference only and do not constitute investment, procurement, or commercial decision advice. If interested in any item or planning to act on it, please open the corresponding source link directly to verify accuracy and timeliness.