类型:增量(信源重核修订版)· 覆盖窗口:2026-06-07 ~ 2026-06-08(基线 2026-06-07)

本期为按「信源纪律 v2.1」重核后的修订版:每条来源链接均经发布前验活、可点开直达原文,关键数字逐条比对原文。核心:CIS Tender 8(4 GW / 16 GWh)截至 06-08 仍在评估,无授标公告;CATL 钠离子储能 2026 年 9 月首批商业交付,全年 GWh 级出货,硬碳负极成本两年减半;CORNEX 楚能 SNEC 签约 12 GWh 框架(东方电气 8 + 正泰 2 + 沃太能源 2);沙特 Saudi Energy 2.5 GW / 12.5 GWh 构网型 BESS 五区商运(BYD 电池、Alfanar EPC、NR Electric 南瑞构网控制 + 2,000 余台 PCS),为全球迄今最大构网型电网侧 BESS 集群;锂价 SMM 06-08 回升至 USD 21,307 / CNY 163,750(含税 +0.46%);Modo 揭示 NEM 新建光伏已 100% 配储、5 月电池收益创 $29k/MW/年 历史新低。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 本期无新增;当前项目库(CIS Tender 8 结果待定) - 中国供应商海外项目 · 表 A — 本期无新增 - 供应商档案 · 表 B — 本期无新增 - 锂价历史 · 表 D — 06-08 行已校正为当日实价(USD 21,307.38 / CNY 163,750,SMM Date 6 月 8 日);趋势图已重画

完整项目供应链 BOM 见 活表 C。

今日无新增项目

CIS Tender 8(4 GW / 16 GWh):截至 06-08 仍在评估 · AEMO Services,招标页 2025-11 更新、持续维护

澳洲 Capacity Investment Scheme Tender 8(NEM Dispatchable)官方招标页截至本期维持「Bids are currently being assessed」状态。投标已于 2026-01-06(AEDT 17:00)截止,评估进入第五个月;官方预期「2026 年 6 月公布」,本月余约 3 周仍属合理窗口。本周未见任何官方或媒体预报性披露。

→ 对 PG 的影响:Tender 8 结果将揭示 16 GWh 纯储能合同的区域分布与成交价格,是 Tender 10 竞价参考的核心校准点,本周内保持高优先级跟踪。

来源:AEMO Services — CIS Tender 8 NEM Dispatchable

NSW LTESA Tender 9(12 GWh,≥8h):注册窗口剩余 14 天 · AEMO Services(NSW Roadmap),招标页 2026-05-19 更新

NSW 长时储能 Tender 9 注册截止日为 2026-06-22,投标截止 2026-07-06;注册为提交投标的硬性前置条件,错过无法补办。官方口径招标规模为 12 GWh 长时储能(最短 8 小时放电),此前部分媒体报道的「12.5 GWh」与官方数字不符,以 AEMO Services 官方页 12 GWh 为准。

→ 对 PG 的影响:若 PG 有 NSW ≥8 小时 BESS 项目管线,本周须完成内部可行性判断并启动注册,错过 06-22 即丧失本轮投标资格。

来源:AEMO Services — NSW Tender 9 Long Duration Storage

CER Q1 2026 季度碳市场报告(06-03):家用电池超 40 万套、可用容量 11.4 GWh · Clean Energy Regulator,2026-06-03

澳洲清洁能源监管机构 CER 于 2026-06-03 发布 2026 年第一季度碳市场报告。截至 2026 年 5 月中旬,全国家用电池累计装机已超 400,000 套、可用容量达 11.4 GWh(含已验证 + 待验证安装);小型光伏 Q1 新增 791 MW,创单季度历史新高。需注意口径:11.4 GWh 为含待验证装机的全国总量(截至 5 月中),其中《更便宜家用电池计划》专项 9 个月累计验证容量为 7.4 GWh,两者不可混用。

背景:联邦《更便宜家用电池计划》已于 2026-05-01 起扩大补贴池,并引入 STC 因子梯度(≤14 kWh 享 100% → 15-28 kWh 60% → 29-50 kWh 15%),每年 1 月、7 月各调降一次以反映成本下降。

→ 对 PG 的影响:分布式储能快速扩张进一步压低日中光伏消纳价格,是 AER Solar Sharer 与 AEMC 最小系统负荷地板价规则变更的政策背景;其聚合调度能力提升将结构性压缩电网级 BESS 的 FCAS 套利空间。

来源:CER 2026 Q1 季度碳市场报告(2026-06-03)· 佐证 CER 新闻稿:Record battery and solar growth

CATL:钠离子储能系统 2026 年 9 月首批商业交付,全年 GWh 级出货 · CarNewsChina,2026-06-05

CATL 国内储能解决方案 CTO 林九标披露迄今最具体的商业化时间表:首批钠离子储能系统将于 2026 年 9 月开始向客户交付,全年出货量将达 GWh 级别。硬碳负极已实现工业级量产,成本由 2024 年约 CNY 6-7 万/吨降至 2026 年 3.5-4 万/吨,中期目标 2.5 万以下。

技术与供应链要点:钠电电芯采用与 CATL 既有 587 Ah LFP 储能电芯相同的壳体尺寸(该平台兼容细节出自 4 月 ESIE 展会披露),系统集成商与 EPC 无需大改产线即可切换。

→ 对 PG 的影响:钠电储能商业化已从「概念」进入「交付倒计时」。平台兼容设计降低供应链切换成本;若 LFP 锂价波动或供给趋紧,钠电可作为 PG 采购框架中的技术对冲选项。澳洲银行方对钠电项目可融资性尚无公开表态,仍需跟踪。

来源:CarNewsChina(2026-06-05)· 平台兼容细节佐证 ESS-News(2026-04-20)

CORNEX 楚能 SNEC 2026 签约 12 GWh 框架协议(东方电气 + 正泰电气 + 沃太能源) · CORNEX 官方 / 碳索储能网,2026-06-03/04

CORNEX(楚能新能源)在 SNEC 2026 展期间官宣三份战略框架合作协议,合计 12 GWh:

| 合作方 | 框架量 | 背景 |

|---|---|---|

| 东方电气(Dongfang Electric,央企) | 8 GWh | 央企 EPC 通道,兼顾国内外大型储能项目 |

| 正泰电气(CHINT) | 2 GWh | 综合电气集团,具备国内外配电 + 储能集成能力 |

| 沃太能源(AlphaESS) | 2 GWh | 具欧洲及亚太分销渠道的储能系统商 |

技术核心:自研 588 Ah 电芯 + CTP 3.0 无模组集成,能量密度 190 Wh/kg、体积能量密度 419 Wh/L,组成 M6 储能容器(约 6.25 MWh/箱,官方英文稿标 6.26 MWh,两版本略有出入),循环次数 >12,000 次、系统效率 96.5%。

→ 对 PG 的影响:CORNEX 以东方电气央企背书提升品牌 bankability,是 PG 采购评估名单中值得关注的新进供应商;东方电气具备国内外 EPC 能力,若搭档 CORNEX 电芯进入澳洲市场,将是供应链整合度较高的选项。

来源:CORNEX 官方(英文)(2026-06-03)· 佐证 碳索储能网(2026-06-04)

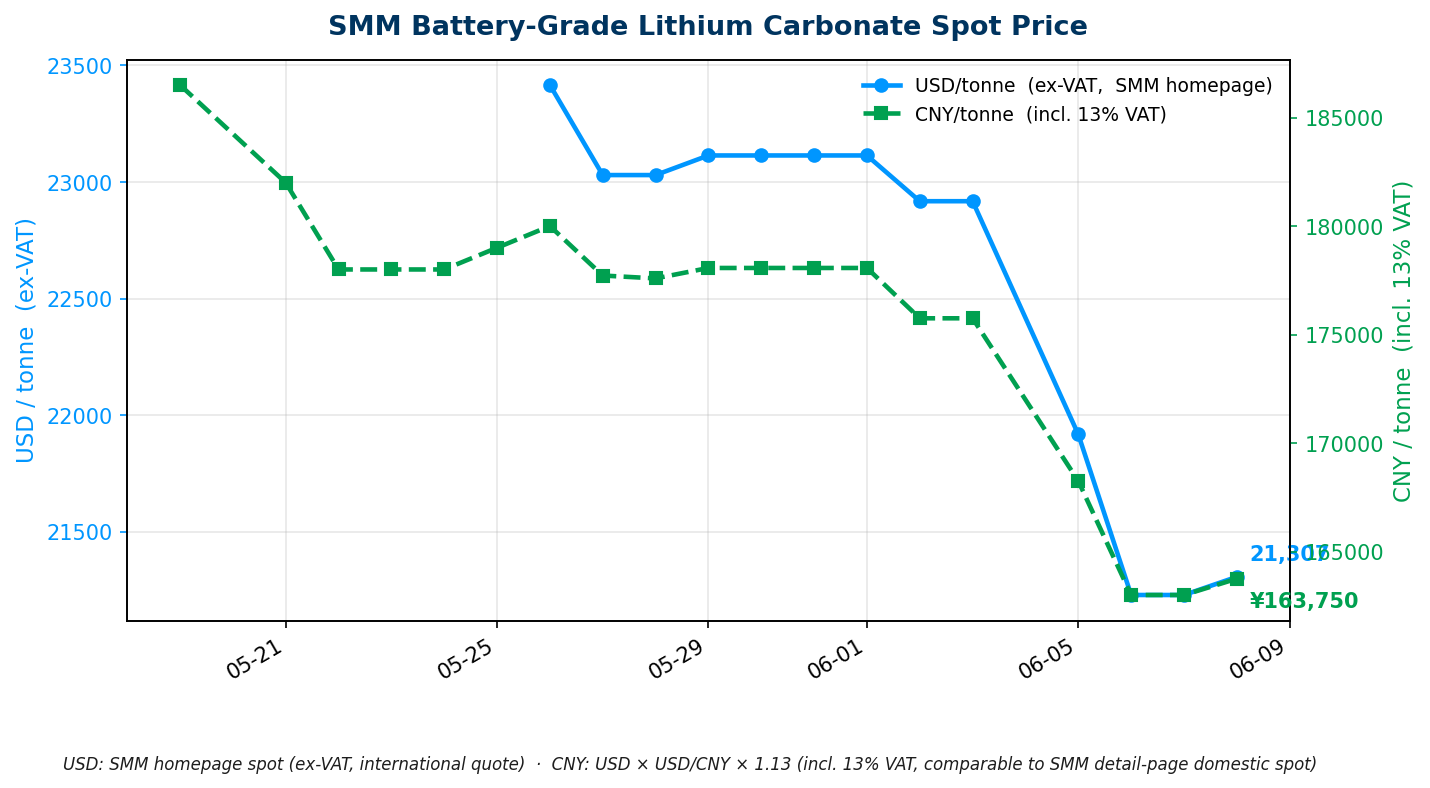

今日价格(口径:2026-06-08 北京时间 14:47 采集,SMM Date 6 月 8 日当日值)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 21,307.38 / tonne(+77.93) / CNY 163,750 / 吨(+750,含税 +0.46%) | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 8 日(周一开市当日值);CNY 含 13% VAT 官方精确均价 |

走势分析:产业备库节奏放缓,短期偏弱,枧下窝申请是最大变量

据华安期货(2026-06-07),生意社数据显示 06-07 现货较期货价差为 -4,300 CNY/吨,期现价差由负值缩小后再度扩大,期货相对现货重新走弱;产业端主动补库意愿明显下降,但锂辉石原料紧张结构未变,下游刚需补库仍在,价格重心短期承压而非崩塌。周一开市现货含税价小幅回升至 CNY 163,750(+750),与上述「承压而非崩塌」判断一致。

矿端关键节点(Q3 观察)

→ 对 PG 的影响:现货含税价小幅回升但仍处磨底区间。枧下窝 06-30 前申请结果与 Bald Hill 7 月实物到货构成双催化剂。PG 采购框架锁价时点维持「7 月首产数据落地后、同步关注枧下窝 06-30 窗口」判断不变。

来源:华安期货(2026-06-07);MinRes Bald Hill 复产公告;完整台账见 活表 D

沙特 Saudi Energy 2.5 GW / 12.5 GWh 构网型 BESS 五区全面商运 — 全球最大 GFM 集群 · MEED / Saudi Gulf Projects / NR Electric,2026-06-04/05

沙特 Saudi Energy(前 Saudi Electricity Company)宣布完成全球迄今规模最大的构网型(Grid-Forming)电网侧 BESS 集群全面并网商运,总容量 2.5 GW / 12.5 GWh,横跨 Riyadh、Rabigh、Dawadmi、Al Jouf、Qassim 五个电网区域。

关键规格与供应链: - 电池供应商:BYD Energy Storage(MC Cube-T 电芯);完成后 BYD 在沙特累计部署达约 15.1 GWh(含此前已交付的 2.6 GWh 项目) - EPC:Alfanar Projects(沙特本土大型能源建设企业) - 构网型控制技术:NR Electric(南瑞)提供构网控制方案与 2,000 余台 PCS - 这是本项目在大规模电网层面实现构网服务的技术核心 - 里程碑:所有网侧充放电测试于 2026-05-27 全部完成;项目合同于 2025 年 1 月签署

→ 对 PG 的影响:沙特 2.5 GW 案例在工程可交付性层面进一步弱化了「GFM BESS 仅适用百 MW 级」的疑虑,BYD 在大规模构网项目的供货能力已有旗舰级实证,NR Electric(南瑞)的构网控制 + PCS 集成能力亦获大规模验证。结合 AEMO 自 2026-10-28 起强制新并网 BESS 具备构网能力,该案例可为 PG 项目在监管文件与银行尽调中提供有力的技术可行性佐证。

来源:MEED(2026-06-05)· Saudi Gulf Projects(2026-06-04)· 构网控制角色据 NR Electric 官方

Ingeteam 发布 9.1 MW 模块化构网型储能平台,构网作标准配置 · ESS-News,2026-06-04

西班牙 Ingeteam 于 6 月初发布 INGECON SUN STORAGE FSK M Series 模块化储能平台,单机最大充放电功率 9.1 MW,将构网型(Grid-Forming)功能作为标准配置(无需额外外部设备),支持 2 至 12 小时放电时长。这是构网型 PCS 从「选配功能」走向产品线「标准件」的又一例证。

→ 对 PG 的影响:AEMO 自 2026-10-28 起强制要求新并网 BESS 具备构网能力,而头部 PCS 供应商已将 GFM 标准化进产品线。PG 新项目采购规格应明确 GFM 要求,否则将错失系统强度服务资格及相关收益。

来源:ESS-News(2026-06-04)

NEM 光伏建设全面混合化:每一个新承诺项目都配储 · Modo Energy,2026-06-05

Modo Energy 拆解 NEM 光伏建设管线发现一个结构性转折:2027-28 年所有已承诺(committed)光伏项目均为光储混合,独立光伏已退出新建管线。

关键数据

| 指标 | 数值 |

|---|---|

| 当前运营光伏中独立占比 | 95%(含调试项目降至 88%,正随配储与改造下降) |

| 独立光伏运营峰值 | 2025 年达 12.5 GW,此后见顶回落 |

| 2027 年混合光伏并网 | 3.3 GW |

| 储能占已承诺 + 预期管线(按 MW) | 67%(公开 announced 阶段 73%) |

| 近三年 BESS 调试速度 | 为公用事业级光伏的 2.3 倍;2026 年至今升至 4.3 倍 |

| 光伏 LCOE vs 单位 MWh 收益(近三年) | 成本降 14%,但单位 MWh 实现收益降 71% |

首批 DC 耦合混合项目 2027 年到来:Goulburn River(NSW,588 MW 光伏)、Fulham(VIC,80 MW)。Modo 预测光伏时段电价已触底,南澳、维州率先回升(电池吸纳日中过剩 + 煤退减少基荷 + 数据中心拉升各时段需求);昆州因配储较慢、煤电更多在线,回升最弱。

→ 对 PG 的影响:独立光伏在 NEM 已无新建可行性,光储混合是唯一可融资模式 - 这从市场结构层面验证了 PG 的光储 / 共址布局方向。混合化亦提升单一并网点价值(抬升 MLF、削减弃电、支撑 PPA firming),是 PG 评估光储一体项目时的核心逻辑。耦合方式(AC vs DC)与光储配比将成为新的投资决策变量。

来源:Modo Energy(2026-06-05)

5 月 NEM 电池收益创历史新低:竞价未跟上日内价格形态变化 · Modo Energy,2026-06-03

Modo Energy 数据显示,5 月 NEM 电网级电池月均收益降至 $29k/MW/年,较 4 月再降 45%,为 2022 年 7 月该指数设立以来最低。

结构与机制

→ 对 PG 的影响:NEM 无集中容量市场,PG 资产全生命周期承受纯 merchant 暴露;融资 IRR 假设需建立在「煤退后价差回升」的长期叙事,而非近期低谷月度数据。并网时间窗口亦关键 - 在 FCAS 与价差尚未完全饱和的市期并网,收益显著优于晚两年并网。

来源:Modo Energy(2026-06-03)

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental (source-reverified revision) · Coverage window: 2026-06-07 ~ 2026-06-08 (baseline 2026-06-07)

This issue is a revision re-verified under "Source Discipline v2.1": every source link has been liveness-checked before sending and resolves directly to the original article, with key figures cross-checked line by line. Highlights: CIS Tender 8 (4 GW / 16 GWh) still under assessment as of 06-08, no award announced; CATL sodium-ion storage first commercial deliveries in September 2026, GWh-level shipments for the year, hard-carbon anode cost halved in two years; CORNEX signs 12 GWh framework at SNEC (Dongfang Electric 8 + CHINT 2 + AlphaESS 2); Saudi Energy's 2.5 GW / 12.5 GWh grid-forming BESS enters commercial operation across five regions (BYD cells, Alfanar EPC, NR Electric grid-forming control + 2,000+ PCS units), the world's largest grid-side grid-forming BESS cluster to date; lithium SMM rebounds 06-08 to USD 21,307 / CNY 163,750 (+0.46% incl. VAT); Modo shows 100% of new NEM solar builds are now paired with storage, and May battery revenues hit a record low of $29k/MW/year.

Companion living tables (continuously accumulated, updated daily): - Australia Project Supply Chain · Table C — no additions this issue (CIS Tender 8 result pending) - China Suppliers Overseas Projects · Table A — no additions this issue - Supplier Profiles · Table B — no additions this issue - Lithium Price History · Table D — 06-08 row corrected to same-day actual (USD 21,307.38 / CNY 163,750, SMM Date June 8); trend chart redrawn

Full project supply-chain BOM in Table C.

No new projects today

CIS Tender 8 (4 GW / 16 GWh): still under assessment as of 06-08 · AEMO Services, page updated 2025-11, continuously maintained

Australia's Capacity Investment Scheme Tender 8 (NEM Dispatchable) official tender page still reads "Bids are currently being assessed" as of this issue. Bids closed 2026-01-06 (17:00 AEDT); assessment is now in its fifth month, and the official expectation of "announcement in June 2026" remains plausible with ~3 weeks left. No official or media pre-announcement leaks were seen this week.

→ For PG: the Tender 8 result will reveal the regional distribution and clearing prices of 16 GWh of standalone storage contracts, a core calibration point for Tender 10 bidding. Keep at high-priority tracking this week.

Source: AEMO Services — CIS Tender 8 NEM Dispatchable

NSW LTESA Tender 9 (12 GWh, ≥8h): 14 days left in registration window · AEMO Services (NSW Roadmap), page updated 2026-05-19

NSW long-duration storage Tender 9 registration closes 2026-06-22, with bids due 2026-07-06; registration is a hard prerequisite for bidding with no late entry. The official tender size is 12 GWh of long-duration storage (minimum 8-hour discharge); some media reports of "12.5 GWh" do not match the official figure — use AEMO Services' official 12 GWh.

→ For PG: if PG has a NSW ≥8-hour BESS pipeline, internal feasibility must be settled and registration started this week; missing 06-22 forfeits eligibility for this round.

Source: AEMO Services — NSW Tender 9 Long Duration Storage

CER Q1 2026 Quarterly Carbon Market Report (06-03): home batteries top 400,000 units, 11.4 GWh usable capacity · Clean Energy Regulator, 2026-06-03

Australia's Clean Energy Regulator released its Q1 2026 Quarterly Carbon Market Report on 2026-06-03. As of mid-May 2026, the national home-battery fleet exceeds 400,000 units with 11.4 GWh of usable capacity (validated + pending installs); small-scale solar added 791 MW in Q1, a single-quarter record. Note the definitions: 11.4 GWh is the national total including pending installs (as of mid-May), while the Cheaper Home Batteries Program's own 9-month validated capacity is 7.4 GWh — the two should not be conflated.

Background: the federal Cheaper Home Batteries Program expanded its subsidy pool from 2026-05-01 and introduced a tiered STC factor (≤14 kWh at 100% → 15-28 kWh at 60% → 29-50 kWh at 15%), stepping down each January and July to reflect falling costs.

→ For PG: rapid distributed-storage growth further depresses midday solar-absorption prices and is the policy backdrop for the AER Solar Sharer and AEMC minimum-system-load floor-price changes; rising aggregated dispatch capability will structurally compress grid-scale BESS FCAS arbitrage room.

Source: CER 2026 Q1 Quarterly Carbon Market Report (2026-06-03) · corroborated by CER media release: Record battery and solar growth

Australian projects in Table C; non-Australian projects in Table A.

CATL: sodium-ion storage systems first commercial deliveries September 2026, GWh-level shipments for the year · CarNewsChina, 2026-06-05

CATL domestic storage solutions CTO Lin Jiubiao disclosed the most concrete commercialization timeline to date: the first sodium-ion storage systems will begin shipping to customers in September 2026, with full-year shipments reaching GWh level. Hard-carbon anode is now in industrial-scale mass production, with cost falling from ~CNY 60-70k/tonne in 2024 to 35-40k/tonne in 2026, targeting below 25k mid-term.

Technical/supply-chain note: the sodium cell uses the same enclosure dimensions as CATL's existing 587 Ah LFP storage cell (this platform-compatibility detail came from the April ESIE expo), so integrators and EPCs can switch without major line retooling.

→ For PG: sodium-ion storage commercialization has moved from "concept" to "delivery countdown." Platform compatibility lowers supply-chain switching cost; if LFP lithium prices swing or supply tightens, sodium can serve as a technology hedge in PG's procurement framework. Australian lenders have not publicly commented on sodium project bankability — keep tracking.

Source: CarNewsChina (2026-06-05) · platform-compatibility detail corroborated by ESS-News (2026-04-20)

CORNEX signs 12 GWh framework agreements at SNEC 2026 (Dongfang Electric + CHINT + AlphaESS) · CORNEX official / TanSuo ESS, 2026-06-03/04

CORNEX announced three strategic framework agreements during SNEC 2026, totaling 12 GWh:

| Partner | Framework volume | Background |

|---|---|---|

| Dongfang Electric (central SOE) | 8 GWh | Central-SOE EPC channel, covering large domestic and overseas storage projects |

| CHINT | 2 GWh | Integrated electrical group with domestic/overseas distribution + storage integration |

| AlphaESS | 2 GWh | Storage system maker with European and APAC distribution channels |

Technical core: in-house 588 Ah cell + CTP 3.0 module-free integration, 190 Wh/kg gravimetric and 419 Wh/L volumetric energy density, forming the M6 storage container (~6.25 MWh/unit; the official English release states 6.26 MWh — a minor discrepancy between versions), >12,000 cycles, 96.5% system efficiency.

→ For PG: CORNEX's central-SOE backing via Dongfang Electric materially lifts brand bankability, making it a new supplier worth watching on PG's procurement shortlist; Dongfang Electric's domestic/overseas EPC capability means a CORNEX-cell + Dongfang-EPC pairing entering Australia would be a highly integrated supply-chain option.

Source: CORNEX official (EN) (2026-06-03) · corroborated by TanSuo ESS (2026-06-04)

Today's price (basis: 2026-06-08, collected 14:47 Beijing time, SMM Date June 8 same-day value)

| Product | Latest | Basis |

|---|---|---|

| Battery-Grade Lithium Carbonate (SMM) | USD 21,307.38 / tonne (+77.93) / CNY 163,750 / tonne (+750, +0.46% incl. VAT) | SMM-Li-LC-001 Avg; SMM latest Date June 8 (Monday-open same-day value); CNY is the official precise average incl. 13% VAT |

Trend analysis: industry restocking slows, near-term weakness, Jianxiawo application the biggest variable

Per Huaan Futures (2026-06-07), SunSirs data show a 06-07 spot-vs-futures spread of -4,300 CNY/tonne; the futures-spot spread, after narrowing from negative, has re-widened, with futures weakening again relative to spot. Active restocking intent on the industry side has clearly fallen, but the spodumene feedstock tightness is unchanged and downstream rigid-demand restocking continues, so the price center is under near-term pressure rather than collapsing. The Monday-open spot price (incl. VAT) rebounded modestly to CNY 163,750 (+750), consistent with the "pressure, not collapse" read.

Mine-side key milestones (Q3 watch)

→ For PG: the spot price (incl. VAT) rebounded modestly but remains in a basing range. The Jianxiawo pre-06-30 application outcome and Bald Hill's July physical delivery form a twin catalyst. PG's procurement price-lock timing maintains the "after July first-output data, while watching the Jianxiawo 06-30 window" view.

Source: Huaan Futures (2026-06-07); MinRes Bald Hill restart announcement; full ledger in Table D

Saudi Energy's 2.5 GW / 12.5 GWh grid-forming BESS fully live across five regions — world's largest GFM cluster · MEED / Saudi Gulf Projects / NR Electric, 2026-06-04/05

Saudi Energy (formerly Saudi Electricity Company) announced the full grid-tied commercial operation of the world's largest grid-forming (GFM) grid-side BESS cluster to date, totaling 2.5 GW / 12.5 GWh, spanning the five grid regions of Riyadh, Rabigh, Dawadmi, Al Jouf and Qassim.

Key specs and supply chain: - Battery supplier: BYD Energy Storage (MC Cube-T cells); on completion, BYD's cumulative Saudi deployment reaches ~15.1 GWh (incl. a previously delivered 2.6 GWh project) - EPC: Alfanar Projects (a major Saudi domestic energy-construction firm) - Grid-forming control technology: NR Electric provides the grid-forming control solution and 2,000+ PCS units - the technical core enabling grid-forming services at large grid scale - Milestones: all grid-tied charge/discharge testing completed 2026-05-27; project contract signed January 2025

→ For PG: the Saudi 2.5 GW case further weakens the notion that "GFM BESS only suits the hundred-MW scale" on engineering-deliverability grounds, providing flagship-grade proof of BYD's supply capability in large GFM projects and large-scale validation of NR Electric's grid-forming control + PCS integration. Combined with AEMO's mandate (from 2026-10-28) that new grid-connected BESS be grid-forming-capable, this case offers strong technical-feasibility support in PG's regulatory filings and lender due diligence.

Source: MEED (2026-06-05) · Saudi Gulf Projects (2026-06-04) · grid-forming-control role per NR Electric official

Ingeteam launches 9.1 MW modular grid-forming storage platform, grid-forming as standard · ESS-News, 2026-06-04

Spain's Ingeteam launched the INGECON SUN STORAGE FSK M Series modular storage platform in early June, with a maximum per-unit charge/discharge power of 9.1 MW, grid-forming (GFM) functionality as standard (no additional external equipment required), supporting 2 to 12 hours of discharge duration. This is another example of grid-forming PCS moving from an "optional feature" to a product-line "standard part."

→ For PG: AEMO requires new grid-connected BESS to be grid-forming-capable from 2026-10-28, and leading PCS suppliers have standardized GFM into their product lines. PG's new-project procurement specs should explicitly require GFM, or risk forfeiting system-strength service eligibility and related revenue.

Source: ESS-News (2026-06-04)

NEM solar build-out goes fully hybrid: every new committed project is paired with storage · Modo Energy, 2026-06-05

Modo Energy's breakdown of the NEM solar build pipeline reveals a structural turning point: every committed solar project for 2027-28 is a solar-plus-storage hybrid, and standalone solar has exited the new-build pipeline.

Key data

| Metric | Value |

|---|---|

| Standalone share of operating solar | 95% (88% incl. commissioning; falling as pairing and retrofits come online) |

| Standalone operating peak | 12.5 GW in 2025, declining since |

| Hybrid solar online in 2027 | 3.3 GW |

| Storage share of committed + anticipated pipeline (by MW) | 67% (73% at publicly announced stage) |

| BESS commissioning pace (3-yr) | 2.3× utility-scale solar; 4.3× in 2026 to date |

| Solar LCOE vs revenue per MWh (3-yr) | cost down 14%, but realized revenue per MWh down 71% |

The first DC-coupled hybrids arrive in 2027: Goulburn River (NSW, 588 MW solar) and Fulham (VIC, 80 MW). Modo forecasts solar-hour prices have bottomed, with South Australia and Victoria recovering first (batteries absorbing midday surplus + coal retirements cutting baseload + data-center growth lifting all-hours demand); Queensland recovers least, given slower storage build-out and more coal staying online.

→ For PG: standalone solar is no longer viable for new build in the NEM, and solar-plus-storage hybrid is the only bankable model - validating PG's hybrid / co-location direction at the market-structure level. Hybridization also raises the value of a single grid connection (lifting MLFs, cutting curtailment, supporting PPA firming), a core rationale for PG's solar-plus-storage project assessments. Coupling type (AC vs DC) and solar-to-storage ratio become new investment-decision variables.

Source: Modo Energy (2026-06-05)

May NEM battery revenues hit record low: bidding missed the shift in daily price shape · Modo Energy, 2026-06-03

Modo Energy data show May NEM grid-scale battery monthly revenue fell to $29k/MW/year, down another 45% on April, the lowest since the index began in July 2022.

Structure and mechanics

→ For PG: the NEM has no centralized capacity market, so PG assets bear full-life merchant exposure; financing IRR assumptions must rest on the long-run "post-coal spread recovery" narrative rather than recent trough months. Connection timing also matters - connecting while FCAS and spreads are not yet fully saturated yields materially better revenue than connecting two years later.

Source: Modo Energy (2026-06-03)

This brief is compiled automatically each day by PGSH's internal research system, with sources annotated for each item. Project progress, policy developments, price data, and institutional views are for internal reference only and do not constitute investment, procurement, or business-decision advice. If you are interested in any item or intend to act on it, please open the corresponding source link directly to verify the accuracy and timeliness of the information.