配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 本期新增 1 条:Edify Energy × CATL QLD 2,400 MWh - 中国供应商海外项目 · 表 A — 本期新增 1 条:Merus Power × CATL 北欧 3 GWh 框架 - 供应商档案 · 表 B — 本期更新 CATL 行(Edify QLD + 北欧框架) - 锂价历史 · 表 D — 06-10 行已追加(SMM 最新 Date 6 月 9 日,T-1 正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

Edify Energy × CATL:QLD Smoky Creek + Guthrie's Gap 2,400 MWh 供货合同(06-09) · Energy-Storage.news / RenewablesNow,2026-06-09

Edify Energy(股东 La Caisse,加拿大机构投资者)宣布,其昆士兰州两座混合光储项目已完成 CATL 供货合同签署,两项目各独立运营、互为参照。

核心规格与供应链: - BESS:600 MW / 2,400 MWh(各 300 MW / 1,200 MWh,3 小时);配套 720 MWp PV;选址 QLD Banana Shire,Biloela 以北约 40 km - CATL:供应 LFP 电芯(含 grid-forming inverter + reverse DC-coupled hybrid 架构) - EPC:DT Infrastructure(马来西亚建筑商 Gamuda 的澳洲子公司)交钥匙承建 - 电网接入:Powerlink 275 kV 骨干网,新建配套变电站 - 收益结构:Rio Tinto 20 年混合服务协议(购买 90% 电力及储能容量)+ CIS 合同双层保障 - 融资状态:14 家国内外银行联合融资,已于 2026 年 5 月关闭;目标 COD 2028

背景:Edify Energy 此前在 QLD(Bulgana 350 MW,SA)有丰富的储能开发运营记录,本次双项目打包以单一 EPC 和供应链方案落地,融资结构(工业大用户 PPA + CIS)是当前澳洲大型混合储能可融资的标准模板之一。

→ 对 PG 的影响:CATL 在澳洲单次公告供货量达 2,400 MWh,是迄今 CATL 在澳单笔最大量,进一步坐实其澳洲市场供应商头部地位。Edify 的「Rio Tinto 20 年 PPA + CIS」结构验证了工业大用户长期合约与政府底托共存的融资可行性,PG 评估 QLD / NSW 项目时可引为同期参照。DT Infrastructure(Gamuda 系)进入大型混合项目 EPC,是继 INTEC × Gotion 之后澳洲 EPC 市场的新力量。

来源:Energy-Storage.news(2026-06-09)· 佐证 RenewablesNow(2026-06-09)

Eku Energy Griffith BESS(NSW Yoogali,100 MW / 1,000 MWh):提交联邦 EPBC 审查(06-09) · Energy-Storage.news,2026-06-09

Eku Energy(Macquarie Asset Management + BCI)将 Griffith BESS 方案从原 LTESA 中标配置(100 MW / 800 MWh,8 小时)升级后,正式向联邦提交 EPBC 审批,是 NSW 乃至 NEM 已进入联邦审批流程中、时长最长的独立 BESS 项目之一。

规格与进展节点: - 100 MW / 1,000 MWh(10 小时);选址 NSW Yoogali(Griffith LGA),占地 9.33 公顷 - 较原 LTESA 批准版扩建 +200 MWh,扩至 10 小时——超过 NSW 与 SA 要求的 8 小时最低门槛 - 电网接入:132 kV 地下电缆接入 Transgrid Griffith 变电站;配套拟建 15 MW Yoogali 太阳能 PV 共址,降低并网 BOS 成本 - LTESA 支撑:NSW Electricity Infrastructure Roadmap 首批 8 小时储能合约之一(2023 年授标,最长 14 年期限),扩容后合约体量上升 - EPBC 提交标志着该项目完成州级开发审批(NSW IPC)和电网接入协商,进入联邦环评最后一道程序;COD 目标 2028

背景:Eku Energy 全球目标为 2028 年前部署 9 GWh 储能;Griffith 若 EPBC 快速通关(同类项目经验:19 天),融资关闭可于 EPBC 批准后数月内完成,2027 年初开工可期。

→ 对 PG 的影响:Eku 率先将 10 小时长时储能推入联邦审批程序,对 NSW LDES 时长竞争态势形成参照。NSW LTESA Tender Round 9(12 GWh,≥8h)注册截止 06-22(12 天倒计时),PG 若有 NSW 长时储能管线项目,本周仍须完成内部决策确认注册资格。

来源:Energy-Storage.news(2026-06-09)

CIS Tender 8(4 GW / 16 GWh NEM Dispatchable):AEW Day 1(06-10)进行中,暂无授标公告 · ASL 官网 / 媒体综合,持续跟踪

Australian Energy Week 2026(06-09~12,墨尔本)第一主会议日(06-10)正在进行。联邦能源部长 Chris Bowen 本周在德国波恩参加 UNFCCC 气候谈判,能源政策重大宣示最可能推至 Energy Policy Forum(06-12) 或部长归国后。今日会场确认出席的主要发言嘉宾为 AEMO CEO Daniel Westerman、维州能源部长 Lily D'Ambrosio、Transgrid CEO Brett Redman。ASL 官网 Tender 8 状态截至本期维持「Bids are currently being assessed」,暂无授标。

NSW LTESA Tender 9 注册截止倒计时:距今 12 天(06-22 届满)。注册为提交投标的硬性前置条件,错过无法补办。

→ 对 PG 的影响:06-12 Energy Policy Forum 是本月 Tender 8 结果最后集中曝光窗口;Tender 9 注册窗口 12 天倒计时构成本周内部决策硬节点。

今日无新增重大政策动态

本期覆盖窗口内,AEMO、AEMC、AER 均无新规则终裁或重大咨询公告。Australian Energy Week(06-10 至 06-12)为本周政策宣示的集中窗口,今日主会议现场暂无联邦级政策宣布。

持续跟踪项目:

→ 对 PG 的影响:建议今晚跟踪 RenewEconomy 及 AEW 官方媒体报道,06-11(AEW Day 2)至 06-12(Energy Policy Forum)是本周政策信息密度最高的窗口。

CATL × Merus Power(芬兰):3 GWh 北欧 BESS 战略合作框架(06-03) · Merus Power 官方 / RenewablesNow,2026-06-03

芬兰上市电力电子公司 Merus Power(HEL:MERUS)与 CATL 签署战略合作协议,将在既有三年合作关系(累计交付约 500 MWh)基础上升级规模,目标在北欧市场交付约 3 GWh BESS 解决方案。

供应链分工: - CATL:提供电芯(LFP 储能电芯,型号未单独披露) - Merus Power:负责 power electronics、grid inverter 技术、网络安全控制与保护系统,以及本地化系统集成与交付 - 市场:芬兰为主,辐射整个北欧(北欧储能市场近年受容量市场和可再生能源并网驱动高速增长) - 背景:Merus Power 为芬兰本地制造商,能够为国际买家提供更接近「本地供应商」身份的 BESS 产品,部分规避中国产品政治风险

→ 对 PG 的影响:CATL 在北欧以本地系统集成商(Merus Power)为渠道落地,是其在欧洲「避锋就利」的典型打法 - 绕过直接供货政治敏感性,以本地品牌包装规避关税/补贴壁垒。若澳洲 CATL 在采购端面临类似情绪,此类「品牌本地化」路线可能在澳洲复现(如 CATL × Zinfra MOU 同理)。对 PG 的 bankability 评估有参考意义。

来源:Merus Power 官方(2026-06-03)· RenewablesNow(2026-06-03)

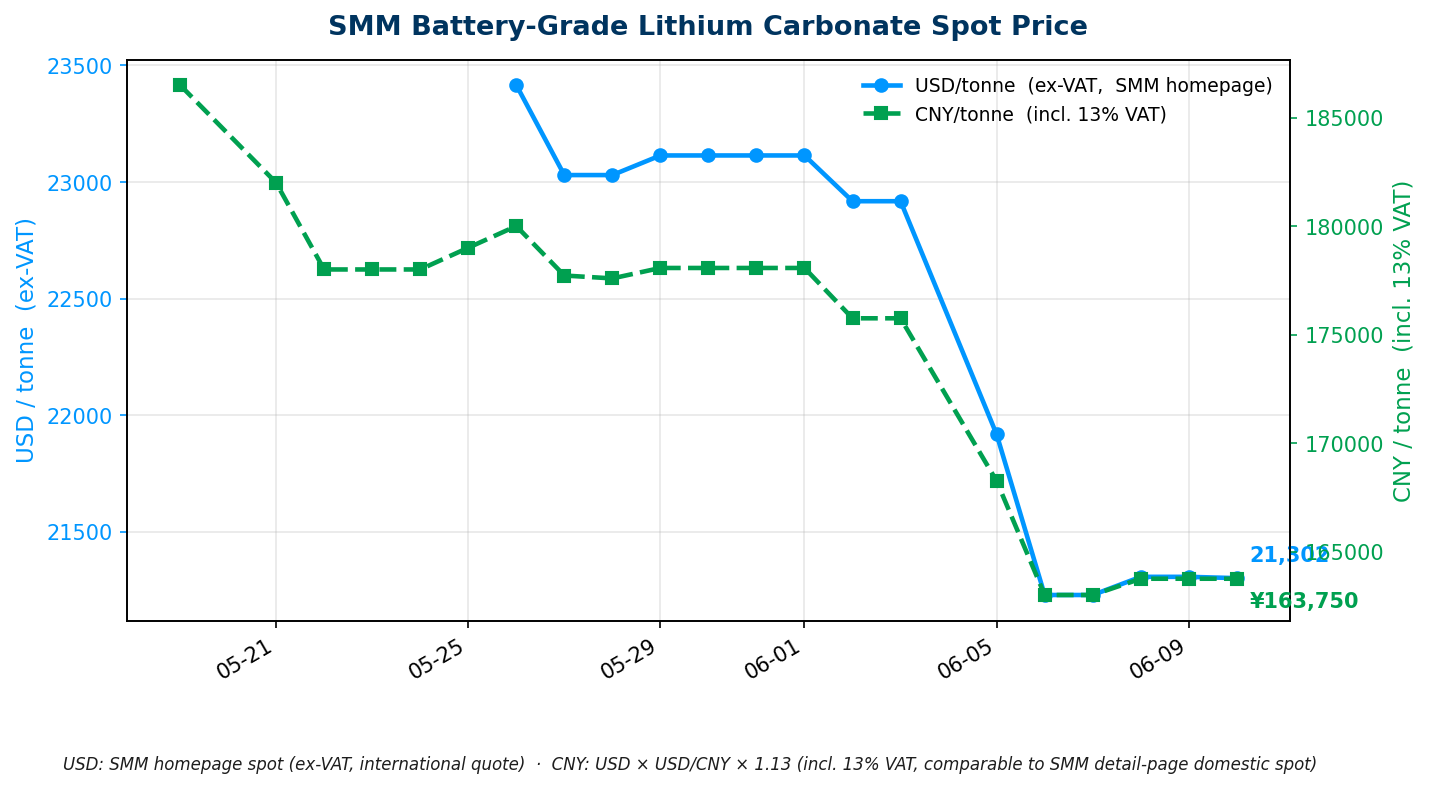

今日价格(口径:2026-06-10 北京时间 07:00 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 21,301.74 / tonne(-5.64,持平) / CNY 163,750 / 吨(0,含 13% VAT 官方精确均价) | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 9 日(SMM 约 10:10 发当日值,7:00 抓为 T-1 是正常) |

走势分析:仓单累库+津巴布韦供给回归双重压力,储能排产创新高托底价格

「多头叙事双重支柱坍塌」:SunSirs(2026-06-09) 将 5 月中旬以来累跌逾 22%(GFEX 2609 从约 CNY 210,000 高点回落至 CNY 163,750)归因于两条多头逻辑相继失效:其一,仓单累库超预期——截至 2026-06-03,广期所碳酸锂仓单量达约 56,000 吨,较 4 月底增加约 2 万吨,相当于国内约半个月产量,现货持续低于期货诱使持货方集中注册套利,形成负向循环;其二,津巴布韦供给恐慌消散——2 月禁令发布后,4 月 10 日起获批企业(成新锂能、中矿资源等)恢复发运,实际减量远低于市场此前预期,机构(东吴电新,06-08)更预警 7-8 月津巴布韦精矿集中到港将再添压力。

产量与矿端:双向信号

储能排产是价格底部保护:6 月 6 家样本企业排产 175.7 GWh(同比 +68%,环比 +6%,超预期)- 据鑫椤锂电(2026-06-08),储能下游需求对价格不敏感,订单满产是防止价格继续深跌的核心托底力量;光大期货(2026-06-08)样本数据显示进口锂盐发运环比下降,进口压力边际改善。

→ 对 PG 的影响:锂价在 CNY 163,000-163,750 区间磨底连续 3 个交易日,短期大幅下行空间受储能满产托底。枧下窝 06-30 前复产信号与 MinRes Bald Hill 7 月首产数据仍是两大催化变量。PG 采购框架锁价时点判断维持不变:待 Bald Hill 7 月实物数据落地、同步关注枧下窝 06-30 申请结果。趋势图如上,近 3 日价格区间 CNY 163,000-163,750,波动收窄进入横盘。

来源:SMM-Li-LC-001 Avg(metal.com API);SunSirs(2026-06-09);上海证券报综合(2026-06-09);鑫椤锂电(2026-06-08);东吴电新(2026-06-08);光大期货(2026-06-08);MinRes 官方复产公告;完整台账见 活表 D

今日无新增重要技术动态

本期覆盖窗口内,主要技术公告均为 SNEC 2026(06-03~05)展后尾声的补报,核心内容(SVOLT CTR 架构 / 华为构网型 PCS RTE 97.8% / CATL 钠电 2026-09 交付 / Hithium ∞Power 6.9 MWh LDES)已于 Issue 17-19 完整报道,本期不重复。

持续跟踪方向: - 构网型 BESS 澳洲落地时间线:AEMO 强制要求 2026-10-28 起新并网 BESS 具备构网能力,此前 6 个月是供应链锁定窗口 - 钠离子电池商业交付:CATL 9 月首批;REPT Battero 澳洲买家 MOU(SNEC 现场)进展 - Eku Energy Griffith 10 小时 BESS EPBC 审批进展(上文第一节)—— 可视为 NEM 长时储能赛道先行指标

Modo Energy Daily Briefing(2026-06-09)澳洲要点 · Modo Energy,2026-06-09

Modo Energy 在 6 月 9 日每日简报中确认以下澳洲方向核心动态:

Edify Energy × CATL QLD 2,400 MWh - 简报原文:「CATL will supply 2,400 MWh of battery storage for Edify Energy's 600 MW hybrid solar-plus-storage projects in central Queensland, backed by long-term offtake and financing agreements.」与本期第一节报道内容完全吻合,形成独立交叉验证。

Eku Energy Griffith BESS 提交 EPBC - 简报原文:「Eku Energy has submitted its expanded 100MW/1,000MWh (10-hour) Griffith BESS for environmental assessment under Australia's EPBC Act, marking one of the NEM's longest-duration battery projects.」与本期第一节报道一致。

(注:简报中提及 Ark Energy Richmond Valley「3,148 MWh」为旧数字,已于 Issue 17 据 Korea Zinc 官方公告修正为 275 MW / 2,200 MWh,本期从 Modo 原文 - 以官方数字为准。)

→ 对 PG 的影响:本期两条澳洲核心增量均经 Modo 独立确认,交叉验证通过。Modo 其余条目为北美(PJM / ERCOT / CAISO 收益对比)和欧洲(德国 BESS / 英国 AMBERS)方向,与 PG 当前澳洲优先策略关联度有限,略去不表。

来源:Modo Energy(2026-06-09)

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Companion Tables (continuously updated by this routine): - Australia Projects Supply Chain · Table C — This issue: 1 new entry: Edify Energy × CATL QLD 2,400 MWh - Chinese Suppliers Overseas Projects · Table A — This issue: 1 new entry: Merus Power × CATL Nordic 3 GWh framework - Supplier Profiles · Table B — This issue: CATL row updated (Edify QLD + Nordic framework) - Lithium Price History · Table D — 06-10 row appended (SMM latest date Jun 9, T-1 normal); trend chart regenerated

Full project supply chain BOM: Table C.

Edify Energy × CATL: QLD Smoky Creek + Guthrie's Gap 2,400 MWh Supply Contract (06-09) · Energy-Storage.news / RenewablesNow, 2026-06-09

Edify Energy (backed by La Caisse, the Canadian institutional investor) announced that its two Queensland hybrid solar-plus-storage projects have reached financial close with CATL supply agreements signed. Both projects operate as independent assets.

Core specifications and supply chain: - BESS: 600 MW / 2,400 MWh (each 300 MW / 1,200 MWh, 3-hour); paired with 720 MWp PV; located in QLD Banana Shire, approximately 40 km north of Biloela - CATL: supplying LFP cells (including grid-forming inverter + reverse DC-coupled hybrid architecture) - EPC: DT Infrastructure (Australian subsidiary of Malaysian contractor Gamuda), turnkey contract - Grid connection: Powerlink 275 kV backbone, new purpose-built substation - Revenue structure: Rio Tinto 20-year hybrid services agreement (purchasing 90% of electricity and storage capacity) + CIS contract dual-layer revenue guarantee - Financing: 14 domestic and international bank syndicate, closed May 2026; COD target 2028

Background: Edify Energy has an established track record in QLD and SA (including Bulgana 350 MW). This dual-project package uses a single EPC and supply chain solution with a financing structure - industrial off-taker PPA + CIS - that represents the current benchmark for bankable large-scale hybrid storage in Australia.

→ For PG: CATL's single-announcement Australian supply volume of 2,400 MWh is the largest to date, cementing its position as the leading battery supplier in the Australian market. The "Rio Tinto 20-year PPA + CIS" structure validates the bankability of combining industrial long-term contracts with government-backed revenue support - a template PG can reference for QLD / NSW project financing. DT Infrastructure (Gamuda) entering large-scale hybrid EPC positions it alongside INTEC × Gotion as a new EPC option in the Australian market.

Sources: Energy-Storage.news (2026-06-09) · Corroborated by RenewablesNow (2026-06-09)

Eku Energy Griffith BESS (NSW Yoogali, 100 MW / 1,000 MWh): Federal EPBC Submitted (06-09) · Energy-Storage.news, 2026-06-09

Eku Energy (Macquarie Asset Management + BCI) has upgraded its Griffith BESS design from the original LTESA-awarded configuration (100 MW / 800 MWh, 8-hour) and formally submitted for Federal EPBC assessment, making it one of the longest-duration standalone BESS projects in the NEM currently in the federal approvals pipeline.

Specifications and milestones: - 100 MW / 1,000 MWh (10-hour duration); located at NSW Yoogali (Griffith LGA), 9.33 hectares - Expanded by +200 MWh from the original LTESA award, extending to 10 hours - exceeding the 8-hour minimum threshold under NSW and SA requirements - Grid connection: 132 kV underground cable to Transgrid's Griffith Substation; co-located with a proposed 15 MW Yoogali solar PV facility, reducing grid BOS costs - LTESA support: One of NSW's first 8-hour storage contracts under the Electricity Infrastructure Roadmap (awarded 2023, up to 14-year term), with expanded storage volume under the upgraded design - EPBC submission signals completion of state planning approvals (NSW IPC) and grid connection negotiations; COD target 2028

Background: Eku Energy's global target is 9 GWh of storage by 2028. If EPBC clears quickly (comparable projects: 19-day precedent), financial close could follow within months of approval, with construction commencing in early 2027.

→ For PG: Eku's 10-hour long-duration BESS is the first of its kind to enter federal assessment in NSW, setting a competitive benchmark in the LDES segment. NSW LTESA Tender Round 9 (12 GWh, ≥8h) registration closes 06-22 (12 days). PG must confirm internal decision on any eligible NSW LDES pipeline projects this week to avoid missing the registration deadline.

Source: Energy-Storage.news (2026-06-09)

CIS Tender 8 (4 GW / 16 GWh NEM Dispatchable): AEW Day 1 (06-10) Underway, No Award Yet · ASL website / media, ongoing

Australian Energy Week 2026 (06-09~12, Melbourne) first main conference day (06-10) is in progress. Federal Energy Minister Chris Bowen is in Bonn, Germany for UNFCCC climate negotiations this week; major policy announcements are expected to await the Energy Policy Forum (06-12) or his return. Key speakers confirmed today include AEMO CEO Daniel Westerman, Victorian Energy Minister Lily D'Ambrosio, and Transgrid CEO Brett Redman. ASL website Tender 8 status remains "Bids are currently being assessed" as of this report.

NSW LTESA Tender 9 registration deadline: 12 days remaining (06-22). Registration is a mandatory prerequisite for bid submission; it cannot be reinstated once missed.

→ For PG: Energy Policy Forum 06-12 is the final concentrated opportunity for Tender 8 announcement this month. Tender 9 registration window (12 days) constitutes a hard decision node this week.

No significant new policy developments today

Within this issue's coverage window, AEMO, AEMC, and AER have issued no new rule determinations or major consultation publications. Australian Energy Week (06-10 to 06-12) remains the primary policy signal window this week; no federal-level policy announcements have been made at the main conference as of this report.

Ongoing tracking:

→ For PG: Monitor RenewEconomy and AEW official media channels through 06-11 to 06-12; Energy Policy Forum (06-12) is the highest-probability window for major policy announcements this week.

Australian projects: Table C; non-Australian projects: Table A.

CATL × Merus Power (Finland): 3 GWh Nordic BESS Strategic Cooperation Framework (06-03) · Merus Power official / RenewablesNow, 2026-06-03

Finnish listed power electronics company Merus Power (HEL:MERUS) and CATL have signed a strategic cooperation agreement, scaling up their established three-year partnership (approximately 500 MWh already delivered) to target delivery of approximately 3 GWh of BESS solutions in the Nordic market.

Supply chain structure: - CATL: Providing battery cells (LFP storage cells) - Merus Power: Responsible for power electronics, grid inverter technology, cyber-secure control and protection systems, and local system integration and delivery - Market: Finland as primary hub, covering the broader Nordic region (Nordic storage markets driven by capacity mechanisms and renewable integration) - Context: As a Finnish-listed domestic manufacturer, Merus Power enables CATL to access Nordic markets with a "local supplier" profile, partially navigating political risk around Chinese-origin products

→ For PG: CATL's approach in the Nordics - using a local systems integrator (Merus Power) as the market-facing entity - mirrors its Australian strategy (e.g., CATL × Zinfra MOU). If similar political or financing sensitivities around Chinese equipment emerge in Australia, this "local brand" channel model could accelerate. PG's bankability assessments should account for the distinction between the nominal supplier (Merus Power / Zinfra) and the ultimate technology and cell origination (CATL).

Sources: Merus Power official (2026-06-03) · RenewablesNow (2026-06-03)

Today's price (collected 07:00 Beijing time, 2026-06-10)

| Product | Latest Price | Notes |

|---|---|---|

| Battery-Grade Lithium Carbonate (SMM) | USD 21,301.74 / tonne (-5.64, flat) / CNY 163,750 / tonne (0, incl. 13% VAT, official average) | SMM-Li-LC-001 Avg; SMM latest date Jun 9 (SMM publishes daily value ~10:10; collecting at 7:00 as T-1 is normal) |

Market Analysis: Dual pressures from inventory build and Zimbabwe supply normalisation; record battery production provides price floor

SunSirs (2026-06-09) characterises the cumulative -22%+ decline since mid-May (GFEX 2609 from ~CNY 210,000 to CNY 163,750) as a "dual collapse of the bull narrative": first, warehouse inventory accumulation exceeded expectations - Guangzhou Futures Exchange lithium carbonate warehouse receipts reached approximately 56,000 tonnes as of 2026-06-03, up ~20,000 tonnes from end-April, equivalent to roughly half a month of domestic production. Cash prices persistently below futures created arbitrage incentives for holders to register warehouse receipts, triggering a reinforcing negative cycle. Second, the Zimbabwe supply scare unwound - following the late-February export suspension, approved companies (Chengxin Lithium, CITIC Guoan Baimahu) resumed shipments from 10 April, with actual supply reduction far below initial panic estimates. Dongwu Securities (2026-06-08) further warns that concentrated Zimbabwe spodumene arrivals in July-August will add further downside pressure.

Production and mine-side: conflicting signals

Battery production is the price floor: June battery production schedule at 6 sample companies reached 175.7 GWh (+68% YoY, +6% MoM, above expectations) - Xinluo Lithium (2026-06-08): storage end-demand is price-insensitive; full-order manufacturing is the fundamental defence against further price decline. Guangda Futures (2026-06-08) sample data showed imported lithium salt shipments declining MoM, easing import pressure at the margin.

→ For PG: Spot prices are consolidating at CNY 163,000-163,750 for the third consecutive session. Large-scale downside is constrained by full-order battery manufacturing, while near-term upside is capped by warehouse inventory overhang and anticipated Zimbabwe arrivals. PG's procurement timing framework remains unchanged: await Bald Hill July production data, with simultaneous monitoring of the Jiangxia 06-30 application outcome.

Sources: SMM-Li-LC-001 Avg (metal.com API); SunSirs (2026-06-09); Shanghai Securities News (2026-06-09); Xinluo Lithium (2026-06-08); Dongwu Securities (2026-06-08); Guangda Futures (2026-06-08); MinRes official restart announcement; full ledger: Table D

No significant new technology announcements today

Within this issue's coverage window, major technology releases are predominantly follow-on reporting from SNEC 2026 (06-03~05); core items (SVOLT CTR architecture / Huawei grid-forming PCS RTE 97.8% / CATL sodium-ion 2026-09 delivery / Hithium ∞Power 6.9 MWh LDES) were reported in full in Issues 17-19 and are not repeated here.

Ongoing tracking directions: - Grid-forming BESS supply chain lock-in window: AEMO requires all new BESS grid-connected from 2026-10-28 to have grid-forming capability - the next 6 months are the critical procurement window - Sodium-ion commercial delivery: CATL September first batch; REPT Battero Australian buyer MOU (SNEC, in-progress) - Eku Energy Griffith 10-hour BESS EPBC timeline (Section I above) - a leading indicator for the NEM's LDES track

Modo Energy Daily Briefing (2026-06-09) - Australia Key Points · Modo Energy, 2026-06-09

Modo Energy's 9 June daily briefing independently confirms the following Australia-specific core items:

Edify Energy × CATL QLD 2,400 MWh - Briefing text: "CATL will supply 2,400 MWh of battery storage for Edify Energy's 600 MW hybrid solar-plus-storage projects in central Queensland, backed by long-term offtake and financing agreements." Fully consistent with Section I reporting, providing independent cross-validation.

Eku Energy Griffith BESS EPBC submission - Briefing text: "Eku Energy has submitted its expanded 100MW/1,000MWh (10-hour) Griffith BESS for environmental assessment under Australia's EPBC Act, marking one of the NEM's longest-duration battery projects." Consistent with Section I.

(Note: The briefing cites Richmond Valley at "3,148 MWh" - Issue 17 corrected this figure to 275 MW / 2,200 MWh per Korea Zinc's official announcement; the official source takes precedence.)

→ For PG: Both Australian core incremental items this issue have been independently confirmed by Modo. Remaining Modo content covers North American markets (PJM / ERCOT / CAISO revenue comparisons) and European markets (Germany BESS / UK AMBERS programme), with limited direct relevance to PG's current Australia-first strategy.

Source: Modo Energy (2026-06-09)

This research brief is automatically compiled daily by PGSH's internal research system; each item's source is individually cited. Project progress, policy developments, price data, and institutional views presented are for internal reference only and do not constitute investment, procurement, or commercial decision-making advice. For any item of interest or intended action, please open the corresponding source link directly to verify the accuracy and currency of the information.