类型:增量 · 覆盖窗口:2026-06-06 ~ 2026-06-07(基线 2026-06-06)

本期为按新「信源纪律」(日期闸 + 同日多源 + deep-link) 重跑的修订版:每条均已核验原文发布日在近 7 天内、来源链接可直接点开看到原文。较今早版本:修正 Richmond Valley 规模 (275/2,200,非 475/3,148)、剔除旧闻、补回今早漏掉的真实增量 (Orana 满功率 / Bunyip North / AER 两项 / CATL 双动态 / Siemens-NVIDIA-Fluence)。

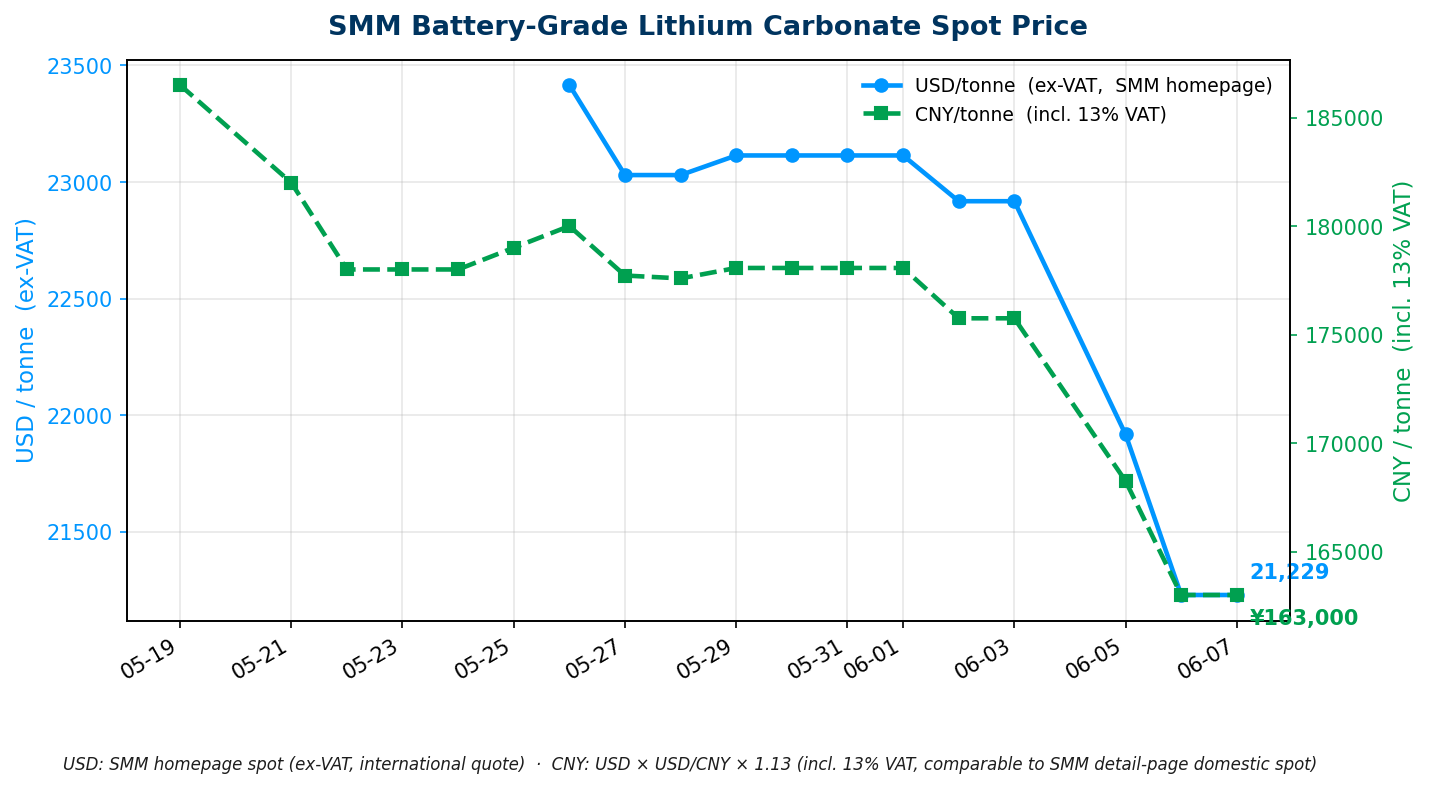

周日。本期核心:Richmond Valley BESS(NSW,275 MW / 2,200 MWh + 200 MW PV,Ark Energy/Korea Zinc)获电网接入批准,走完 DA + EPBC + 电网接入三关,韩国 Korea Zinc 以 BOO 模式直接开发澳洲长时储能;Lower Wonga(QLD,281 MW / 843 MWh + 380 MWdc PV,Lightsource bp)正式开工,EPC = INTEC × Gotion JV;Akaysha Orana BESS(NSW,415 MW / 1,660 MWh)达满功率,同时 BlackRock「Project Ironbark」出售数据室已开放(7 月收意向报价);AER Transgrid MCC 裁定(06-04) 将 GFM BESS 列为 AU$63 亿系统强度方案的非网络备选;CATL 战略转储能——厦门 ESVL 全球最大测试平台开园 + 2030 储能占全球销售 50% 目标;Siemens × NVIDIA × Fluence 发布 136 MW AI 数据中心参考架构,BESS 首次进入 AI Factory 标准蓝图。锂价 SMM USD 21,229.46 / CNY 163,000(smm_date 06-05,周日休市持平)。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 本修订版新增/修正:Richmond Valley(规模修正 275/2,200)、Akaysha Orana 满功率、RES Bunyip North EPBC - 中国供应商海外项目 · 表 A — 本期 HyperStrong 巴尔干、Trina 罗马尼亚两条海外新单 - 供应商档案 · 表 B — 本期无更新 - 锂价历史 · 表 D — 06-07 行 USD 21,229.46(SMM 最新 Date 6 月 5 日,周日休市不更新,为正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

Richmond Valley Solar+BESS(NSW,275 MW / 2,200 MWh;配套 200 MW PV):获电网接入批准 · Korea Zinc 官方公告 / Seoul Economy Daily,2026-06-05

Korea Zinc 旗下澳洲子公司 Ark Energy 宣布,Richmond Valley Solar & BESS 项目已获 Transgrid 和 AEMO 的电网接入批准,这是继州开发审批(DA)和联邦 EPBC 环评之后、进入建设前的最后一道关键监管程序。

规格与背景: - BESS:275 MW / 2,200 MWh(约 8 小时长时);配套 200 MW PV - 选址:NSW 东北部 Richmond Valley 地区,Myrtle Creek 附近 - 三道审批已全部通过:州 DA + 联邦 EPBC(无附带条件)+ 本次电网接入 - 商业模式:BOO(Build-Own-Operate),Ark Energy 全程自建自持自运——这是 Ark Energy 首个采用 BOO 模式的大型可再生项目 - Korea Zinc:全球最大锌冶炼商,澳洲 BESS 开发是其 ESG / 脱碳战略的核心增长点

→ 对 PG 的影响:韩国工业资本(Korea Zinc)以 BOO 模式走完全部监管流程后直接进入建设运营,与 PG 的 Portland / Nine Mile 项目融资—建设路径高度可比;275 MW / 2,200 MWh 的 8 小时长时配置正对标 NSW LDES 政策偏好,是 NSW 电网接入容量与供应链资源的直接竞争者。

来源:Seoul Economy Daily(Korea Zinc 公告)(2026-06-05)· 佐证 MK Business

Lower Wonga Solar+BESS(QLD,281 MW / 843 MWh + 380 MWdc PV):正式开工,EPC 含 Gotion · Lightsource bp 官方 / PV Tech,2026-06-05

Lightsource bp 宣布 Lower Wonga Solar & BESS 混合项目在昆士兰 Gympie 附近正式破土动工,是其在澳洲第二个进入建设阶段的太阳能+储能混合项目。

核心数据: - BESS:281 MW / 843 MWh(3 小时);PV:380 MWdc - EPC:INTEC Energy Solutions × Gotion Hi-Tech Australia 联合体——Gotion 以工程总承包角色深度参与澳洲大陆电网侧 BESS - 收益结构:与 Rio Tinto 的混合(solar+BESS)长期 PPA + CIS 合同底托双层 - 紧邻 Powerlink 已有的 Woolooga 275 kV 变电站,降低并网基建成本;峰值施工 400-500 人;COD 目标 2028 年底

→ 对 PG 的影响:Gotion 从设备供应深入到 EPC 工程端,是中国企业在澳角色升级的标志性节点;「工业大用户混合 PPA + CIS」双层收益结构,是当前澳洲大型混合项目融资的有力范式,PG 评估类似结构时可引为同期参照。

来源:Lightsource bp 官方公告(2026-06-05)· 佐证 PV Tech、Renewables Now

Akaysha Orana BESS(NSW,415 MW / 1,660 MWh):达满功率输出 · ESS News / RenewEconomy,2026-06-04

Akaysha Energy(BlackRock)确认 NSW 中西部 Wellington 附近的 Orana BESS 已达满功率(415 MW / 1,660 MWh,4 小时),正式在 NEM 可见并参与调度,按时且低于预算完工。

→ 对 PG 的影响:「200 MW 锚点合约 + 215 MW 商人化」的双轨收益结构,正成为澳洲大型 BESS 融资模板;PG 在 NSW Nine Mile 及 VIC 项目设计融资结构时可直接参考。

来源:ESS News(2026-06-04)· 佐证 RenewEconomy

Akaysha「Project Ironbark」出售:数据室已开放,7 月收意向报价 · Financial Post / Bloomberg,2026-06-04

BlackRock 委托 Macquarie Capital 主导的 Akaysha 股权出售进程升级:数据室(data room)已正式向意向买家开放,indicative bids 截止 2026 年 7 月。

→ 对 PG 的影响:成交倍数将重定价澳洲大型 BESS 资产估值基准;若产业买家接盘可能带来垂直整合、改变竞争格局,PG 自身融资 / 股权安排可引为外部参照。(注:AFR 5 月中旬的推销材料首报已超本期窗口,本条仅记 06-04 数据室开放这一新进展。)

来源:Financial Post / Bloomberg(2026-06-04)

RES Australia Bunyip North BESS(VIC,400 MW / 2,400 MWh):通过联邦 EPBC 环评 · Energy-Storage.news / 项目官网,2026-06-01

RES Australia 的 Bunyip North BESS(400 MW / 2,400 MWh,6 小时)获联邦 EPBC「非管控行动」认定,无需进一步联邦环评。选址 VIC Cardinia Shire(墨尔本东南约 80 km),约 30.8 公顷农地,直接切入 Yallourn–Rowville 220 kV 线路;施工预计 2027 年中启动、2029 年中投产。

→ 对 PG 的影响:VIC Gippsland 区域多个 6 小时 BESS(含 Akaysha Glenrowan)连续 EPBC 快速通关,长时储能竞争加剧;PG 的 Limestone Coast / Gelliondale 邻近项目在融资与并网时序上面临更密竞争。

来源:Energy-Storage.news(2026-06-01)· 佐证 项目官网

CIS Tender 8(4 GW / 16 GWh):截至 06-07 仍未授标 · DCCEEW / ASL,持续跟踪

ASL 官网状态截至本期仍为「Bids are currently being assessed」。官方授标窗口为「2026 年 6 月」,本月余下约 3.5 周仍在等待期内。

→ 对 PG 的影响:Tender 8 结果一旦落地,将揭示 16 GWh 纯储能合同的区域分布与竞争格局,直接指导 Tender 10 竞价策略。本周内仍属高概率发布窗口。

AER Transgrid MCC 裁定(06-04):AU$63 亿系统强度方案纳入 GFM BESS 非网络备选 · AER,2026-06-04

AER 就 Transgrid NSW 系统强度 RIT-T 的「重大情况变更(MCC)」作出正式裁定:Transgrid 10 台同步调相机采购成本较原 RIT-T 评估值上涨超 30%(触发 MCC 重开条款),原方案总预算约 AU$63 亿(含调相机 + 配套 GFM BESS 非网络方案)。

AER 要求 Transgrid: - 2026-06-24 前发布更新分析草稿(开放 1 个月公众咨询) - 2026-08-24 前发布最终声明

关键意义:裁定文本明确将 grid-forming BESS 列为首选非网络方案组成部分,是 AER 在规模级监管文件中正式确认 GFM BESS 在 NSW 系统强度解决方案中的核心角色。

→ 对 PG 的影响:调相机成本飙升使电网侧对 GFM BESS 替代方案的需求更紧迫;若 PG Portland / Nine Mile 具备 GFM 能力,可在电网接入谈判中作为系统强度贡献加分项。关注 06-24 草案。

来源:AER 裁定登记页(2026-06-04)· AER 新闻公告

AER 网络韧性指引咨询(第一阶段,06-04 启动) · AER,2026-06-04

AER 启动「Network Resilience Guidelines」制定第一阶段咨询(由 AEMC 2025-05-08 终版规则赋权),规范配电网运营商(DNSP)提出「韧性支出」项目的申报框架。意见截止 2026-07-10;最终指引须 2026-12-01 前发布。

→ 对 PG 的影响:若最终指引将 BESS 明确纳入「韧性资产」,可能为电网侧 BESS 开辟 DNSP 侧额外监管收入路径;咨询期介入提交意见可塑造对 BESS 有利的条款。中期关注。

AER 发布统一零售指引草案(06-05) · AER,2026-06-05

AER 将四份执行性零售指引合并为一份《Draft AER Retail Guidelines》(定价信息 / 优惠变更通知 / 账单 / 客户困难政策),转向「诚实公正」原则导向,适应含电池 / V2G / VPP 套餐的新型能源零售计划入市。意见截止 2026-07-17,最终版预计 2026-09。

→ 对 PG 的影响:随 PG 涉足零售 / 聚合(VPP、BESS 辅助服务零售侧产品),合规框架统一降低进入门槛。直接相关度中等。

来源:AER 新闻公告(2026-06-05)· 草案文件页

HyperStrong(海博思创):巴尔干 1 GWh+ 储能订单(罗马尼亚 + 克罗地亚 / 塞尔维亚) · EnergyTrend,2026-06-02/03

HyperStrong 签下东南欧 >1 GWh 大储订单:罗马尼亚两个大型项目 >900 MWh + 克罗地亚 / 塞尔维亚 75 MWh,供货其 HyperBlock III AC 版大储系统及工商业户外柜。背景:罗马尼亚市场有 EBRD 融资(€44M 支持 Scornicesti BESS)+ 欧盟 €150M 独立储能补贴(2026-03 获批)托底。

→ 对 PG 的影响:HyperStrong 从亚太向东南欧快速渗透,巴尔干标杆若顺利交付将强化其 bankability,意味着 PG 在非澳市场采购时会面对更具价格竞争力的中国集成商。

来源:EnergyTrend(2026-06-03)

Trina Storage(天合储能):罗马尼亚 Gamma BESS 40 MW / 160.48 MWh 交付(欧洲首个 Elementa + Electra 一体化) · Trina 官方 / PR Newswire,2026-05-29

Trina Storage 完成罗马尼亚 Izvoarele(Giurgiu 县)Gamma 项目设备交付:32 台 Elementa 2 Pro + 4 台 Electra AC 单元,是其 DC+AC「Cell-to-AC」一体化方案在欧洲首次落地;买家为本地开发商 LSG,计划 Q3 2026 投运。Trina Storage 2026 年欧洲签单已超 6 GWh。

→ 对 PG 的影响:Trina 从供货商向「交钥匙」EPC 进化,Cell-to-AC 方案若获欧洲银行可融资认可,其在亚太投标竞争力将同步上升;PG 国际采购可纳入评估名单并关注其交付记录是否达 IFC 标准。

来源:Trina Storage 官方(2026-05-29)· 佐证 PR Newswire

SNEC 2026(上海,06-03/05)闭幕后第二天(周日),Watchlist 其余供应商(CATL / BYD / EVE / Hithium / Envision / Sungrow / REPT / CORNEX)本期均无 ≥100 MWh 新海外项目正式公告,展后合同预计 06-09(周一)起密集披露。

今日价格(口径:2026-06-07 北京时间采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 21,229.46 / tonne(0,持平) / CNY 163,000 / 吨 | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 5 日(周日休市 SMM 不更新;与 06-06 值相同,为正常);CNY 含 13% VAT 官方精确均价 |

走势分析:三重压制延续,仓单拐点是短期关键变量

据 SMM 周评(2026-06-04),6 月第 1 周碳酸锂现货持续下行,三条压力线延续:① 仓单持续累库(截至 06-01 约 55,215 手 ≈ 5.5 万吨,中粮期货预计下周破 6 万手);② 5 月产量大幅放量(62,100 吨,+27.9% MoM,锂辉石加工端复产 + 青海盐湖爬产);③ 月初现货成交清淡(动力电芯淡季买盘薄弱)。

机构短期观点(06-04/05 综合)

矿端关键节点(Q3 观察)

→ 对 PG 的影响:SMM 价 USD 21,229 / CNY 163,000 较本轮高点(约 CNY 180,000)回撤约 10%,已接近卓创 / 长江有色 CNY 155,000-165,000 磨底区间上沿。PG 采购框架锁价时点维持「Bald Hill 7 月首产数据落地后、同步关注 CATL 枧下窝 6 月 30 日申请结果」判断不变。

来源:财联社引述 SMM / 卓创资讯 / 中粮期货 / 长江有色 / 大地期货(2026-06-05,机构走势观点为综合转述、无单篇原文链接);完整台账见 活表 D

Siemens × NVIDIA × Fluence:136 MW AI 数据中心参考架构发布,BESS 首次进入 AI Factory 标准蓝图 · Siemens 官方 / ESS News,2026-06-01

Siemens 联合 NVIDIA、Fluence 发布全球首个专为 NVIDIA DSX Vera Rubin NVL72 平台打造的 AI 工厂标准参考架构:总设施容量 136 MW(IT 负载 100 MW),34.5 kV 公用电网接入 → 中压配电 → 模块化低压电力块,按 Tier III 设计。Fluence Smartstack 模块化 BESS 作为架构内置组件,承担电压 / 频率穿越、黑启动、需求响应、AI 负载平滑(AI 功率波动极大需 BESS 缓冲)。Fluence 确认已与两家超大规模云厂商签主供应协议,本季度首单落地。

→ 对 PG 的影响:这是 BESS 从 AI 基础设施「可选项」变「标准件」的里程碑。Fluence 已明言美国超大规模蓝图定稿后澳洲部署将加速(弹弓效应)。PG 应提前研究数据中心配储新业务模式——收益逻辑(电网服务合约 + 运维稳定性)与响应时间要求都不同于传统 NEM 套利。

来源:Siemens 官方新闻(2026-06-01)· 佐证 ESS News

CATL 厦门 ESVL:全球最大储能测试验证平台开园(RMB 30 亿) · CATL 官方 / pv-magazine,2026-06-01

CATL 在厦门开园全球最大一站式储能系统测试验证平台(ESVL,占地 10 公顷):站级并网实验室配 35 kV / 100 MVA 电网模拟器(NREL 同类 14 倍),可同测 10 个大型储能舱;全球首座大型室内燃烧实验室配 20 MW 量热仪,对 9 个储能舱同步做爆炸测试。与 TÜV SÜD / TÜV Rheinland / CSA 合作做「一次测试、多方见证、全球互认」。直接回应行业安全信任危机(国家能源局数据:2025 年底全球 131 起储能事故 80% 发生在正常运行阶段)。

→ 对 PG 的影响:设备质量验证是澳洲银行 / 保险方最关注的风险点(Waratah 变压器事故即警示)。ESVL 第三方数据可作 PG 对接融资方的背书工具;采购合同宜要求供应商提交整站级验证报告,而非只看出厂参数。

来源:CATL 官方(2026-06-01)· 佐证 pv-magazine

CATL:储能业务目标 2030 年占全球销售 50% · Invezz(SNEC 2026 专访),2026-06-04

CATL 欧洲储能系统总监 Kevin Tang 在 SNEC 2026 披露:储能业务已从 5 年前占全球销售 2% 升至约 25%,目标 2030 年达 50%。欧洲为 CATL 第三大储能市场(次于中国、美国),德国 / 匈牙利工厂已投产、西班牙(Stellantis JV)在建。盈利仍承压(锂 / 铜 / 铝原材料上行)。

→ 对 PG 的影响:全球最大电芯商战略重心持续倾向储能,确认 LFP 供给长期充裕、采购端议价有利;CATL 欧澳布局加宽,PG 后续项目拿到 CATL 直供合同的窗口打开,可把握其欧洲制造合规优势谈备货条款。

来源:Invezz(2026-06-04)

LDES Council 联合 9 家机构致函欧委会:要求把长时储能列为战略资产 · LDES Council,2026-06-03

LDES Council 联合 Cleantech for Europe、Energy Storage Europe、Flow Batteries Europe、IHA 等致函欧盟能源专员,要求在《电气化行动计划》中明确把「≥8 小时长时储能」定性为战略资产,四诉求:政策显性写入 LDES、制定 EU LDES 路线图、培育先导市场、建立 LDES 收益确定性机制。

→ 对 PG 的影响:澳欧储能政策高度联动;若欧盟建立 LDES 收益确定性机制,将成澳洲 LDES 政策讨论的参照,钒液流 / 铁空气等非锂长时路线的政策空间打开,对 PG 思考长时化产品组合有参考意义。

来源:LDES Council 联名信(2026-06-03)

本期暂缺

周日无新文章发布(属正常)。最近覆盖为 2026-06-05「NEM 所有 2027-28 新提交太阳能项目 100% 为混合 BESS 系统」(已于 Issue 16 完整报道)。

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注、且经「信源纪律」核验(发布日在近 7 天内、链接可直接点开看到原文)。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental · Coverage window: 2026-06-06 ~ 2026-06-07 (baseline 2026-06-06)

This is a revised re-run under the new "source discipline" (date gate + same-day corroboration + deep-link): every item has been verified to be published within the last 7 days, with a source link that opens directly to the original article. Versus this morning's version: corrected Richmond Valley size (275/2,200, not 475/3,148), dropped stale items, and added genuine increments the morning run missed (Orana full output / Bunyip North / two AER items / CATL double moves / Siemens-NVIDIA-Fluence).

Sunday. Headlines: Richmond Valley BESS (NSW, 275 MW / 2,200 MWh + 200 MW PV, Ark Energy/Korea Zinc) secures grid connection approval, clearing the final of DA + EPBC + grid connection; Korea Zinc develops Australian long-duration storage directly under a BOO model; Lower Wonga (QLD, 281 MW / 843 MWh + 380 MWdc PV, Lightsource bp) breaks ground, EPC = INTEC × Gotion JV; Akaysha Orana BESS (NSW, 415 MW / 1,660 MWh) reaches full output, while BlackRock's "Project Ironbark" sale data room is now open (indicative bids in July); AER Transgrid MCC determination (06-04) lists GFM BESS as the non-network option in a AU$6.3bn system-strength plan; CATL pivots to storage — opens the world's largest validation platform (ESVL) in Xiamen + targets 50% of global sales from storage by 2030; Siemens × NVIDIA × Fluence release a 136 MW AI data center reference architecture, with BESS entering the AI Factory standard blueprint for the first time. Lithium SMM USD 21,229.46 / CNY 163,000 (smm_date 06-05, flat as Sunday market closed).

Companion living tables (cumulative, updated daily): - Australia Project Supply Chain · Table C — this revision adds/corrects: Richmond Valley (size corrected 275/2,200), Akaysha Orana full output, RES Bunyip North EPBC - China Suppliers Overseas Projects · Table A — two overseas new deals this issue: HyperStrong Balkans, Trina Romania - Supplier Profiles · Table B — no update this issue - Lithium Price History · Table D — 06-07 row USD 21,229.46 (latest SMM Date Jun 5; Sunday market closed, normal); trend chart redrawn

Full project supply-chain BOM: Living Table C.

Richmond Valley Solar+BESS (NSW, 275 MW / 2,200 MWh; with 200 MW PV): grid connection approval · Korea Zinc official / Seoul Economy Daily, 2026-06-05

Korea Zinc's Australian subsidiary Ark Energy announced that the Richmond Valley Solar & BESS project has secured grid connection approval from Transgrid and AEMO — the last key regulatory step before construction, after state DA and federal EPBC approvals.

Specs & context: - BESS: 275 MW / 2,200 MWh (~8-hour long-duration); with 200 MW PV - Site: near Myrtle Creek in the Richmond Valley region of northeastern NSW - All three approvals cleared: state DA + federal EPBC (no conditions) + this grid connection - Commercial model: BOO (Build-Own-Operate), Ark Energy handles the full lifecycle — its first large renewable project using BOO - Korea Zinc: world's largest zinc smelter; Australian BESS is core to its ESG / decarbonization growth strategy

→ Implication for PG: Korea Zinc clearing the full regulatory path and going straight to build-own-operate closely parallels PG's Portland / Nine Mile financing-to-construction path; the 275 MW / 2,200 MWh 8-hour config matches NSW LDES policy preference and is a direct competitor for NSW grid-connection capacity and supply-chain resources.

Source: Seoul Economy Daily (Korea Zinc announcement) (2026-06-05) · corroboration MK Business

Lower Wonga Solar+BESS (QLD, 281 MW / 843 MWh + 380 MWdc PV): breaks ground, EPC includes Gotion · Lightsource bp official / PV Tech, 2026-06-05

Lightsource bp broke ground on the Lower Wonga Solar & BESS hybrid near Gympie, Queensland — its second hybrid solar-plus-storage project to enter construction in Australia.

→ Implication for PG: Gotion moving from equipment supply deep into EPC marks China's role escalation in Australia; the "industrial offtaker hybrid PPA + CIS" two-layer revenue structure is a strong financing paradigm for large Australian hybrids that PG can reference.

Source: Lightsource bp official (2026-06-05) · corroboration PV Tech, Renewables Now

Akaysha Orana BESS (NSW, 415 MW / 1,660 MWh): reaches full output · ESS News / RenewEconomy, 2026-06-04

Akaysha Energy (BlackRock) confirmed Orana BESS near Wellington in central-west NSW has reached full output (415 MW / 1,660 MWh, 4-hour), now visible and dispatching in the NEM, completed on time and under budget.

→ Implication for PG: the "200 MW anchor contract + 215 MW merchant" dual-track revenue structure is becoming a template for large Australian BESS financing; PG can reference it directly when structuring financing for NSW Nine Mile and VIC projects.

Source: ESS News (2026-06-04) · corroboration RenewEconomy

Akaysha "Project Ironbark" sale: data room open, indicative bids in July · Financial Post / Bloomberg, 2026-06-04

The Akaysha equity sale led by Macquarie Capital (mandated by BlackRock) has progressed: the data room is now open to interested buyers, with indicative bids due July 2026.

→ Implication for PG: the transaction multiple will reset the valuation benchmark for large Australian BESS assets; an industrial acquirer could bring vertical integration and reshape competition. PG can reference it for its own financing / equity arrangements. (Note: AFR's mid-May teaser first-report is outside this window; this item records only the 06-04 data-room opening.)

Source: Financial Post / Bloomberg (2026-06-04)

RES Australia Bunyip North BESS (VIC, 400 MW / 2,400 MWh): clears federal EPBC · Energy-Storage.news / project site, 2026-06-01

RES Australia's Bunyip North BESS (400 MW / 2,400 MWh, 6-hour) received a federal EPBC "not a controlled action" decision, requiring no further federal assessment. Sited in VIC Cardinia Shire (~80 km SE of Melbourne), ~30.8 ha of farmland, cut into the Yallourn–Rowville 220 kV line; construction expected mid-2027, COD mid-2029.

→ Implication for PG: multiple 6-hour BESS in VIC Gippsland (incl. Akaysha Glenrowan) clearing EPBC fast-track in succession intensifies long-duration competition; PG's nearby Limestone Coast / Gelliondale projects face tighter competition on financing and connection timing.

Source: Energy-Storage.news (2026-06-01) · corroboration project site

CIS Tender 8 (4 GW / 16 GWh): still not awarded as of 06-07 · DCCEEW / ASL, ongoing

ASL's site still shows "Bids are currently being assessed". The official award window is "June 2026", with ~3.5 weeks remaining this month.

→ Implication for PG: once Tender 8 lands it will reveal the regional distribution and competition for 16 GWh of standalone storage contracts, directly informing Tender 10 bidding strategy. This week remains a high-probability release window.

AER Transgrid MCC determination (06-04): AU$6.3bn system-strength plan includes GFM BESS as non-network option · AER, 2026-06-04

AER issued a formal determination on the "Material Change of Circumstances (MCC)" in Transgrid's NSW system-strength RIT-T: procurement cost of 10 synchronous condensers rose >30% vs the original RIT-T estimate (triggering the MCC reopener), with the plan totaling ~AU$6.3bn (condensers + companion GFM BESS non-network option).

AER requires Transgrid to: - Publish an updated draft by 2026-06-24 (1-month public consultation) - Publish a final statement by 2026-08-24

Significance: the determination explicitly lists grid-forming BESS as part of the preferred non-network option — AER formally recognizing GFM BESS's core role in NSW system-strength solutions at a regulatory-scale document.

→ Implication for PG: surging condenser costs make the GFM BESS alternative more urgent for the grid; if PG's Portland / Nine Mile have GFM capability, it can serve as a system-strength bonus in grid-connection negotiations. Watch the 06-24 draft.

Source: AER determination register (2026-06-04) · AER news

AER network resilience guidelines consultation (phase 1, launched 06-04) · AER, 2026-06-04

AER launched phase 1 of consultation on "Network Resilience Guidelines" (empowered by AEMC's 2025-05-08 final rule), framing how DNSPs propose "resilience expenditure" projects. Submissions due 2026-07-10; final guidelines must publish by 2026-12-01.

→ Implication for PG: if the final guidelines explicitly include BESS as a "resilience asset", it could open an additional DNSP-side regulatory revenue path for grid-side BESS; submitting during consultation could shape BESS-favorable terms. Medium-term watch.

Source: AER consultation page (2026-06-04) · news

AER releases draft consolidated retail guidelines (06-05) · AER, 2026-06-05

AER consolidated four enforceable retail guidelines into one Draft AER Retail Guidelines (pricing information / benefit change notice / billing / customer hardship policy), shifting to a "fair and honest" principles-based approach to accommodate new energy plans (battery / V2G / VPP) entering retail. Submissions due 2026-07-17, final expected 2026-09.

→ Implication for PG: as PG moves into retail / aggregation (VPP, BESS ancillary retail products), a unified compliance framework lowers entry barriers. Medium relevance.

Source: AER news (2026-06-05) · draft document page

Australia projects in Living Table C; non-Australia in Living Table A.

HyperStrong: Balkans 1 GWh+ storage order (Romania + Croatia / Serbia) · EnergyTrend, 2026-06-02/03

HyperStrong signed >1 GWh of SE-European storage orders: two large Romanian projects >900 MWh + Croatia / Serbia 75 MWh, supplying its HyperBlock III AC large-storage systems and C&I outdoor cabinets. Backdrop: Romania has EBRD financing (€44M for Scornicesti BESS) + EU €150M standalone-storage subsidy (approved 2026-03) as support.

→ Implication for PG: HyperStrong is penetrating SE Europe fast from APAC; a successful Balkan flagship strengthens its bankability, meaning PG will face more price-competitive Chinese integrators when procuring outside Australia.

Source: EnergyTrend (2026-06-03)

Trina Storage: Romania Gamma BESS 40 MW / 160.48 MWh delivered (Europe's first Elementa + Electra integrated) · Trina official / PR Newswire, 2026-05-29

Trina Storage completed equipment delivery for the Gamma project in Izvoarele (Giurgiu County), Romania: 32 Elementa 2 Pro + 4 Electra AC units — the first European deployment of its DC+AC "Cell-to-AC" integrated solution; buyer is local developer LSG, targeting Q3 2026 operation. Trina Storage's 2026 European bookings already exceed 6 GWh.

→ Implication for PG: Trina is evolving from supplier toward turnkey EPC; if the Cell-to-AC solution gains European bankability, its APAC bidding competitiveness rises in parallel. PG can add it to international procurement evaluation lists and watch whether its delivery record meets IFC standards.

Source: Trina Storage official (2026-05-29) · corroboration PR Newswire

Two days after SNEC 2026 (Shanghai, 06-03/05) closed (Sunday), the rest of the watchlist (CATL / BYD / EVE / Hithium / Envision / Sungrow / REPT / CORNEX) had no ≥100 MWh new overseas project announcements this issue; post-show contracts expected to publish densely from Monday 06-09.

Today's price (collected 2026-06-07 Beijing time)

| Product | Latest | Basis |

|---|---|---|

| Battery-grade lithium carbonate (SMM) | USD 21,229.46 / tonne (0, flat) / CNY 163,000 / tonne | SMM-Li-LC-001 Avg; latest SMM Date Jun 5 (Sunday market closed, SMM not updated; same as 06-06, normal); CNY incl. 13% VAT, official precise average |

Trend: triple suppression continues, the warrant inflection is the key near-term variable

Per SMM weekly (2026-06-04), lithium carbonate spot kept falling in the first week of June, with three pressure lines: ① continued warrant build-up (~55,215 lots ≈ 55kt as of 06-01, COFCO Futures expects >60k lots next week); ② May output surge (62,100 t, +27.9% MoM, spodumene processing restarts + Qinghai brine ramp); ③ thin early-month spot turnover (weak off-season EV-cell buying).

Institutional near-term views (06-04/05)

Mine-side milestones (Q3 watch)

→ Implication for PG: SMM USD 21,229 / CNY 163,000 is ~10% off the cycle high (~CNY 180,000), near the upper edge of the CNY 155,000-165,000 bottoming range cited by Sublime / Changjiang. PG's procurement framework pricing timing holds: "after Bald Hill's first July output data, with attention to CATL Jianxiawo's June 30 application."

Source: Caixin citing SMM / Sublime China / COFCO Futures / Changjiang Nonferrous / Dadi Futures (2026-06-05; institutional trend views are aggregated paraphrase with no single source article); full ledger in Living Table D

Siemens × NVIDIA × Fluence: 136 MW AI data center reference architecture, BESS enters the AI Factory standard blueprint for the first time · Siemens official / ESS News, 2026-06-01

Siemens, with NVIDIA and Fluence, released the world's first standard reference architecture purpose-built for NVIDIA's DSX Vera Rubin NVL72 platform: total facility capacity 136 MW (IT load 100 MW), 34.5 kV grid connection → medium-voltage distribution → modular low-voltage power blocks, Tier III design. Fluence Smartstack modular BESS is a built-in component handling voltage/frequency ride-through, black start, demand response, and AI workload smoothing (AI power swings are large and need BESS buffering). Fluence confirmed master supply agreements with two hyperscalers, first orders this quarter.

→ Implication for PG: a milestone of BESS moving from "optional" to "standard component" in AI infrastructure. Fluence has stated Australian deployment will accelerate once US hyperscale blueprints are finalized (slingshot effect). PG should study the data-center storage business model early — its revenue logic (grid-service contracts + operational reliability) and response-time requirements differ from traditional NEM arbitrage.

Source: Siemens official news (2026-06-01) · corroboration ESS News

CATL Xiamen ESVL: world's largest storage validation platform opens (RMB 3bn) · CATL official / pv-magazine, 2026-06-01

CATL opened the world's largest one-stop storage system test & validation platform (ESVL, 10 ha) in Xiamen: a station-level grid lab with a 35 kV / 100 MVA grid simulator (14× NREL's equivalent), able to test 10 large storage units simultaneously; the world's first large indoor combustion lab with a 20 MW calorimeter for explosion testing of 9 units at once. Partners with TÜV SÜD / TÜV Rheinland / CSA for "test once, witnessed by many, recognized globally". A direct response to the industry's safety trust crisis (NEA data: 80% of 131 global storage incidents through end-2025 occurred during normal operation).

→ Implication for PG: equipment quality validation is the top risk concern for Australian banks / insurers (the Waratah transformer incident being a warning). ESVL third-party data can serve as PG's backing tool with financiers; procurement contracts should require station-level validation reports, not just factory specs.

Source: CATL official (2026-06-01) · corroboration pv-magazine

CATL: targets 50% of global sales from storage by 2030 · Invezz (SNEC 2026 interview), 2026-06-04

CATL's European storage systems director Kevin Tang disclosed at SNEC 2026: storage has grown from 2% of global sales 5 years ago to ~25%, targeting 50% by 2030. Europe is CATL's third-largest storage market (after China, US), with German / Hungarian plants in production and Spain (Stellantis JV) under construction. Profitability remains pressured (lithium / copper / aluminum input costs rising).

→ Implication for PG: the largest cell maker's strategic tilt toward storage confirms long-term abundant LFP supply and procurement-side bargaining advantage; CATL's widening Europe-Australia footprint opens a window for PG to secure CATL direct-supply contracts on future projects, leveraging its European manufacturing compliance edge for stocking terms.

Source: Invezz (2026-06-04)

LDES Council and 9 organizations write to the European Commission: call for long-duration storage as a strategic asset · LDES Council, 2026-06-03

The LDES Council, with Cleantech for Europe, Energy Storage Europe, Flow Batteries Europe, IHA and others, wrote to the EU energy commissioner asking the Electrification Action Plan to explicitly designate "≥8-hour long-duration storage" as a strategic asset, with four demands: explicit LDES in policy, an EU LDES roadmap, lead markets, and an LDES revenue-certainty mechanism.

→ Implication for PG: Australian and EU storage policy are highly linked; an EU LDES revenue-certainty mechanism would become a reference for Australian LDES policy discussions, opening policy space for non-lithium long-duration routes (vanadium flow, iron-air) — relevant to PG's thinking on a long-duration product mix.

Source: LDES Council joint letter (2026-06-03)

None this issue

No new articles on Sunday (normal). Most recent coverage was 2026-06-05 "Every new NEM solar project submitted for 2027-28 is a hybrid BESS system" (fully reported in Issue 16).

This briefing is auto-compiled daily by the PGSH internal research system, with each item's source labeled and verified under "source discipline" (published within the last 7 days, link opens directly to the original). All project progress, policy, price data, and institutional views are for internal reference only and do not constitute investment, procurement, or business decision advice. If interested in any item or planning to act on it, please open the corresponding source link to verify accuracy and timeliness.