类型:增量 · 覆盖窗口:2026-06-05 ~ 2026-06-06(基线 2026-06-05)

周六。本期核心:PG 双项目里程碑 - Portland Energy Park(VIC,1 GW / 2,500 MWh)获联邦 EPBC 审批清关;Nine Mile BESS(VIC,500 MW / 1,500 MWh,Pacific Green × Green Switch Energy)获 VIC DFP 批准 - 两个 VIC 项目同日进入可开工阶段,Victoria DFP 批次合计约 1,390 MW / AU$24 亿。Waratah Super Battery 恢复 700 MW(HVT2 修复,06-04)。NSW LTESA Tender Round 6 完整名单揭晓(6 个项目,1,171 MW / ~12 GWh)。Modo Energy 确认 NEM 2027-28 所有新提交太阳能项目 100% 为混合 BESS 系统,独立太阳能时代终结。中国供应商本期无新海外公告(SNEC 闭幕后滞后期)。锂价 SMM USD 21,229.46 / CNY 163,000(smm_date 06-05,-3.12%);GFEX 2609 全周 -8.5%,周五尾盘止跌反弹 +1.21%;机构短期区间 CNY 155,000-172,000。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 49 个 ≥100 MWh 项目(本期新增 6 条:Portland Energy Park / Nine Mile BESS / Great Western Battery / Bowmans Creek BESS / Armidale East BESS / Ebor BESS;更新 2 条:Waratah 700 MW 恢复 + Bannaby LTESA 合约容量) - 中国供应商海外项目 · 表 A — 本期无新增;当前 22 条 - 供应商档案 · 表 B — 本期无更新 - 锂价历史 · 表 D — 今日已追加 06-06 行(USD 21,229.46;SMM 最新 Date 6 月 5 日,T-1 正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

Pacific Green Portland Energy Park(VIC,1 GW / 2,500 MWh):获联邦 EPBC 审批清关 · Energy-Storage.news,2026-06-05

Pacific Green 开发的 Portland Energy Park(维多利亚州 Portland,铝冶炼厂旁约 40 公顷工业用地)已通过联邦《环境保护和生物多样性保护法》(EPBC Act)审批,这是澳洲大型 BESS 项目开工前的最后一道联邦监管门槛。

规格:1 GW / 2,500 MWh(4 × 250 MW 储能园区,4 小时时长),总投资约 AU$13 亿(约 US$840M)。

开发时间线: - 首期 S1:250 MW 目标 Q3 2026 上线 - 其余三期:每 6 个月追加 1 期,36 个月内完工 - 供货框架:天合储能(Trina Storage)5 GWh 供货框架协议(2025-11)

此前:VIC DFP 快速规划审批已于 2025-09 完成,本次 EPBC 清关消除最后监管障碍,项目进入工程采购与融资关闭阶段。

→ 对 PG 的影响:Portland Energy Park 是 PG 澳洲旗舰资产,EPBC 清关意味着工程采购可全面推进;Q3 2026 首期 250 MW 并网将是 PG 在 NEM 的首个运营里程碑,是 2026/27 融资故事的核心支撑。SA Limestone Coast + VIC Portland 双线并轨,PG 澳洲管线可见度大幅提升。

来源:Energy-Storage.news(2026-06-05)· 首记 2026-06-06

Nine Mile BESS(VIC,500 MW / 1,500 MWh,Pacific Green × Green Switch Energy):获 VIC DFP 批准 · 维州规划部 PA2504144/PA2504148,2026-05-28

Pacific Green 与本地开发商 Green Switch Energy 的合资项目 Nine Mile BESS,作为本轮 VIC DFP 快速审批批次(2026-06-05 官方发布)的一部分获得规划批准,总投资约 AU$6 亿。

规模与结构: - S1:250 MW / 500 MWh(2h),规划许可 PA2504144 - S2:250 MW / 1,000 MWh(4h),规划许可 PA2504148 - 两期合计:500 MW / 1,500 MWh - 选址:Golden Plains LGA,Barunah Park(Geelong 以西约 50 公里),接入 VIC Western Hub 电网

前置条件:电网连接协议 + 设备采购 + 财务关闭,预计不早于 2026 年底开工。

→ 对 PG 的影响:Nine Mile 是 PG 在 VIC 的第二块布局,与 Portland Energy Park(VIC Portland)形成同州双线部署。若两项目 S1 均按 2026-2027 时间表推进,PG 有望于 2027 年底前在 VIC 实现约 1 GW 运营或在建装机;AU$6 亿规模属于中型项目,JV 结构降低单方开发风险。

来源:VIC 规划部 PA2504144 / PA2504148 · ESN DFP 报道(2026-06-05)· 首记 2026-06-06

VIC DFP 批次审批(2026-06-05 官方发布):4 个项目约 1,390 MW / AU$24 亿 · 维多利亚州政府,2026-06-05

维多利亚州通过 DFP 快速程序批准本轮 4 个可再生与储能项目,合计约 AU$24 亿 总投资(含 Morwell 已于 Issue 15 单独报道):

| 项目 | 开发商 | 规模(储能) | 投资 |

|---|---|---|---|

| Morwell BESS(已于 Issue 15 报道) | TagEnergy | 最高 1,000 MW / 4,000 MWh | AU$13 亿 |

| Nine Mile BESS | Pacific Green × Green Switch | 500 MW / 1,500 MWh | AU$6 亿 |

| Chivers Road BESS(Glenrowan) | Pacific Partnerships | 约 100 MW | AU$1.3 亿 |

| Gelliondale Wind+BESS(Gippsland) | Synergy Wind | 80 MW 风 + 40 MW BESS | AU$3.88 亿 |

DFP 两年内已批准逾 30 个可再生能源项目,VIC 累计批准总投资超 AU$110 亿。

→ 对 PG 的影响:VIC DFP 是澳洲审批最快通道(对比 NSW 中位 614 天),PG 两个 VIC 项目均借助此路径完成州级审批;对比 NSW 竞争对手须经 IPC,PG VIC 资产的开发确定性和时间线更优。VIC 大规模储能密度持续上升,供应链资源(EPC、电网接入槽)抢手,采购前置至关重要。

Waratah Super Battery(NSW):HVT2 修复完成,恢复 700 MW / 1,680 MWh 运营 · Energy-Storage.news,2026-06-05

Akaysha Energy(BlackRock)确认 Waratah Super Battery 第二台高压变压器(HVT2)于 2026-06-04 完成修复并重新上线,系统恢复至 700 MW / 1,680 MWh(占设计额定 850 MW 的 82%): - 350 MW 履行 Transgrid SIPS(系统完整性保护方案)合约义务 - 350 MW 以商业方式参与 NEM 现货市场及 FCAS 辅助服务

全量 850 MW 恢复仍需等待 HVT3 交付(Wilson Transformer Company 制造中),预计 2026 年 Q3 到货,年底前实现满额 SIPS 履约。此前 AER 因容量延误已削减合同赔付逾 AU$9,000 万(SIPS 最终总额调整至 AU$512.6M)。

→ 对 PG 的影响:350 MW 商业容量重入 NEM 将对 NSW 区域 FCAS 及现货套利产生边际价格压力;Waratah SIPS 合约结构(容量合同+套利混合)是 PG 大型项目合同谈判的重要参考样本。

来源:Energy-Storage.news(2026-06-05)

NSW LTESA Tender Round 6 完整授标名单:6 个项目,1,171 MW / 11,980 MWh(约 12 GWh) · ASL,2026 年授标(本期补全全貌,Issue 15 仅单独报道 Kingswood)

NSW 消费者受托人 ASL 完成 LTESA Tender Round 6(目标 ≥8 小时长时储能)全部 6 个项目授标,总合计超出目标:

| 项目 | 开发商 | 规模 | 时长 | 备注 |

|---|---|---|---|---|

| Great Western Battery | Neoen Australia | 330 MW / 3,500 MWh | 10.6h | Tender 6 最大单项 |

| Bannaby BESS | BW ESS Australia | 233 MW / 2,676 MWh | 11.5h | 全场规划约 700-750 MW,LTESA 合约容量 233 MW |

| Bowmans Creek BESS | Ark Energy | 250 MW / 2,414 MWh | 9.7h | - |

| Armidale East BESS | FRV Services Australia | 158 MW / 1,440 MWh | 9.1h | - |

| Kingswood BESS | Iberdrola Australia | 100 MW / 1,080 MWh | 10.8h | 已于 Issue 15 报道(双批获批) |

| Ebor BESS | Bridge Energy | 100 MW / 870 MWh | 8.7h | Energy Vault B-VAULT 技术,澳洲首次落地;AU$3.1 亿;COD 2028 |

| 合计 | 1,171 MW / 11,980 MWh | 8.7-11.5h | 超目标 ~17% |

NSW LTESA 2030 目标(2 GW / 16 GWh)经本轮授标后已完成约 75%。Ebor BESS 是 Energy Vault 重力储能(B-VAULT 模块化方案)首次在澳洲获得 LTESA 合约。

→ 对 PG 的影响:Round 6 全部 6 个项目均超过 8.7 小时,验证 NSW 政策偏好 LDES;竞争者格局:Neoen(330 MW)、BW ESS(233 MW)、Iberdrola(100 MW)是 NSW LTESA 主要对手。NSW LTESA Tender Round 7(Tender 9,目标 12 GWh,≥8h)注册截止 2026-06-22,PG 须本周内确认是否注册。

QLD 北部能源基金(NWEF):AU$2 亿正式开放提案征集 · QIC,2026-06-02

QIC 正式开放 North West Energy Fund(NWEF),专项服务 QLD 西北矿业区(Mount Isa / Cloncurry / Julia Creek / Richmond),支持类型含 BESS、太阳能、风能: - 商运截止:2030 年 - 背景:CopperString 输电线造价从 AU$18 亿飙升至 AU$136 亿,LNP 政府缩减规划,NWEF 作为离网过渡方案填补供电缺口

→ 对 PG 的影响:PG 的 ARENA 离网卡车充电项目(fuel cells + LFP + PV 三元微网)若落点 QLD 西北矿业区,NWEF 是可直接对接的政府联合投资渠道,值得评估申请资格。

来源:PV Magazine Australia(2026-06-02)

AER Solar Sharer Offer(07-01 生效):NSW / SE-QLD / SA 日内免费用电窗口 · AER,2026-05-26 公告,2026-07-01 生效

AER DMO 8 最终决定确认 Solar Sharer Offer(SSO) 于 2026-07-01 正式生效(opt-in,适用所有安装智能电表居民): - 范围:NSW、昆州东南部(SE-QLD)、SA - 机制:每日 11:00-14:00 用电免费(午间光伏过剩引导需求消纳) - 套利影响:午间 BESS 收益进一步压缩,价值向傍晚-夜间峰时转移;4 小时以上 BESS 受影响较小

→ 对 PG 的影响:SSO 结构性压低 11am-2pm 价差,进一步支持 LTESA/CIS 合约底托的必要性;Portland(4h)等大型 BESS 有足够充放电窗口规避影响。

来源:AER SSO 事实页(2026-05-26)

AEMC 消费者能源资源调度规则(IPRR):2026-11-05 生效 · AEMC,规则已最终确定

AEMC《Integrating Price-Responsive Resources into the NEM》最终规则于 2026-11-05 生效:VPP 聚合商升级为注册 NEM 参与方,家用 BESS 通过聚合商正式接入 5 分钟实时市场价格信号(上限 AU$16,600/MWh);2027-02 起开放早期参与招募。

→ 对 PG 的影响:分布式 VPP 规模化可能分流电网侧 FCAS 收入,长期值得关注;短期(2026-2027)影响有限。

来源:AEMC IPRR

CIS Tender 8(4 GW / 16 GWh):截至 2026-06-06 仍未授标 · DCCEEW,持续跟踪

DCCEEW 官网截至本期仍显示"Bids currently being assessed",官方预期"2026 年 6 月公布"窗口有效;本周(06-01 至 06-06)未落地。本月余下三周仍在观察窗口内。

→ 对 PG 的影响:Tender 8 结果公布后直接校准 PG Tender 10 竞价策略与区域优先级,须第一时间关注。

今日无新增

SNEC 2026(上海,06-03/05)闭幕后,Watchlist 各供应商展后合同公告通常有 2-5 个工作日滞后。截至本期(北京时间 2026-06-06 早),CATL / BYD / EVE / Hithium / Envision / Sungrow / Trina / REPT / CORNEX / HyperStrong 十家供应商均未发出 ≥100 MWh 新海外项目公告。预计 6 月 9 日(周一)起陆续披露。

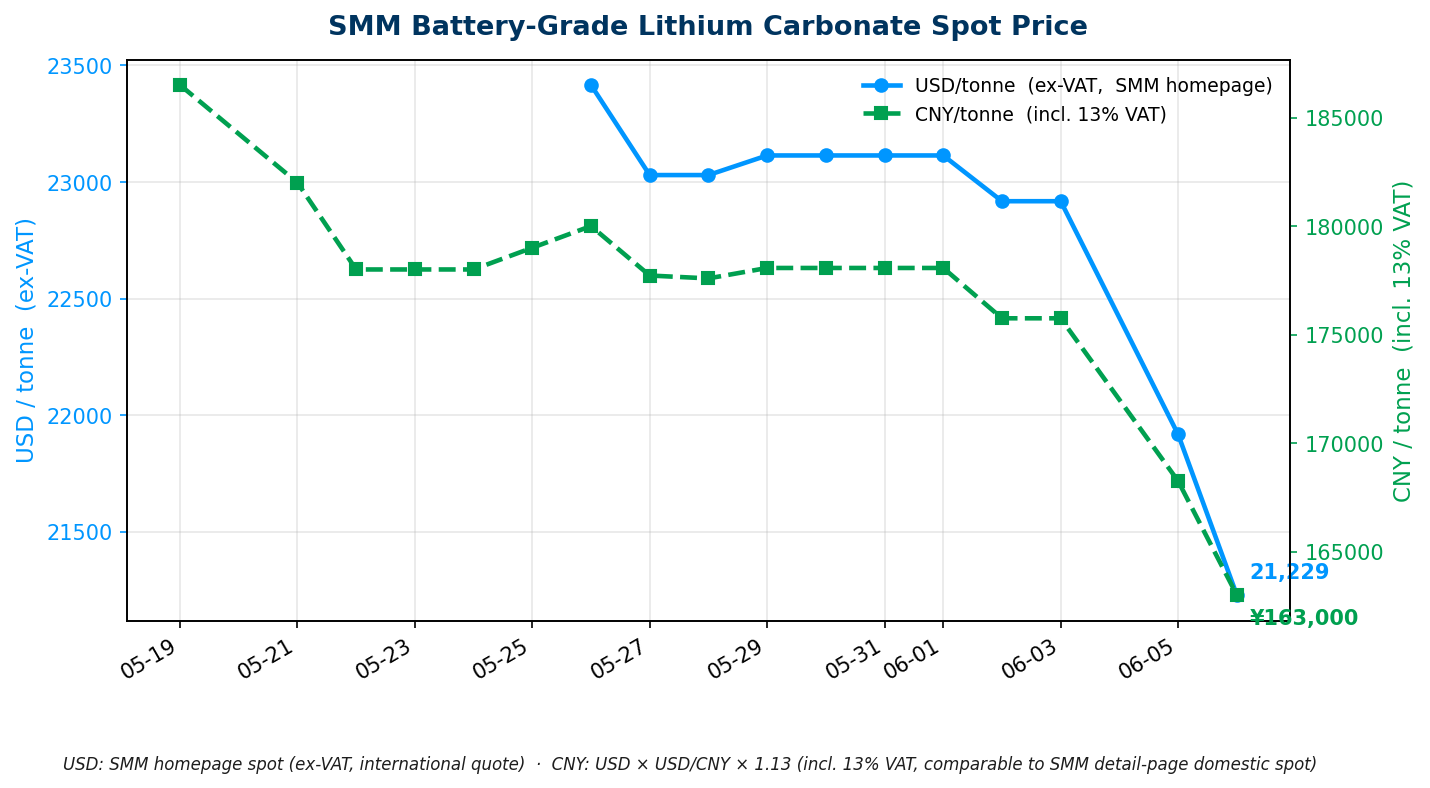

今日价格(口径:2026-06-06 北京时间 07:00 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 21,229.46 / tonne(-688.61,-3.12%) / CNY 163,000 / 吨 | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 5 日(SMM 约 10:10 发当日值,7:00 抓为 T-1 是正常;周六休市 SMM 不更新);CNY 含 13% VAT 官方精确均价 |

走势分析:全周跌幅 -8.5%,周五尾盘技术止跌反弹

GFEX 主力合约 LC2609 本周(第 23 周)累计跌幅 -8.5%。06-05(周五)盘中大幅低开至约 CNY 160,000/吨后尾盘技术反弹,最终收涨 +1.21%(CNY 164,360),持仓量增加 8,061 手,反映部分资金低位建仓;现货端延续下行(CNY 163,000,-2,000),期现分化延续。

三重叠压:仓单 + 产量 + 淡季需求(机构综合,06-05)

① GFEX 仓单超预期累库:截至 06-01,仓单约 55,215 手(≈5.5 万吨),中粮期货预计下周突破 6 万手;大量贸易商将现货注册入仓,持续打压期货; ② 5 月产量大幅放量(约 62,100 吨,+27.9% MoM):青海盐湖厂产季爬产、江西省前期环保影响消退;Mysteel 预计 6 月产量续增约 3.8%; ③ 月初现货成交清淡:动力电芯淡季买盘薄弱,储能电芯出口抢装对冲后整体偏弱。

机构短期观点

矿端关键节点(Q3 观察)

→ 对 PG 的影响:现货 CNY 163,000 较本轮高点(约 CNY 180,000)回撤约 10%;卓创 / 长江有色的 CNY 155,000-165,000 磨底区间成立的话,当前价位已接近底部上沿。PG 采购框架锁价时点(以 MinRes Bald Hill 7 月首产数据落地后为宜)维持不变,同步关注 CATL 枧下窝 6 月 30 日申请结果。

来源:卓创资讯、中粮期货、长江有色金属网、大地期货(财联社引述,2026-06-05);完整台账见 活表 D

Invinity × FlexBase:2.1 GWh 钒液流电池(VRFB)专为 AI 数据中心设计,欧洲首例 GWh 级 VRFB AIDC 项目 · Energy-Storage.news,2026-06-04

英国-加拿大 VRFB 公司 Invinity Energy Systems 赢得瑞士 FlexBase 集团 Technology Centre Laufenburg 项目储能供应商竞选:初期 1.5 GWh,扩展至 2.1 GWh(全量阶段);应用:AI 数据中心园区 + 电网稳定(瑞士-德国边境 Laufenburg)。

FlexBase CEO Marcel Aumer 的选择依据:最低全生命周期成本(LCOS)+ 不可燃性 + >20 年循环稳定寿命。这是全球首个在 GWh 规模上、专为 AIDC 设计并与 LFP 正面竞争的 VRFB 项目,以安全性与长寿命胜出。进展:2025-05 破土,Invinity 进入工程设计阶段(2026-2027)。

→ 对 PG 的影响:AIDC 客户对不可燃、长寿命储能存在独特偏好,VRFB 与 LFP 形成技术互补;PG 聚焦 LFP,但在欧洲或 AIDC 场景中,VRFB 合作渠道值得评估以覆盖安全监管敏感市场。

来源:Energy-Storage.news(2026-06-04)

LFP 电芯现货参考价:CEEC 7 GWh 集采底价 ¥0.34/Wh(约 US$47/kWh) · 中国能建集团工程,2026-05-07 公示

中国国家能源集团工程公司(CEEC)5 月 7 日完成 7 GWh 储能电芯集采,最低中标价 ¥0.34/Wh(约 US$47/kWh)(314 Ah 包),区间 ¥0.34-0.394/Wh;≥500 Ah 包底价 ¥0.360/Wh。BNEF 预计 2026 年全球工程系统装机成本 US$210-390/kWh installed。

→ 对 PG 的影响:US$47/kWh 电芯单价意味着 Portland Energy Park 2.5 GWh 电芯采购约 AU$1.8 亿(占 AU$13 亿总投资约 14%);BOS 工程才是成本主体,本地 EPC 能力与采购条款是 CAPEX 控制核心杠杆。

「每一个 2027-28 年新提交 NEM 太阳能项目都是混合系统」:独立太阳能时代终结 · Modo Energy,2026-06-05(9 分钟深度分析)

Modo Energy 证实一个结构性转折点已发生:NEM 所有 2027-28 年已确认(Committed)和预计(Anticipated)阶段的新建公用事业规模太阳能项目,100% 为 BESS 混合系统(唯一例外 Aramara QLD 140 MW 属 2018 年遗留许可,已无实质推进)。

经济学转折点:太阳能 LCOE 三年下降 14%,但商业收益 /MWh 因"价格时段套利折扣(price cannibalisation)"同期下跌 71% - 成本降速远不及收益降速,独立太阳能融资案例已无法成立。BESS 通过以下机制维持太阳能项目可融资性:午间低价电搬移至傍晚峰时、共享电网连接提升接入效率、MLF 优化、构网型系统强度服务资格。

区域价格展望(Modo 预测): - SA 和 VIC:太阳能小时价格预期见底并回升(BESS 装机+煤电退役+数据中心需求) - QLD 和 NSW:价格降幅趋平,但无显著回升预期(储能装机增速较慢,煤电延退)

管线结构:Committed+Anticipated 混合太阳能管线 8.8 GW,全部为混合系统;DC 耦合设计在明确声明的开发商中最为普遍(2027 年起),共享逆变器允许太阳能超配提升收益。

2026 年节点:1.7 GW 现有独立太阳能场正在加装 BESS 改造(Limondale、New England、Broadsound、Culcairn、Gunsynd);2026 年至今 BESS 委托量是太阳能的 4.3 倍。

→ 对 PG 的影响:独立 BESS(非混合系统)在 SIPS / FCAS / CIS 合约层面仍有独立经济逻辑,与混合太阳能互补而非竞争;Modo 数据证明 BESS 已成为太阳能项目融资的必要前提。PG 若布局 DC 耦合混合系统场景(如 Nine Mile),可借助此结构提升银行可融资性。Portland Energy Park 等纯储能项目仍依托 CIS/LTESA 合约获得独立融资基础。

来源:Modo Energy(2026-06-05)

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental · Coverage Window: 2026-06-05 ~ 2026-06-06 (Baseline: 2026-06-05)

Saturday. Key highlights this issue: PG dual-project milestones - Portland Energy Park (VIC, 1 GW / 2,500 MWh) clears final federal EPBC hurdle; Nine Mile BESS (VIC, 500 MW / 1,500 MWh, Pacific Green × Green Switch Energy) secures VIC DFP approval - both VIC projects entering construction-ready stage on the same day, with the VIC DFP batch totalling approximately 1,390 MW / AU$2.4 billion. Waratah Super Battery restored to 700 MW (HVT2 repaired, 06-04). NSW LTESA Tender Round 6 full results released (6 projects, 1,171 MW / ~12 GWh). Modo Energy confirms 100% of 2027-28 committed NEM solar projects are now BESS hybrids - the era of standalone solar has ended. No new Chinese supplier announcements this issue (post-SNEC lag period). Lithium: SMM USD 21,229.46 / CNY 163,000 (smm_date 06-05, -3.12%); GFEX LC2609 weekly decline -8.5%, Friday close technical rebound +1.21%; institutional short-term range CNY 155,000-172,000.

Supporting live tables (continuously updated by daily routine): - Australia Projects BOM · Table C — 49 projects ≥100 MWh (6 new entries this issue: Portland Energy Park / Nine Mile BESS / Great Western Battery / Bowmans Creek BESS / Armidale East BESS / Ebor BESS; 2 updated: Waratah 700 MW restored + Bannaby LTESA contract capacity) - China Suppliers Overseas Projects · Table A — No new entries this issue; currently 22 entries - Supplier Profiles · Table B — No updates this issue - Lithium Price History · Table D — 06-06 row appended (USD 21,229.46; SMM latest date June 5, T-1 normal); chart regenerated

Full project supply chain BOM: Live Table C.

Pacific Green Portland Energy Park (VIC, 1 GW / 2,500 MWh): Clears Federal EPBC Approval · Energy-Storage.news, 2026-06-05

Pacific Green's Portland Energy Park (Victoria, approximately 40 hectares of industrial land adjacent to the Portland aluminium smelter) has cleared Australia's federal Environment Protection and Biodiversity Conservation Act (EPBC Act) assessment - the final federal regulatory gate before construction can commence.

Specifications: 1 GW / 2,500 MWh (4 × 250 MW battery parks, 4-hour duration), total investment approximately AU$1.3 billion (~US$840M).

Development timeline: - Stage 1: 250 MW targeting Q3 2026 commissioning - Remaining three stages: one added every 6 months, completed within 36 months - Supply framework: 5 GWh supply framework agreement with Trina Storage (Nov 2025)

Previous milestone: VIC DFP fast-track planning approval completed September 2025. EPBC clearance removes the final regulatory obstacle, advancing the project into procurement and financial close.

→ For PG: Portland Energy Park is PG's flagship Australian asset. EPBC clearance means full procurement can commence; the Q3 2026 Stage 1 commissioning will be PG's first operating NEM asset milestone - the cornerstone of the 2026/27 financing narrative. SA Limestone Coast + VIC Portland running in parallel materially increases PG's Australian pipeline visibility.

Source: Energy-Storage.news (2026-06-05) · First recorded 2026-06-06

Nine Mile BESS (VIC, 500 MW / 1,500 MWh, Pacific Green × Green Switch Energy): Secures VIC DFP Approval · Victoria Planning Authority PA2504144/PA2504148, 2026-05-28

Pacific Green and local developer Green Switch Energy's joint venture, Nine Mile BESS, received planning approval under Victoria's Development Facilitation Program (DFP), as part of the batch announcement on 2026-06-05. Total investment approximately AU$600 million.

Scale and structure: - Stage 1: 250 MW / 500 MWh (2h), Permit PA2504144 - Stage 2: 250 MW / 1,000 MWh (4h), Permit PA2504148 - Combined two stages: 500 MW / 1,500 MWh - Location: Golden Plains LGA, Barunah Park (~50 km west of Geelong), connecting to VIC Western Hub

Pre-conditions for construction: grid connection agreement + equipment procurement + financial close; construction expected no earlier than end of 2026.

→ For PG: Nine Mile is PG's second VIC foothold, forming a dual-project deployment alongside Portland Energy Park. If both Stage 1s proceed on the 2026-2027 timeline, PG could have approximately 1 GW of operating or under-construction capacity in VIC by end of 2027. The JV structure reduces single-party development risk.

Source: VIC Planning Authority PA2504144/PA2504148 · ESN DFP report (2026-06-05) · First recorded 2026-06-06

VIC DFP Batch Approval (announced 2026-06-05): 4 Projects, ~1,390 MW / AU$2.4 Billion · Victoria State Government, 2026-06-05

Victoria's Planning Minister Sonya Kilkenny announced approval for four projects under DFP fast-track, totalling approximately AU$2.4 billion (including Morwell, already reported in Issue 15):

| Project | Developer | Storage Capacity | Investment |

|---|---|---|---|

| Morwell BESS (reported in Issue 15) | TagEnergy | up to 1,000 MW / 4,000 MWh | AU$1.3B |

| Nine Mile BESS | Pacific Green × Green Switch | 500 MW / 1,500 MWh | AU$600M |

| Chivers Road BESS (Glenrowan) | Pacific Partnerships | ~100 MW | AU$130M |

| Gelliondale Wind+BESS (Gippsland) | Synergy Wind | 80 MW wind + 40 MW BESS | AU$388M |

DFP has now approved over 30 projects in two years; Victoria's cumulative renewable and storage infrastructure approvals exceed AU$11 billion.

→ For PG: VIC DFP is Australia's fastest approval pathway (vs. NSW IPC median of 614 days). Both PG VIC projects have used this route; the development certainty and timeline advantage over NSW-based competitors is significant. As VIC BESS density continues rising, supply chain resources (EPC, grid capacity) are tightening - early procurement is critical.

Waratah Super Battery (NSW): HVT2 Repaired, Restored to 700 MW / 1,680 MWh · Energy-Storage.news, 2026-06-05

Akaysha Energy (BlackRock) confirmed that Waratah Super Battery's second high-voltage transformer (HVT2) was repaired and returned to service on 2026-06-04, restoring the system to 700 MW / 1,680 MWh (82% of the designed 850 MW rating): - 350 MW: fulfilling Transgrid SIPS (System Integrity Protection Scheme) contract obligations - 350 MW: participating commercially in NEM spot market and FCAS ancillary services

Full 850 MW restoration awaits HVT3 delivery (Wilson Transformer Company manufacturing), expected Q3 2026, with full SIPS contract compliance targeted by year-end. AER has cut contract payments by over AU$90 million due to capacity delays (SIPS final total adjusted to AU$512.6M).

→ For PG: The return of 350 MW of commercial capacity to NSW will exert marginal downward pressure on FCAS and spot arbitrage revenues in the region. Waratah's SIPS contract structure (capacity contract + arbitrage hybrid) remains the most important benchmark for large-scale BESS contract negotiation in Australia.

Source: Energy-Storage.news (2026-06-05)

NSW LTESA Tender Round 6 Full Results: 6 Projects, 1,171 MW / 11,980 MWh (~12 GWh) · ASL, awarded 2026 (full picture; Issue 15 only reported Kingswood)

ASL completed all awards under NSW LTESA Tender Round 6 (target: ≥8-hour long-duration storage), exceeding the target by approximately 17%:

| Project | Developer | Capacity | Duration | Notes |

|---|---|---|---|---|

| Great Western Battery | Neoen Australia | 330 MW / 3,500 MWh | 10.6h | Largest Round 6 award |

| Bannaby BESS | BW ESS Australia | 233 MW / 2,676 MWh | 11.5h | Full site planned ~700-750 MW; LTESA contracted at 233 MW |

| Bowmans Creek BESS | Ark Energy | 250 MW / 2,414 MWh | 9.7h | - |

| Armidale East BESS | FRV Services Australia | 158 MW / 1,440 MWh | 9.1h | - |

| Kingswood BESS | Iberdrola Australia | 100 MW / 1,080 MWh | 10.8h | Reported in Issue 15 (dual approvals secured) |

| Ebor BESS | Bridge Energy | 100 MW / 870 MWh | 8.7h | Energy Vault B-VAULT technology; first Australia deployment; AU$3.1B; COD 2028 |

| Total | 1,171 MW / 11,980 MWh | 8.7-11.5h |

Round 6 completes approximately 75% of NSW's 2030 target (2 GW / 16 GWh). Ebor BESS marks Energy Vault's first commercial deployment in Australia.

→ For PG: All 6 Round 6 projects exceed 8.7 hours - NSW policy is firmly locked into LDES (long-duration energy storage). Key competitors in this space: Neoen (330 MW), BW ESS (233 MW), Iberdrola (100 MW). NSW LTESA Tender Round 7 (Tender 9, target 12 GWh, ≥8h) registration closes 2026-06-22 - PG must determine registration eligibility this week.

Source: ASL NSW LTESA Tender 6 results

QLD North West Energy Fund (NWEF): AU$200M Proposals Now Open · QIC, 2026-06-02

QIC formally opened the North West Energy Fund (NWEF) for proposals, targeting QLD's northwest mining region (Mount Isa / Cloncurry / Julia Creek / Richmond). Eligible project types include BESS, solar, wind: - Commercial operation deadline: 2030 - Context: CopperString transmission line budget escalated from AU$1.8B to AU$13.6B; LNP government scaled back to a 330kV line; NWEF bridges the gap with off-grid solutions

→ For PG: PG's ARENA off-grid truck charging project (fuel cells + LFP + PV tri-hybrid microgrid) may qualify if sited in QLD's northwest mining region. NWEF is a direct government co-investment channel worth evaluating for eligibility.

Source: PV Magazine Australia (2026-06-02)

AER Solar Sharer Offer (effective 07-01): Free Electricity 11am-2pm in NSW / SE-QLD / SA · AER, announced 2026-05-26, effective 2026-07-01

AER DMO 8 final determination confirms the Solar Sharer Offer (SSO) takes effect 2026-07-01 (opt-in for all smart meter customers): - Scope: NSW, South-East Queensland (SE-QLD), SA - Mechanism: free electricity every day 11:00-14:00 (designed to absorb midday solar surplus) - BESS arbitrage impact: midday spreads compressed further; arbitrage value shifts toward evening-to-night peak hours; BESS assets with ≥4h duration are less affected

→ For PG: SSO structurally reduces 11am-2pm price spreads, further supporting the necessity of LTESA/CIS contract revenue floors. Portland Energy Park (4h) and other large BESS assets have sufficient charge-discharge windows to absorb the impact.

Source: AER SSO Fact Sheet (2026-05-26)

AEMC Consumer Energy Resources Dispatch Rule (IPRR): Effective 2026-11-05 · AEMC, rule finalised

AEMC's Integrating Price-Responsive Resources into the NEM final rule takes effect 2026-11-05: VPP aggregators upgraded to registered NEM participants; residential BESS (home batteries, EVs) formally connected to the 5-minute real-time market price signal (cap AU$16,600/MWh) via aggregators; early participation recruitment opens from 2027-02.

→ For PG: Distributed VPP scaling may gradually erode grid-scale FCAS revenues; short-term (2026-2027) impact limited. Grid-scale and distributed-scale BESS operate in distinct market tiers.

Source: AEMC IPRR

CIS Tender 8 (4 GW / 16 GWh): Still Unannounced as of 2026-06-06 · DCCEEW, ongoing monitoring

DCCEEW's website continues to show "Bids currently being assessed" as of this issue. The official guidance of "June 2026 announcement" remains valid; no announcement was made during the week of 06-01 to 06-06. Three weeks of the official announcement window remain.

→ For PG: Once Tender 8 results land, the regional distribution of 16 GWh of contracts will directly calibrate PG's Tender 10 bidding strategy and regional development priorities.

Australia projects: Live Table C; non-Australia projects: Live Table A; supplier profiles: Live Table B.

No New Entries This Issue

Following SNEC 2026 (Shanghai, 06-03/05), post-show contract announcements typically lag by 2-5 business days. As of this issue (Beijing time 06-06 morning), none of the Watchlist 10 suppliers (CATL / BYD / EVE / Hithium / Envision / Sungrow / Trina / REPT / CORNEX / HyperStrong) have issued new overseas project announcements ≥100 MWh. Expect announcements beginning Monday 09 June.

Today's Price (captured Beijing time 07:00, 2026-06-06)

| Commodity | Latest Price | Notes |

|---|---|---|

| Battery-Grade Lithium Carbonate (SMM) | USD 21,229.46 / tonne (-688.61, -3.12%) / CNY 163,000 / tonne | SMM-Li-LC-001 Avg; SMM latest date June 5 (SMM updates ~10:10am Beijing, 7:00am capture is T-1 normal; Saturday - SMM does not update); CNY includes 13% VAT, official precise average |

Market Analysis: -8.5% Weekly Decline, Friday Technical Rebound

GFEX front-month contract LC2609 declined -8.5% for the week (Week 23, 2026). On 06-05 (Friday), the contract opened sharply lower at approximately CNY 160,000/tonne before a technical rebound, closing up +1.21% at CNY 164,360 with open interest increasing by 8,061 lots - reflecting some bottom-fishing activity. Spot prices continued declining (CNY 163,000, -2,000), with futures/spot divergence persisting.

Three Compounding Downward Pressures (institutional consensus, 06-05)

① GFEX warehouse warrant accumulation beyond expectations (55,215 lots ≈ 55,000 tonnes as of 06-01): CITIC Futures forecasts a breach of 60,000 lots next week; large volumes of physical material being registered as exchange warrants applies sustained pressure; ② May production surged (~62,100 tonnes, +27.9% MoM): Qinghai salt lake producers ramping up for their production season, Jiangxi environmental restrictions easing; Mysteel forecasts June production +3.8% MoM; ③ Slow spot activity at month-open: EV battery demand subdued (seasonal lull); battery storage cell export pull-forward provides partial offset but net effect remains weak.

Institutional Short-term Views

Key Mining Milestones (Q3 Watch)

→ For PG: At CNY 163,000, spot prices have retreated ~10% from the recent high (~CNY 180,000); if the CNY 155,000-165,000 floor range holds, current levels approach the upper end of the bottom zone. PG's procurement timing guidance (lock in after MinRes Bald Hill July first-ore data) remains unchanged; monitor CATL Jianxiawo's 30-June application outcome.

Sources: Zhuochuang Consulting, COFCO Futures, Yangtze Nonferrous Metals, Daditai Futures (via Cailian Press, 2026-06-05); full ledger: Live Table D

Invinity × FlexBase: 2.1 GWh Vanadium Flow Battery (VRFB) Purpose-Built for AI Data Centre - Europe's First GWh-Scale VRFB AIDC Project · Energy-Storage.news, 2026-06-04

UK-Canadian VRFB company Invinity Energy Systems won the storage supplier selection for Swiss company FlexBase Group's Technology Centre Laufenburg project: initial phase 1.5 GWh, expanding to 2.1 GWh (full stage). Application: AI data centre campus + grid stability (Laufenburg, Swiss-German border).

FlexBase CEO Marcel Aumer's selection criteria: lowest lifecycle cost (LCOS) + non-flammability + >20-year cycle stability. This is the world's first GWh-scale VRFB project specifically designed for AIDC - winning head-to-head against LFP on safety and longevity grounds. Status: broke ground May 2025; Invinity in detailed engineering phase (2026-2027).

→ For PG: AIDC clients have a distinct preference for non-flammable, long-life storage - VRFB is complementary to LFP rather than directly competitive. PG focuses on LFP, but VRFB partnerships are worth evaluating for European AIDC projects or markets with strict fire safety regulations.

Source: Energy-Storage.news (2026-06-04)

LFP Cell Spot Reference Price: CEEC 7 GWh Tender Low-Bid ¥0.34/Wh (~US$47/kWh) · CEEC, public announcement 2026-05-07

China Energy Engineering Corporation (CEEC) completed a 7 GWh storage cell tender on 07 May with a lowest bid of ¥0.34/Wh (~US$47/kWh) (314 Ah package), range ¥0.34-0.394/Wh; ≥500 Ah package low bid ¥0.360/Wh. BNEF estimates 2026 global utility-scale installed system cost at US$210-390/kWh installed.

→ For PG: At US$47/kWh cell cost, Portland Energy Park's 2.5 GWh cell procurement equates to approximately AU$180 million (~14% of AU$1.3B total investment); BOS engineering dominates total cost. Local EPC capability and contract terms are the key CAPEX control levers.

"Every New 2027-28 Committed NEM Solar Project Is a Hybrid": The Era of Standalone Solar Is Over · Modo Energy, 2026-06-05 (9-minute deep-dive)

Modo Energy has confirmed a structural inflection point: in the NEM, 100% of Committed and Anticipated utility-scale solar projects planned for 2027-28 are paired with BESS as hybrid systems. The only exception, Aramara (QLD, 140 MW), is a 2018 legacy permit with no public progress since a 2018 investor sale and should be read as an artefact rather than a live signal.

The economics have turned: Solar LCOE has fallen 14% over three years, but merchant revenue per MWh has fallen 71% due to "price cannibalisation" (time-of-day shape discounts). The cost-to-revenue ratio has worsened even as costs fall. BESS restores bankability through: shifting cheap midday solar to evening peaks, maximising grid connection utilisation, improving MLF (marginal loss factors), and qualifying for grid-forming system strength services.

Regional price outlook (Modo forecast): - SA and VIC: solar-hour prices expected to bottom out and recover (BESS absorbing midday surplus + coal retirements + data centre demand growth) - QLD and NSW: price declines plateauing, but no material recovery expected (slower BESS build-out, coal stays online longer)

Pipeline structure: Committed + Anticipated solar pipeline totals 8.8 GW, all hybrid; DC-coupled configurations are the most common among developers who have declared a coupling type - DC-coupling arrives at scale from 2027, with shared inverters enabling solar oversizing.

2026 transition: 1.7 GW of existing standalone solar is being retrofitted with BESS (Limondale, New England, Broadsound, Culcairn, Gunsynd); year-to-date 2026, BESS commissioning runs at 4.3 times the rate of solar commissioning.

→ For PG: Standalone BESS (non-hybrid) retains an independent economic case through SIPS / FCAS / CIS contracts - it is complementary to hybrid solar rather than competing with it. Modo's data confirm that BESS has become a prerequisite for solar project financing. For PG's Nine Mile BESS JV (DC-coupled potential), this hybrid structure would enhance bankability. Portland Energy Park's pure storage positioning can still secure independent financing through CIS/LTESA contract floors.

Source: Modo Energy (2026-06-05)

This research brief is compiled daily by PGSH's internal research system, with each entry sourced and attributed. The project developments, policy updates, price data, and institutional views presented are for internal reference only and do not constitute investment, procurement, or commercial decision advice. For any item of interest or if you intend to act on any finding, please open the corresponding source link directly to verify the accuracy and timeliness of the information.