类型:增量 · 覆盖窗口:2026-06-03 ~ 2026-06-05(基线 2026-06-03)

周五。本期核心:Modo Energy 数据显示 NEM 电网级 BESS 5 月收益跌至 $29k/MW/year 历史最低(同比 -69%,较 4 月 -45%),2 小时价差同比腰斩 65%,全 merchant 模式下 BESS 的融资可行性再度严峻;TagEnergy Morwell BESS(VIC,最高 1,000 MW / 4,000 MWh)获维州规划批准,投资约 AU$13 亿;NSW LTESA Tender 9(12 GWh,≥8 小时长时储能)注册窗口已开,截止 2026-06-22;Kingswood BESS(NSW,100 MW / 1,080 MWh,Iberdrola)完成州批+联邦 EPBC 双重获批(EPBC 仅耗时 7 周);昆士兰 LNP 政府召回 6 个风电及 BESS 项目,QLD 开发风险进一步上升。SNEC 2026(上海,06-03/05)技术端:Hithium 发布 ∞Cell 1300Ah 原生 8 小时 LDES 系统(单箱 6.9 MWh);IEA 确认澳洲 2025 年储能新增近 9 倍至约 8 GW,可调度容量占比 18% 位居全球最高。锂价 SMM USD 21,918.07 / CNY 168,250(SMM Date 6 月 4 日,T-1 正常;GFEX 仓单创历史新高压制期货,但机构认为当前回调非趋势逆转)。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 43 个 ≥100 MWh 项目(本期新增 2 条:Morwell BESS 获维州批 + Kingswood BESS 双批获批) - 中国供应商海外项目 · 表 A — 本期新增 2 条(Trina 日本九州 160 MWh + Hithium 越南 DSS Solar 1 GWh 框架);当前 22 条 - 供应商档案 · 表 B — 本期更新 3 家(CATL 战略目标 / Trina 日本市场 / Hithium 东南亚+SNEC 新品) - 锂价历史 · 表 D — 今日已追加 06-05 行(USD 21,918.07;SMM 最新 Date 6 月 4 日,T-1 正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

TagEnergy Morwell BESS(VIC,最高 1,000 MW / 4,000 MWh):获维州规划批准,总投资约 AU$13 亿 · RenewEconomy,2026-06-04

TagEnergy(葡萄牙清洁能源商,2025 年中期从澳本土开发商 Ace Power 收购该项目)获得维多利亚州交通规划厅批准,Morwell BESS 最高 1,000 MW / 4,000 MWh(4 小时),总投资约 AU$13 亿,选址 Hazelwood North,毗邻 500 kV Hazelwood Terminal Station,电网接入条件属澳洲最优等级。

开发时间线:电网接入协议谈判约需 12 个月;Financial Close 目标 2027 年底;建设周期 18-24 个月;COD 目标 2029 年底。项目位于 Latrobe Valley,即维州煤电主要退役区,TagEnergy 同时在建 Golden Plains 风电场(1.33 GW,全澳最大),具备大型项目工程管理经验。

→ 对 PG 的影响:VIC 再添 GW 级批复,澳洲已全面进入"GW 尺度"储能时代。Latrobe Valley 接入点竞争已趋激烈,TagEnergy 以外资身份快速收购并扩容是欧洲开发商切入澳洲的标准路径。PG 若布局 VIC,需将变电站容量作为选址首要筛查指标。

来源:RenewEconomy(2026-06-04)

Kingswood BESS(NSW,100 MW / 1,080 MWh,Iberdrola):EPBC + NSW IPC 全部获批,仅待 Transgrid 接入 · RenewEconomy,2026-06-04

Iberdrola 位于 Tamworth 东南 6 公里的 Kingswood BESS(100 MW / 1,080 MWh,约 10.8 小时,NSW LTESA Tender 6 ≥8 小时长时储能合同)已完成:①NSW 州规划 IPC 审查(2025-12 通过,含 50+ 份社区异议);②联邦 EPBC 仅耗时 7 周获批(2026-05 底,认定"不受控行动")。目前唯一剩余前置条件为与 Transgrid 达成并网协议,2026 年内预计开工建设。

项目原设计为 270 MW,为竞得 NSW Tender 6 LTESA 而削减至 100 MW(2026-02 获授标)。Tamworth 变电站周边已形成储能集聚区:Equis Australia Calala(250 MW/500 MWh,在建)、Valent Energy Tamworth(200 MW/400 MWh)及 Trinasolar Burgmanns(200 MW/400-800 MWh)均在同区域推进。

→ 对 PG 的影响:IPC 审查路径下,超 50 份异议的项目仍可走通(Kingswood 历时约 14 个月 IPC + 7 周 EPBC);但 EPBC 7 周极速通关模式说明联邦审批对 LTESA 项目存在"绿色通道"效应。Tamworth 接入容量趋于饱和,NSW 内陆新项目选址须提前核查变电站容量余量。

来源:RenewEconomy(2026-06-04)

Recharge Power × Energy Decarb JV:台湾储能系统商首进澳洲,初始管线 128 MW / 292 MWh · Energy-Storage.news,2026-06-04

台湾储能系统开发商 Recharge Power(台湾累计部署超 1 GWh,持有台湾首个 AFC 自动频率控制等多项本土纪录)与昆州本地开发商 Energy Decarb 成立合资公司正式进入澳洲市场。JV 结构:Recharge Power 提供自主 EMS 软件+系统集成(工程、施工、长期运维),Energy Decarb 提供本地项目开发资源+电力市场交易能力,锚定投资方为 St Baker Capital(Trevor St Baker AO,前 ERM Power 创始人)。

初始确定管线:128 MW / 292 MWh,计划两年内分批交付。据报道澳洲已跃升为全球第三大公用事业级储能市场,2025 年 FID 项目达 4.3 GW,BESS 在 Q1 2026 NEM 定价占比达 32%(超越水电)。

→ 对 PG 的影响:海外 BESS 开发商以 JV + 本地合作伙伴的模式降低市场准入门槛,EPC 及运维侧竞争加剧。292 MWh 初始规模属于小型电网侧,与 PG 的大型电网侧项目定位暂无直接竞争;但 JV 若规模化将分流 EPC 资源与电网接入容量。

来源:Energy-Storage.news(2026-06-04)

CIS Tender 8(4 GW / 16 GWh):仍在评估,截至 06-05 无授标公告 · DCCEEW,持续跟踪

官网最新状态维持"评估中","6 月出结果"的市场预期不变,但截至本期(2026-06-05)尚无公告。本周内仍属可能窗口;一旦落地将是 2026 年 NEM 最大竞争格局事件。

→ 对 PG 的影响:Tender 8 中标名单揭示后,将锁定 16 GWh 纯储能合同的区域分布与市场接受价格,直接校准 Tender 10 竞价策略,PG 应第一时间比对。

NSW 规划审批中位数吹出至 614 天——全澳最慢,WA 仅 168.5 天 · PV Magazine Australia / CEIG,2026-06-03

Clean Energy Investor Group 报告显示,NSW 独立 BESS 项目规划审批平均耗时从 2023 年的 530 天升至 2026 年的 614 天(WA 168.5 天、QLD 192 天、VIC 247 天、SA 252 天,NSW 排名垫底);审批费用比 QLD 高出最高 48 倍。目前 NSW 规划系统排队:BESS 68 个、太阳能 38 个、风电 48 个。

→ 对 PG 的影响:NSW 在 LTESA/CIS 合同上优势明显,但 614 天审批中位数需硬性纳入开发时间表。相对而言 QLD / WA 开发效率更高(若政策风险可管控),SA 和 VIC 居中。

来源:PV Magazine Australia(2026-06-03)

NSW LTESA Tender 9(12 GWh,≥8 小时长时储能):注册窗口已开,截止 2026-06-22 · ASL,2026-05-20 开标

NSW 能源委托机构 ASL 同步开放 Tender 8(2.5 GW 发电,太阳能/风电)和 Tender 9(目标 12 GWh,≥8 小时长时储能,最低 5 MW),为 NSW 史上规模最大的长时储能单轮采购。注册窗口已开,截止 2026-06-22(注册是提交投标的前置硬性条件)。

合同机制要点:LDS LTESA 支付上限(Annuity Cap)按 CPI 或法规变化可调增,仅适用 SFV 向开发商方向支付,对开发商现金流结构更为友好;可接受 NSW 全境选址(QLD 边界不受限),配合 8h 以上设计具备与钒液流、长时铁-空气等竞争同台的技术多样性。

→ 对 PG 的影响:12 GWh 目标量是整个 NSW Roadmap 迄今最大单轮采购,且 ≥8 小时门槛直接命中 PG 的 BESS 产品定位(与 SA FERM 4h/8h 双层结构不同,Tender 9 明确要求 8 小时以上)。06-22 注册截止是硬性节点,逾期无法投标。 PG 须本周内完成内部可行性判断并决定是否注册。

来源:ASL Tender 9(2026-05-20);Dentons 分析(2026-05-26)

QLD LNP 政府召回 6 个风电及 BESS 项目,持续阻碍可再生能源审批 · RenewEconomy,2026-06-05

昆士兰 Crisafulli LNP 政府已对 6 个风电及 BESS 项目发出"召回通知(call-in)",其中 Moonlight Range 风电项目批准已被直接撤销;立法修改已直接阻止 1.2 GW Forest Wind 推进;《能源路线图》为保留煤电续命向 Stanwell 等国有公司注入 AU$16 亿,导致这些企业主动撤回可再生能源投资计划。

政府同期向联邦施压,要求对 Taroom Trough 油气田实施 EPBC 快速通道(但联邦明确排除化石燃料),并授权生产力委员会对 EPBC 改革独立调查,被视为双边协议谈判筹码。

→ 对 PG 的影响:QLD 已构建"规划召回 + 法规修改 + 煤电续命补贴"三重阻拦机制,BESS 项目政策风险属全澳最高级别。PG 应将 QLD 项目管线的政策风险缓冲期至少延长 6-12 个月,短期聚焦 NSW / SA / VIC 管线推进。

来源:RenewEconomy(2026-06-05)

AEMC 最小系统负荷(MSL)规则变更提案:拟在极低需求时将现货锁定 -$1,000/MWh · AEMC,2026-04-23 提交

AEMC 可靠性面板正式提交规则变更请求,要求在最小系统负荷(MSL)三级事件期间将现货电价自动设置为市场底价(MFP = -$1,000/MWh),同步建立 MSL 治理框架。目前状态"Pending",尚未启动正式审查程序。Clean Energy Council 此前独立提交的 MSL Reserve 服务机制(允许 BESS 竞标获酬"吸纳过剩太阳能")同样处于 Pending 状态。

→ 对 PG 的影响:若两项 MSL 规则变更落地,将为 BESS 在负电价时段的充电行为提供新的价格信号和收益来源,改善全商业 BESS 的收益结构下限。落地时间需持续跟踪,当前两项变更均未启动正式审查。

来源:AEMC MSL 规则变更页;Ashurst 澳洲 E&G 月报(2026-05-12)

外资 CGT 改革草案:储能设施排除在 50% 折扣范围外 · Ashurst,2026-05-12 月报

联邦财政部《外国居民可再生能源资产 CGT 折扣草案》对外国居民处置澳洲可再生能源资产给予 50% CGT 折扣(适用至 2030-06-30),但草案明确排除储能设施(电池),除非电池"完全由可再生能源充电",实操门槛极高。行业提交意见批评:①折扣期限 2030 年截止过短;②储能排除破坏 BESS 招商吸引力。最终立法版本尚未公布。

→ 对 PG 的影响:若最终立法维持储能排除条款,外国股东/投资人在退出 PG 澳洲 BESS 项目时税务成本将显著高于纯发电资产。PG 需尽早与税务律所确认持股结构是否受影响,并关注最终立法版本。

来源:Ashurst 澳洲 E&G 月报(2026-05-12)

Trina Storage 签约日本九州 160 MWh BESS(完成 JIS8715-2R 认证,亚太新市场准入) · ESN / The Battery Magazine,2026-06-03

天合储能于 2026-06-03 宣布签约日本九州地区超高压电网储能项目(160 MWh),系统采用 Elementa 2 平台(314 Ah LFP 电芯),已通过日本 JIS8715-2R 火灾蔓延认证——这是日本电网侧储能接入的关键硬门槛。买方信息未公开。交付计划 2026 年内,COD 目标 2027 年。

天合同期在 PV EXPO 2026 上发布 Elementa 3 Flex(约 1.56 MWh 紧凑系统,专为日本空间受限场景设计)。

(已进表 A:第 21 条,首记 2026-06-05)

→ 对 PG 的影响:天合完成 JIS 认证意味着其储能系统已通过全球最严苛的进场认证之一,为 PG 在澳洲或其他高监管市场采购天合设备时的 bankability 论证增添了重要佐证。

来源:The Battery Magazine(2026-06-03)

Hithium × DSS Solar 越南 1 GWh 三年战略合作框架(SNEC 2026,06-04) · Hithium 官网,2026-06-04

海辰储能在 SNEC 2026 上与越南储能渠道商 DSS Solar 签署三年期 1 GWh 战略合作框架,覆盖越南住宅、商业及工业储能市场。Hithium 负责产品方案+供应链,DSS Solar 负责本地渠道+项目开发。框架非单一公用事业项目,为分批渠道部署。

(已进表 A:第 22 条,首记 2026-06-05)

→ 对 PG 的影响:Hithium 同时推进澳洲 LDES 发布(5 月悉尼)和东南亚渠道扩张,产能与市场布局双线加速;其在澳洲市场的可见度(Gnarwarre 500 MWh 在建)正在增强,若 PG 寻求澳洲 LDES 备选供应商,Hithium 的本地化路线是重要参考。

来源:Hithium 官网(2026-06-04)

CATL:储能业务 2030 年目标占全球营收 50%,欧洲为全球第三大储能市场 · Reuters / InvEZZ,2026-06-04

CATL 欧洲储能系统总监 Kevin Tang 在 SNEC 2026 期间接受路透社采访确认:储能业务占全球营收当前约 25%(五年前仅 2%),公司预计 2030 年升至 50%。欧洲是 CATL 储能全球第三大市场(中国→美国→欧洲),欧洲储能当前不面临类似电动车行业的"本地成分"监管压力。Tang 同时指出原材料成本(锂、铜、铝)因地缘局势短期承压。

→ 对 PG 的影响:CATL 全力押注储能与 EV 并重的战略定位,其全球 bankability 信用背书在 lender 层面将持续强化。对 PG 旗下采用 CATL 供货的项目(如 SA Reeves Plains),融资机构的供应商信用认可度持续提升是正面信号。

来源:InvEZZ / Reuters(2026-06-04)

本期 Watchlist 动态(其余 7 家,2026-06-03/05 窗口)

BYD / EVE / Envision / Sungrow / REPT / CORNEX 六家供应商本期无新的 ≥100 MWh 海外项目或订单公告;HyperStrong 无新增海外项目(SNEC 展品更新见第五节技术板块)。

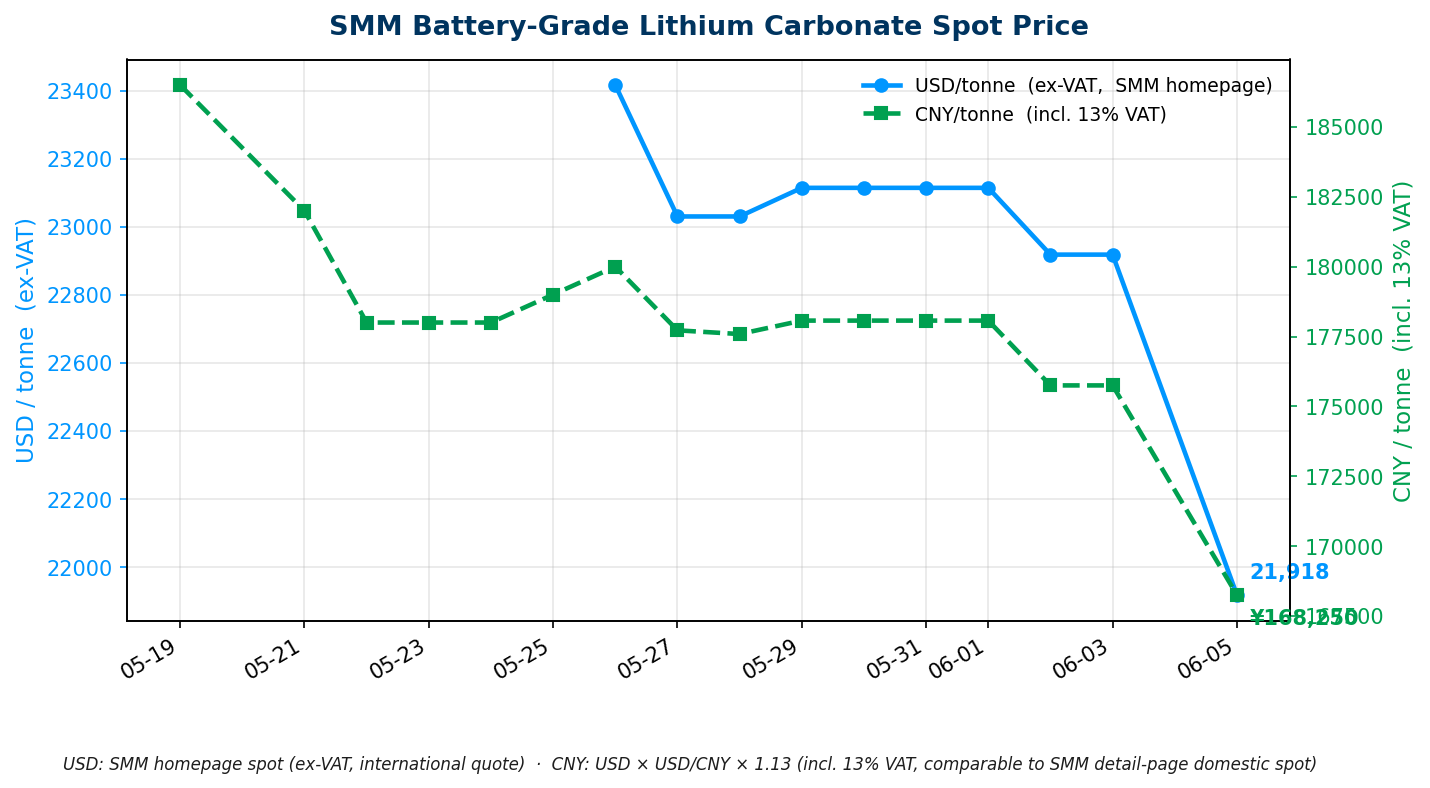

今日价格(口径:2026-06-05 北京时间 07:00 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 21,918.07 / tonne(-325.20,-1.32%) / CNY 168,250 / 吨 | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 4 日(SMM 约 10:10 发当日值,7:00 抓为 T-1 是正常);较 6 月 2 日高点 USD 22,918 跌约 4.4%;CNY 含 13% VAT 官方精确均价 |

走势分析

06-04 下行驱动:GFEX 仓单创历史高位压制 + 产量放量 + 淡季成交清淡

据 Mysteel 6 月初调研及 CITIC Futures 6 月 4 日日报综合分析,本轮下行由三条压力线叠压:

① GFEX 仓单创历史新高:截至 6 月 1 日,注册仓单总量达 56,045 手(约 5.6 万吨),5 月单月净增约 17,203 吨;仓单高企令空头获得有力打压工具,期货承压; ② 国内产量 5 月大幅回升:碳酸锂 5 月产量约 62,100 吨(+27.9% MoM),青海盐湖厂产季爬产、江西省前期环保影响消退是主因;Mysteel 预计 6 月产量继续环比增约 3.8%; ③ 月初现货成交清淡:动力电芯因 NEV 销售淡季明显拉低整体需求,实物买盘薄弱;储能电芯受出口抢装支撑相对坚挺,但两力对冲后整体偏弱。

据 CITIC Futures(2026-06-04):「仓单高企是核心压制力量——现货贴水叠加票据整治成本,大量企业将现货注册入仓,对期货形成持续打压。整体供需仍处紧平衡,但多空博弈加剧,预计短期内价格区间震荡。」

GFEX 期货曲线(2026-06-05 盘中):近月 LC2606 报 CNY 154,760/吨,主力 LC2608 报 CNY 159,700/吨,远月 LC2612 报 CNY 164,040/吨,期货曲线呈 contango 结构(近低远高),反映市场预期价格中枢将缓慢回升。

机构观点(最新口径)

机构分歧汇总(Q1 2026 最新口径)

| 机构 | 2026 年供需判断 |

|---|---|

| Wood Mackenzie | 名义盈余但强调 2028 前潜在结构性缺口(需 USD 276 亿新投资) |

| S&P Global | 盈余约 10.9 万吨 LCE(较 2025 年收窄) |

| Morgan Stanley | 预测缺口约 8 万吨 LCE |

| UBS | 预测缺口约 2.2 万吨 LCE,全年均价 CNY 200,000 |

| Benchmark MI | 需求 CAGR 14%,前向曲线 5 月约 USD 24,000/吨 |

矿端节点(Q3 关键观察)

→ 对 PG 的影响:GFEX 仓单创高 + 5 月产量放量 + 淡季买盘薄弱,三重叠压确立短期(6 月)价格区间偏弱。但机构分歧极大(MS 预测缺口 vs Wood Mac 名义盈余),CATL 枧下窝任何复产消息均可触发剧烈波动。PG 采购框架协议锁价时点建议维持「Bald Hill 7 月首矿数据落地后」判断,同步关注 Greenbushes 7 月季报信号。

来源:完整台账见 活表 D

SNEC 2026(06-03/05):电芯向 8 小时原生 LDES + AI 专属双赛道分叉 · 各厂商 SNEC 发布,2026-06-03/04

SNEC 2026 上海是本期技术信息密度最高的节点:

Hithium ∞Cell 1300Ah + ∞Power 6.9 MWh(全球首款原生 8 小时 LDES 系统):专为长时储能开发的 1300Ah 电芯,单个标准 20 英尺集装箱实现 6.9 MWh / 8 小时连续放电,设计寿命 25 年,支持并排与背靠背部署节约用地。与此同时发布 ∞Cell 650Ah 大容量电芯及 ∞Power 10+ MWh 产品方案,以及钠离子 ∞Power N2.28 MWh 系统。

REPT BATTERO 85Ah 高功率 AI 数据中心专属电芯:最大持续放电 10C、循环寿命 >60,000 次,是国内首款以"AI 数据中心专属"命名发布的储能电芯,对应 AIDC 备用电源与削峰应用的高倍率需求。同期发布 Wending® 320Ah 钠离子大容量储能电芯(>20,000 次循环寿命)。

Sungrow PowerMatrix 平台:PV + 储能 + 能量路由 + 构网型控制集成于统一架构,声称可降低 BOS 成本 10% 以上,面向公用事业、微电网、数据中心。

Ingeteam INGECON SUN STORAGE M Series(2026-06-04):构网型功能作为标配,构网型与跟网型模式均不降容运行,4 款配置(3.4/4.5/6.8/9.1 MW),装入标准 40 英尺集装箱,支持 2-12 小时储能场景,工作温度 -20°C 至 60°C。

→ 对 PG 的影响:电芯密度向 6.9-10 MWh/集装箱演进将持续压低 PG 项目的 $/MWh 采购成本;Hithium 1300Ah LDES 系统与澳洲 NSW Tender 9(12 GWh,≥8 小时)的直接对应意味着供给侧已做好准备;构网型从"选配附加"走向"标配无降容",降低 PG 在构网型技术路线上的集成成本。

来源:Hithium SNEC(2026-06-04);ESS-News Ingeteam(2026-06-04)

IEA:全球 2025 年新增电池储能 108 GW(+40%),澳洲可调度占比 18% 居全球第一 · IEA / PV Magazine USA,2026-06-03

IEA《全球能源评审 2026》确认 2025 年全球新增公用事业级+用户侧电池储能 108 GW(+40%),超越天然气有史以来单年最高新增纪录,是 2021 年的 11 倍。

澳洲数据尤为突出: - 2025 年储能新增至约 8 GW(公用事业侧约 4.2 GW + 用户侧约 3.4 GW),是 2024 年的近 9 倍 - 电池储能占澳洲可调度容量比例达 18%,全球最高(中国 7%、美国 5%、欧洲 4%) - 全球层面:能量搬移已成主导商业模式(>90%),新投运项目平均时长升至 3 小时(2023 年约 2 小时),LFP 占新增约 90%

→ 对 PG 的影响:IEA 数据是 PG 澳洲业务的最权威市场背书。可调度占比 18% 全球最高,说明澳洲 NEM 对储能的结构性依赖已远超其他市场;平均时长从 2h 升至 3h 的趋势向 4h 以上演进,与 PG 的大容量长时储能产品定位一致。

来源:PV Magazine USA(2026-06-03)

NEM 电网级 BESS 5 月收益跌至 $29k/MW/year 历史最低 · Modo Energy,2026-06-04

Modo Energy 数据显示,NEM 电网级 BESS 5 月平均收益 $29k/MW/year,较 4 月 -45%,是 Modo 自 2022 年 7 月建立指数以来的历史最低。

核心驱动因素: - 2 小时价差同比骤跌 65%:从 2025 年 5 月约 $280/MWh 压缩至今年 5 月 $99/MWh;NSW 跌幅最大达 82%;SA 相对坚挺(仅 SA 5 月日内价差仍在 $100/MWh 以上) - 三天出现净负收益(5 月 17/25/27 日):当天日内价格形态异常平坦甚至倒挂(duck curve 反转),日前预调度信号与实际价格大幅偏离,依赖日内套利策略的电池"踩空";维多利亚 5 月 1-4 日 2h 价差仅 $5-32/MWh,SA 5 月 1-3 日类似 - 结构性压缩因素:用户侧(户用)储能持续削减晚间需求峰值,电网侧 BESS 车队规模已是一年前的 2.6 倍,套利池被切分;全国家庭电池持续增加,evening peak demand 被系统性压低

Modo 指出,收益损失并非全由价差压缩解释:若干收益最差的日子,价差属正常水平,但电池的调度优化实际执行远差于价差所蕴含的理论上限——即策略执行质量(bidding discipline)成为独立的收益变量。

→ 对 PG 的影响:$29k/MW/year 的收益率,按典型 BESS 资本成本($600-900k/MW),对应的 payback period 已超 20 年——纯商业套利模式已无法支撑项目融资。这印证了 LTESA/CIS 等政府合同作为底托的绝对必要性:Modo 自己的数据显示,有 SIPS/CIS 合同覆盖的资产(如 Waratah)与全 merchant 资产(如 SA/VIC 部分项目)的收益差异超过 3 倍。PG 在任何新项目的商业案例中,合同底托应作为首要前提而非加分项。

来源:Modo Energy(2026-06-03/04)

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental · Coverage Window: 2026-06-03 ~ 2026-06-05 (Baseline: 2026-06-03)

Friday. Key headlines: Modo Energy data shows NEM grid-scale BESS revenues fell to a record-low $29k/MW/year in May 2026 (down 45% from April, down 69% YoY), with 2-hour spreads compressing 65% YoY — the financing viability of fully-merchant BESS is once again under severe pressure. TagEnergy's Morwell BESS (VIC, up to 1,000 MW / 4,000 MWh) has secured Victoria's planning approval, with an estimated investment of AU$1.3 billion. NSW LTESA Tender 9 (12 GWh, ≥8 hours long-duration storage) is now open for registration with a 22 June deadline. Kingswood BESS (NSW, 100 MW / 1,080 MWh, Iberdrola) has received both state and federal EPBC approvals (EPBC in just 7 weeks), with only the Transgrid connection agreement remaining. Queensland's LNP government has called in 6 wind and BESS projects, raising QLD development risk to the highest level in Australia. At SNEC 2026 (Shanghai, 03–05 June): Hithium unveiled the ∞Cell 1300Ah native 8-hour LDES system (6.9 MWh per 20ft container); IEA confirmed Australia's 2025 storage additions grew nearly 9x to approximately 8 GW, representing an 18% share of dispatchable capacity — the highest globally. SMM lithium carbonate: USD 21,918.07 / CNY 168,250 (SMM Date 4 June, T-1 as expected; GFEX warehouse receipts at a record high are suppressing futures, but institutions characterise the current decline as technical rather than a structural reversal).

Supporting Live Tables (continuously updated): - Australia Project Supply Chain · Table C — 43 projects ≥100 MWh (2 new this issue: Morwell BESS VIC approval + Kingswood BESS dual approval) - Chinese Supplier Overseas Projects · Table A — 2 new entries (Trina Japan Kyushu 160 MWh + Hithium Vietnam DSS Solar 1 GWh framework); total 22 entries - Supplier Profiles · Table B — 3 suppliers updated (CATL strategic target / Trina Japan market / Hithium Southeast Asia + SNEC new products) - Lithium Price History · Table D — 06-05 row appended (USD 21,918.07; SMM Date 4 June, T-1 normal); chart refreshed

Full project supply chain BOM available in Live Table C.

TagEnergy Morwell BESS (VIC, up to 1,000 MW / 4,000 MWh): Victoria planning approval secured, total investment ~AU$1.3 billion · RenewEconomy, 2026-06-04

TagEnergy (Portuguese clean energy developer; acquired the project from Australian developer Ace Power in mid-2025) has received approval from Victoria's Department of Transport and Planning for Morwell BESS — up to 1,000 MW / 4,000 MWh (4-hour duration), total investment approximately AU$1.3 billion, sited at Hazelwood North adjacent to the 500 kV Hazelwood Terminal Station — among the best grid connection locations in Australia.

Development timeline: Grid connection agreement negotiations approximately 12 months; Financial Close target end-2027; construction period 18–24 months; COD target end-2029. TagEnergy is simultaneously developing Golden Plains wind farm (1.33 GW, Australia's largest).

→ For PG: VIC has added another GW-scale approval, confirming Australia has entered the "GW-era" for storage. Latrobe Valley interconnection capacity is increasingly contested. PG considering VIC development must treat substation capacity as the primary site-screening criterion.

Source: RenewEconomy (2026-06-04)

Kingswood BESS (NSW, 100 MW / 1,080 MWh, Iberdrola): EPBC + NSW IPC fully approved; only Transgrid connection pending · RenewEconomy, 2026-06-04

Iberdrola's Kingswood BESS (100 MW / 1,080 MWh, approximately 10.8 hours, NSW LTESA Tender 6 ≥8-hour long-duration contract) has completed: ① NSW state IPC review (approved December 2025, despite 50+ community objections); ② Federal EPBC clearance in just 7 weeks (May 2026, determined "not a controlled action"). The sole remaining precondition is a grid connection agreement with Transgrid — construction expected to commence in 2026.

The project was originally designed at 270 MW and scaled down to 100 MW to win a NSW Tender 6 LTESA award (February 2026, ≥8 hours). The Tamworth substation area has become a storage cluster: Equis Australia Calala (250 MW/500 MWh, under construction), Valent Energy Tamworth (200 MW/400 MWh), and Trinasolar Burgmanns (200 MW/400–800 MWh) are all advancing in the same catchment.

→ For PG: The IPC pathway works even with 50+ objections (Kingswood: ~14 months IPC + 7 weeks EPBC). EPBC's 7-week turnaround suggests a "green channel" effect for LTESA projects. Tamworth interconnection capacity is nearing saturation — NSW inland sites require upfront substation capacity verification.

Source: RenewEconomy (2026-06-04)

Recharge Power × Energy Decarb JV: Taiwanese BESS developer enters Australia, initial pipeline 128 MW / 292 MWh · Energy-Storage.news, 2026-06-04

Taiwan-based Recharge Power (>1 GWh deployed in Taiwan; holder of Taiwan's first AFC automatic frequency control record) and Queensland-based Energy Decarb have formed a joint venture entering the Australian market. JV structure: Recharge Power provides proprietary EMS software + system integration (engineering, construction, long-term O&M); Energy Decarb provides local project development + electricity market trading capabilities. Anchor investor: St Baker Capital (Trevor St Baker AO, former ERM Power founder).

Initial confirmed pipeline: 128 MW / 292 MWh, targeting delivery within two years. Australia is reported to be the world's third-largest utility-scale storage market, with 4.3 GW of FID projects in 2025 and BESS accounting for 32% of NEM dispatch interval price-setting in Q1 2026 (overtaking hydro).

→ For PG: Overseas BESS developers entering via JV + local partner lowers the market entry threshold, intensifying EPC and O&M competition. The initial 292 MWh pipeline is small-scale grid-side, not directly competing with PG's large utility-scale focus; however, if the JV scales, it will compete for EPC resources and grid connection capacity.

Source: Energy-Storage.news (2026-06-04)

CIS Tender 8 (4 GW / 16 GWh): Still under assessment, no award announcement as of 06-05 · DCCEEW, ongoing

The official website status remains "bids under assessment" with a June 2026 indicative award timeline. The window remains open this week; once published, the award list will be the most significant competitive intelligence event of 2026 for NEM BESS.

→ For PG: The Tender 8 award list will reveal the regional distribution and market-clearing price for 16 GWh of pure-storage contracts, directly calibrating Tender 10 bidding strategy.

NSW planning approvals blown out to 614-day median — slowest in Australia; WA is just 168.5 days · PV Magazine Australia / CEIG, 2026-06-03

A Clean Energy Investor Group report shows NSW standalone BESS project planning approval times have risen from 530 days (2023) to 614 days (2026) — last among all states (WA 168.5 days, QLD 192, VIC 247, SA 252); with approval fees up to 48x higher than Queensland.

→ For PG: NSW offers the strongest LTESA/CIS contract pipeline, but the 614-day median must be hardwired into development schedules. QLD and WA offer significantly faster timelines where policy risk can be managed.

Source: PV Magazine Australia (2026-06-03)

NSW LTESA Tender 9 (12 GWh, ≥8 hours long-duration storage): Registration open, deadline 2026-06-22 · ASL, open from 2026-05-20

NSW's energy trustee ASL has launched Tender 9, targeting 12 GWh of long-duration storage (≥8 hours, minimum 5 MW) — NSW's largest-ever single-round long-duration storage procurement. Registration is now open; deadline: 2026-06-22 (registration is a mandatory prerequisite to submitting a bid).

Contract mechanism highlights: LDS LTESA payment caps (Annuity Cap) can increase with CPI or regulatory changes, applying only to SFV-to-developer payments — more favourable cash flow terms for developers. Eligible sites cover all of NSW, and the ≥8-hour requirement creates a level playing field for LFP, vanadium flow batteries, and other long-duration technologies.

→ For PG: The 12 GWh target aligns directly with PG's BESS product positioning. The 22 June registration deadline is non-negotiable — missing it forecloses bidding. PG must complete an internal feasibility assessment and registration decision this week.

Sources: ASL Tender 9 (2026-05-20); Dentons Analysis (2026-05-26)

QLD LNP government calls in 6 wind and BESS projects, ongoing obstruction of renewables · RenewEconomy, 2026-06-05

Queensland's Crisafulli LNP government has issued "call-in notices" for 6 wind and BESS projects; the Moonlight Range wind project approval has been directly revoked; legislative amendments have blocked 1.2 GW Forest Wind from proceeding; AU$16 billion channelled into coal-power continuity (Stanwell et al.), prompting those utilities to withdraw renewable investments.

→ For PG: Queensland has constructed a triple barrier — planning call-in + legislative obstruction + coal subsidies — making BESS project policy risk the highest in Australia. PG should extend QLD pipeline risk buffers by at least 6–12 months and prioritise NSW / SA / VIC pipelines in the near term.

Source: RenewEconomy (2026-06-05)

AEMC Minimum System Load (MSL) rule change proposal: Automatic -$1,000/MWh floor price during extreme low-demand events · AEMC, submitted 2026-04-23

AEMC's Reliability Panel has formally submitted a rule change request to lock the spot price at the market floor price (MFP = -$1,000/MWh) during MSL Level 3 events, alongside an MSL governance framework. Status: "Pending" — formal review not yet commenced. The Clean Energy Council's independent MSL Reserve service mechanism (allowing BESS to bid for remuneration to absorb excess solar) is also pending.

→ For PG: If both MSL rule changes are implemented, BESS will gain new revenue streams or price protection during negative-price periods. Timeline uncertain — neither change has entered formal review.

Sources: AEMC MSL Rule Change; Ashurst Australia E&G Markets Update (2026-05-12)

Foreign resident CGT reform draft: Battery storage excluded from the 50% discount · Ashurst, 2026-05-12 monthly update

The federal Treasury's draft legislation for foreign residents' CGT discount on Australian renewable energy assets (50% discount, applicable until 30 June 2030) explicitly excludes storage facilities (batteries), unless the battery is "entirely charged by renewable energy" — a near-impossible threshold in practice. Industry submissions criticise both the 2030 sunset date and the storage exclusion. Final legislation has not been published.

→ For PG: If the exclusion is retained, foreign shareholders/investors will face materially higher tax costs on exiting PG's Australian BESS assets compared to pure generation assets. PG should engage tax counsel early to assess the impact on holding structures.

Source: Ashurst Australia E&G Markets Update (2026-05-12)

Australia projects in Table C; non-Australia projects in Table A; supplier profiles in Table B.

Trina Storage signs 160 MWh BESS in Japan's Kyushu region (JIS8715-2R certified, new APAC market entry) · ESN / The Battery Magazine, 2026-06-03

Trina Storage announced on 2026-06-03 the signing of a contract for a 160 MWh ultra-high-voltage grid-scale BESS project in Japan's Kyushu region, using the Elementa 2 platform (314 Ah LFP cells), certified to Japan's mandatory JIS8715-2R fire propagation standard — the key regulatory gateway for grid-side storage in Japan. Buyer details undisclosed. Delivery planned within 2026, COD target 2027.

(Added to Table A: entry #21, first recorded 2026-06-05)

→ For PG: Achieving JIS8715-2R certification — one of the strictest market entry certifications globally — strengthens the bankability case for Trina equipment in PG's Australian projects and other high-regulatory markets.

Source: The Battery Magazine (2026-06-03)

Hithium × DSS Solar Vietnam 1 GWh three-year strategic cooperation framework (SNEC 2026, 06-04) · Hithium, 2026-06-04

Hithium and Vietnamese storage channel distributor DSS Solar signed a three-year 1 GWh strategic cooperation framework at SNEC 2026, covering residential, commercial, and industrial storage in Vietnam. Hithium provides product solutions and supply chain; DSS Solar provides local channels and project development. Framework covers distributed deployment rather than a single utility-scale project.

(Added to Table A: entry #22, first recorded 2026-06-05)

→ For PG: Hithium is simultaneously advancing Australian LDES market entry (May 2026 Sydney launch) and Southeast Asia channel expansion. Its growing visibility in the Australian market (Gnarwarre 500 MWh under construction) makes Hithium an increasingly credible LDES supplier option if PG is exploring alternatives.

Source: Hithium (2026-06-04)

CATL: Energy storage to reach 50% of global revenue by 2030; Europe is its third-largest storage market · Reuters / InvEZZ, 2026-06-04

CATL's Head of European Energy Storage Systems Kevin Tang confirmed at SNEC 2026 that energy storage currently accounts for approximately 25% of CATL's global revenue (just 2% five years ago), with a target of 50% by 2030. Europe is CATL's third-largest storage market globally (China → US → Europe), and European storage currently faces no "local content" regulatory pressure comparable to the EV sector. Tang also flagged short-term raw material cost pressure (lithium, copper, aluminium) from geopolitical factors.

→ For PG: CATL's strategic pivot to storage as a co-equal business line with EVs will strengthen its global bankability profile with lenders. For PG projects using CATL supply (e.g., SA Reeves Plains), financier credit acceptance for the supplier continues to improve.

Source: InvEZZ / Reuters (2026-06-04)

Watchlist update — remaining 7 suppliers (2026-06-03/05 window)

BYD, EVE, Envision, Sungrow, REPT, CORNEX: no new overseas project or order announcements ≥100 MWh this period. HyperStrong: no new overseas project announcements (SNEC product launches covered in Section V).

Today's price (collected: Beijing time 07:00, 2026-06-05)

| Product | Latest Price | Basis |

|---|---|---|

| Battery-Grade Lithium Carbonate (SMM) | USD 21,918.07/tonne (-325.20, -1.32%) / CNY 168,250/tonne | SMM-Li-LC-001 Avg; SMM Date 4 June (SMM releases same-day value ~10:10 Beijing time; 07:00 capture is T-1, expected); approx. -4.4% from 2 June peak of USD 22,918; CNY is the official VAT-inclusive average price (13% VAT) |

Price analysis

04 June decline drivers: Record GFEX warehouse receipts + supply recovery + weak seasonal demand

Based on Mysteel's early-June survey and CITIC Futures' 4 June daily report, the current decline is driven by three overlapping pressure lines:

① GFEX warehouse receipts at a record high: Total registered warehouse receipts reached 56,045 lots (~56,045 tonnes) as of 1 June, with a net increase of approximately 17,203 tonnes in May. The surge gives short sellers a powerful suppression tool, weighing on futures prices; ② Chinese domestic production surged in May: Lithium carbonate output approximately 62,100 tonnes (+27.9% MoM), driven by seasonal ramp-up at Qinghai brine producers and the easing of prior environmental compliance impacts in Jiangxi; Mysteel projects a further approximately +3.8% MoM increase in June; ③ Weak spot trading at month start: EV cell demand is seasonally weak, with thin physical buying; ESS cells remain relatively firm on export pre-purchase activity, but insufficient to offset overall weakness.

Per CITIC Futures (2026-06-04): "Record warehouse receipts are the core suppression force — physical inventory being registered into GFEX while contango basis narrows, combined with inventory financing costs, is continuously pressuring futures. Overall supply-demand remains in tight balance, but the bull-bear battle has intensified; range-bound trading expected near-term."

GFEX futures curve (intraday 2026-06-05): LC2606 CNY 154,760/tonne; front-month LC2608 CNY 159,700/tonne; LC2612 CNY 164,040/tonne — a contango structure reflecting the market's expectation that price pressure will gradually ease over the coming months, but near-term downside remains.

Institutional views (latest vintage)

Institutional divergence summary (Q1 2026 latest estimates)

| Institution | 2026 Supply-Demand Assessment |

|---|---|

| Wood Mackenzie | Nominal surplus, but highlights potential structural deficit before 2028 (requires USD 27.6B in new investment) |

| S&P Global | Surplus of approximately 109,000 tonnes LCE (narrowing from 141,000 tonnes in 2025) |

| Morgan Stanley | Projected deficit of approximately 80,000 tonnes LCE |

| UBS | Projected deficit of approximately 22,000 tonnes LCE; full-year average price CNY 200,000 |

| Benchmark MI | Demand CAGR 14%; forward curve ~USD 24,000/tonne in May |

Mine-level milestones (Q3 key observations)

→ For PG: The three-factor overlay — record GFEX receipts + supply volume recovery + weak seasonal demand — establishes a soft June near-term price environment. However, institutional divergence remains extreme (MS deficit vs. Wood Mac nominal surplus), and CATL's Jianxiawo mine represents a binary news risk capable of triggering 3–5% single-day swings. PG's procurement framework agreement lock-in timing should remain at "after the MinRes Bald Hill July first-ore data lands," with additional monitoring of the Greenbushes July quarterly report.

Source: Full price ledger in Table D

SNEC 2026 (06-03/05): Cell roadmaps bifurcate into native 8-hour LDES and AI-dedicated tracks · Multiple vendors at SNEC, 2026-06-03/04

SNEC 2026 in Shanghai was the densest technology information release event of this period:

Hithium ∞Cell 1300Ah + ∞Power 6.9 MWh (world's first native 8-hour LDES system): A 1300Ah cell purpose-designed for long-duration storage; a single standard 20ft container delivers 6.9 MWh / 8-hour continuous discharge, 25-year design life, supporting side-by-side and back-to-back deployment to conserve land. Also launched: ∞Cell 650Ah large-capacity cell, ∞Power 10+ MWh product system, and sodium-ion ∞Power N2.28 MWh system.

REPT BATTERO 85Ah high-power AI data centre-specific cell: Maximum sustained discharge of 10C, >60,000 cycle life — the first domestic cell to be launched under an "AI data centre-dedicated" designation, targeting AIDC backup and peak-shaving high-rate applications. Also launched: Wending® 320Ah sodium-ion large-capacity storage cell (>20,000 cycle life).

Sungrow PowerMatrix platform: PV + storage + energy routing + grid-forming control integrated in a unified architecture, claiming >10% BOS cost reduction, targeting utility-scale, microgrid, and data centre applications.

Ingeteam INGECON SUN STORAGE M Series (2026-06-04): Grid-forming as standard — no derating in either grid-forming or grid-following mode; 4 configurations (3.4/4.5/6.8/9.1 MW) in a standard 40ft container; supports 2–12 hour storage; operating range -20°C to 60°C.

→ For PG: Cell density evolving toward 6.9–10 MWh per container will continue to drive down PG project $/MWh procurement costs. Hithium's 1300Ah LDES system directly addresses NSW Tender 9 (12 GWh, ≥8h) — the supply side is ready. Grid-forming transitioning from "optional add-on" to "standard with no derating" reduces PG's integration cost premium for grid-forming specifications.

Sources: Hithium SNEC (2026-06-04); ESS-News Ingeteam (2026-06-04)

IEA: Global 2025 battery storage additions reached 108 GW (+40%); Australia's 18% dispatchable capacity share is the world's highest · IEA / PV Magazine USA, 2026-06-03

IEA's Global Energy Review 2026 confirms global utility-scale and behind-the-meter battery storage additions of 108 GW in 2025 (+40%), surpassing the all-time single-year record for gas capacity additions and representing 11 times the 2021 level.

Australia's figures stand out sharply: - 2025 additions reached approximately 8 GW (utility-side ~4.2 GW + behind-the-meter ~3.4 GW) — nearly 9x the 2024 figure - Battery storage now accounts for 18% of Australian dispatchable capacity — the highest globally (China 7%, USA 5%, Europe 4%) - Globally: energy arbitrage now dominates commercial models (>90%); newly commissioned projects average 3-hour duration (up from ~2 hours in 2023); LFP accounts for approximately 90% of new additions

→ For PG: IEA data is the strongest external validation for PG's Australian strategy. Australia's 18% dispatchable share — far ahead of any other market — demonstrates the structural depth of NEM's dependence on storage. The average duration trend from 2 to 3 hours moving toward 4+ hours is consistent with PG's large-capacity, longer-duration product positioning.

Source: PV Magazine USA (2026-06-03)

NEM grid-scale BESS May revenues hit record low at $29k/MW/year · Modo Energy, 2026-06-04

Modo Energy data shows NEM grid-scale BESS revenues averaged $29k/MW/year in May 2026 — down 45% from April and the lowest since Modo's index began in July 2022.

Key drivers: - 2-hour spreads down 65% YoY: Compressed from approximately $280/MWh (May 2025) to $99/MWh (May 2026) across the NEM; NSW led the compression at 82%; SA was relatively resilient (still above $100/MWh intraday spread for most days) - Three days of net-negative revenues (17, 25, 27 May): Intraday price profiles were abnormally flat or inverted (duck curve reversal); pre-dispatch signals diverged significantly from actual prices; batteries relying on standard shape expectations were caught out. Victoria 1–4 May saw 2-hour spreads of just $5–32/MWh; SA 1–3 May similar - Structural compression factors: Behind-the-meter storage is persistently shaving evening peak demand; the grid-scale BESS fleet is now 2.6 times its year-ago size, competing for the same arbitrage pool

Modo notes that revenue losses were not fully explained by spread compression alone: several of the worst revenue days had average-to-high spreads but poor capture — bid execution quality has emerged as an independent revenue variable separate from market conditions.

→ For PG: At $29k/MW/year and typical BESS capex of $600–900k/MW, the implied simple payback exceeds 20 years — fully-merchant BESS is not financeable. This reinforces that LTESA/CIS contracts are a financing prerequisite: Modo's own data shows assets with SIPS/CIS contract coverage (e.g., Waratah) outperform fully-merchant assets by more than 3x in revenue terms. In PG's commercial case for any new project, a contracted revenue floor must be a primary assumption, not a bonus.

Source: Modo Energy (2026-06-03/04)

This report is automatically compiled daily by the PGSH internal research system; each item's source is individually noted. The project developments, policy updates, price data, and institutional views presented are for internal reference only and do not constitute investment, procurement, or commercial decision advice. For any item of interest or where action is contemplated, please directly access the corresponding source link to verify the accuracy and currency of the information.