类型:增量 · 覆盖窗口:2026-06-02 ~ 06-03(基线 2026-06-02)

周三。本期核心:Akaysha Orana BESS(NSW,415 MW / 1,660 MWh)完成调试首次达到满功率输出,COD 待定;同日 BlackRock 开启 Akaysha 整体出售数据室,内部文件预测 2029 年底 EBITDA 超 AU$6 亿 - 是 2026 年澳洲 BESS 行业最大 M&A 信号。QLD BESS 车队 05-31 创下 79.5% 可再生+储能瞬时消费占比历史新高。政策侧,SA FERM Tender 1"4 小时标称、8 小时运行"的投标结构机制获深度披露,直接参考 CIS Tender 8 竞价策略;NSW《Prioritising Renewable Energy Bill 2026》已通过下议院,待上议院审议;NEM 结算周期缩短最终规则(5 天内有效)2026-08-09 生效;AEMO 2026 ISP 最终版定于 06-25 发布。供应商侧,阳光电源签下智利 Librillo BESS 643.8 MWh 供货协议(新增表 A)。锂价 SMM 最新值维持 06-02 精确值 USD 22,918.04 / CNY 175,750(T-1 正常),机构分析将本次回调定性为"进口放量+矿端复产预期"主导的技术性回落而非趋势逆转。技术侧,Fluence Smartstack 正式进入 Siemens × Nvidia Vera Rubin 136 MW AI 数据中心参考架构,标志 BESS 从配角跃升为 AI 基础设施核心组件。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 41 个 ≥100 MWh 项目(本期更新 1 条:Orana 状态至「调试完成·满功率输出,COD 待定」) - 中国供应商海外项目 · 表 A — 本期新增 1 条(Sungrow 智利 Librillo 643.8 MWh);当前 20 条 - 供应商档案 · 表 B — 本期无更新 - 锂价历史 · 表 D — 今日已追加 06-03 行(USD 22,918.04;SMM 最新 Date 6 月 2 日,T-1 正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

Akaysha Orana BESS(415 MW / 1,660 MWh,NSW):调试完成,满功率输出,COD 待定;BlackRock 开启整体出售 · RenewEconomy,2026-06-02

Akaysha Energy 确认其位于 NSW 中西部(Dubbo 附近)的 Orana BESS(415 MW / 1,660 MWh,Tesla Megapack)已在本周首次达到满功率输出并通过 hold point 测试(commissioning 阶段完成),正式商业运营日(COD)尚需完成最终监管、市场和合同手续。Akaysha 声明"按时完工、成本低于预算",资金背景为 2024 年 7 月完成的 AU$6.5 亿融资,售电方为 EnergyAustralia(12 年 tolling 协议)。

M&A 进展(同日 AFR Street Talk 独家):BlackRock 已为旗下 Akaysha Energy 开启数据室,寻求整体出售。内部财务文件预测 Akaysha 2029 年底 EBITDA 超 AU$6 亿,收益来源集中于:① Waratah Super Battery(850 MW / 1,680 MWh,NSW,5.5 年 SIPS 合同,目前因变压器事故约半容量运行,恢复目标 2026 年底);② Orana(EnergyAustralia 12 年协议);③ Elaine(VIC,311 MW / 1,244 MWh,Snowy Hydro 15 年虚拟托管,在建);④ Ulinda Park P2(QLD,350 MW / 780 MWh,在建);⑤ 新获 SA FERM Brinkworth(250 MW / 1,000 MWh nameplate,15 年 FERMA)。Akaysha 2022 年被 BlackRock 收购,是澳洲规模最大的独立 BESS 组合持有方,出售若成交将是该行业迄今最大 M&A 事件。

→ 对 PG 的影响:BlackRock 出售 Akaysha 意味着澳洲 BESS 资产在大型金融机构层面已达资本化「退出窗口」,EBITDA >AU$6 亿的预测(约对应 2-3 GW 运营资产)为 PG 项目定价和 IRR 论证提供了直接参照。若战略买家(基础设施基金/公用事业)接盘,Akaysha 可能加速管线开发;若财务买家则影响有限。PG 应密切跟踪竞价进程及最终买家身份。

来源:RenewEconomy(2026-06-02)

Eku Energy Griffith BESS(100 MW / 1,000 MWh,10 小时,NSW):进入联邦 EPBC 评估队列,74 份反对意见或触发 NSW IPC 复审 · RenewEconomy,2026-06-02

英国开发商 Eku Energy 的 Griffith BESS(NSW Griffith 镇,Yoogali 太阳能农场旁,占地约 7.5 公顷,132 kV 接入 TransGrid 变电站)已提交联邦 EPBC 环评申请。规格较前期 LTESA 合同(100 MW / 800 MWh,8 小时)升级至 10 小时(1,000 MWh),联邦环境调查未发现受威胁物种,海拔与火灾/洪水风险评估均较低,联邦通关预期顺畅。

NSW 州规划层面,项目收到 74 份反对意见,其中仅 1 份来自 650 米内真实本地居民(道路/噪音),其余来自 QLD、TAS、VIC 及 NSW 其他地区,内容多为模板化(含"外资担忧"、"可再生能源毒素"等不实声称)。NSW 规划规定反对意见达到一定门槛即触发 NSW IPC 第二次审查,预计为项目引入 3-6 个月额外时间成本。

→ 对 PG 的影响:澳洲 BESS 项目正面临"远距离模板化反对"现象成规模化趋势,IPC 触发门槛成为项目时间线的潜在隐患。若 NSW《Prioritising Renewable Energy Bill》在上议院通过,PEP 认定项目可绕过 IPC 无上诉通道,Griffith 这类案例可能是最先受益的候选。PG 在 NSW 开发时须将社区参与策略提前至选址阶段,以主动管控反对意见数量。

来源:RenewEconomy(2026-06-02)

QLD BESS 车队:05-31 创 79.5% 可再生+储能瞬时占比历史新高,5 月单月调度超 100 GWh · Energy-Storage.news,2026-06-02

2026 年 5 月 31 日 11:20,昆士兰 BESS 车队推动该州可再生能源+储能瞬时消费占比达 79.5%,超越 4 月 13 日纪录(78.4%)。同期 10:50,电池储能单项占比达 16.9%(一年前约 6.4%,近三倍增长)。主要在线 BESS:Stanwell Tarong(300 MW / 600 MWh)、Quinbrook Supernode Unit 2(260 MW / 1,090 MWh)、CleanCo Swanbank(250 MW / 500 MWh,2026-02 投产)。5 月 QLD 电池调度量首次超过 100 GWh(NEM 各州首次单月破此门槛)。

收益数据对比:CleanCo Swanbank 5 月收益 AU$74.3 万,维州大电池(Big Battery VIC,450 MWh)同期仅 AU$30.6 万(差距 2.4 倍),反映 QLD 相较 VIC 仍具日内价差优势,但日内价差已从高峰期压缩至 AU$110/MWh 以下(SA 除外)。

→ 对 PG 的影响:QLD BESS 装机迅速上量正在压缩日内套利空间,纯商业 BESS 的收益率将趋降;在 QLD 布局需优先考量叠加 FCAS / CIS 合同的混合收益结构。Swanbank vs. 维州大电池的收益对比,也印证了 NSW/VIC 市场中合同收入(LTESA/CIS)对提高收益稳定性的战略价值。

来源:Energy-Storage.news(2026-06-02)

CIS Tender 8(4 GW / 16 GWh 可调度储能):仍在评估中,本月内预期授标 · DCCEEW,持续跟踪

DCCEEW 官网最新状态(2026-05-22 更新):CIS Tender 8 标书"仍在评估中(bids under assessment)",指示性授标时间为"2026 年 6 月"。投标截止于 2026 年 2 月 6 日,评估已历约 4 个月。CIS Tender 7(混合型,7.9 GWh,19 个项目)已于 5 月 26 日公布,CIS Tender 9(5 GW 发电,联邦层面)已于 5 月 25 日开标(注册截止 6 月 22 日)。截至今日(2026-06-03),Tender 8 尚无公告。

→ 对 PG 的影响:Tender 8 授标名单一旦公布,将直接揭示 NEM 下一批 16 GWh 纯储能合同的区域分布与中标竞争者,是当前最重要的价格信号节点。PG 应持续监控 DCCEEW 官网(Closed CIS Tenders 页),结果落地后需立即校准 Tender 10 竞价策略。

来源:DCCEEW CIS Tenders(持续更新)

SA FERM Tender 1:「4h 标称容量、8h 持续调度」双层投标结构机制详解 · RenewEconomy,2026-06-03

RenewEconomy 6 月 3 日深度报道披露 SA FERM Tender 1 授标机制:六个 FERMA 项目合计标称容量 1,334 MW / 5,336 MWh(nameplate),但 FERMA 合约容量仅为 517 MW / 4,136 MWh(committed)。机制设计:FERMA 要求在"预测储备不足(Forecast Lack of Reserve,LOR)"系统应力事件触发时,储能资产须持续调度 8 小时以上;但开发商可以更小的「committed」容量投标,以标称容量建设(4 小时设计),在实际事件中以部分放电功率延长调度时长至 8 小时。

这一机制与 CIS Tender 8 的技术规格(≥4 小时时长)存在可借鉴之处:开发商可用 4 小时标称系统在 LOR 触发时以 50% 功率运行,实现 8 小时容量合规 - 投资成本控制与合同容量最大化双优。Akaysha Brinkworth(250 MW / 1,000 MWh nameplate,92 MW / 736 MWh committed)和 ZEBRE Dartmoor(144 MW / 576 MWh nameplate,50 MW / 400 MWh committed)均采用此结构。

→ 对 PG 的影响:4h/8h 双层结构对 CIS Tender 8 及未来 FERMA / LTESA 竞标均有直接策略参考价值。在技术规格书起草阶段,PG 应评估以 4 小时系统参与 8 小时合同的技术可行性(PCS 降额运行、热管理余量)以优化 CAPEX,同时规避过度设计风险。

来源:RenewEconomy(2026-06-03)

NSW《Prioritising Renewable Energy Bill 2026》:通过下议院(05-28),进入上议院 · Dentons,2026-05-28

NSW《Energy Legislation Amendment (Prioritising Renewable Energy) Bill 2026》于 05-28 携修正案通过下议院,进入 Legislative Council(上议院)审议。核心机制:能源部长可将特定 BESS / 可再生发电 / 输电项目认定为"Priority Energy Project(PEP)",PEP 可:① 绕过常规 IPC 意见程序,由规划部长直接决定;② 无合并上诉权(申请方和反对方均不可上诉);③ 享受法定审批时序加速。05-27 修正案加入 12 个月强制回顾条款(评估社区参与质量和利益分配公平性);适用范围明确排除煤电和核电配套储能。

→ 对 PG 的影响:法案若通过上议院,PG 在 NSW 的 BESS 项目若被认定为 PEP,可将 DA 周期从 12-18 个月压缩至约 3-6 个月,对 CIS Tender 10 / NSW LTESA 等时间紧迫窗口具有实质意义。PG 应在法案通过后第一时间向 Norton Rose Fulbright / Baker McKenzie 确认"优先识别"申请条件和前置材料清单。

来源:Dentons(2026-05-28)

NEM 结算周期缩短最终规则:2026-08-09 正式生效(约 67 天后) · AEMO,持续跟踪

AEMC 2024-12 通过的《Shortening the Settlement Cycle》最终规则(ERC0384)将于 2026 年 8 月 9 日(第 33 账单周起)正式生效,结算周期从约 30 个工作日压缩至 9 个工作日。AEMO 配套实施《NEM Settlement Revisions Policy》和结算历法重配置。意义:更短结算周期降低 BESS 运营商现金流占用,加快市场收益实现节奏,对短期流动性要求高的独立项目公司尤为利好。

→ 对 PG 的影响:PG 澳洲 BESS 资产运营现金流节奏将于 8 月改善;需在 08-09 前确认所有运营项目(若有)的结算系统和合同条款已适配新机制。

来源:AEMO

AEMO 2026 ISP 最终版:定于 2026-06-25 发布 · AEMO

AEMO 2026 年综合系统规划(Integrated System Plan)最终版按官方时间表定于 2026 年 6 月 25 日发布(距今 22 天)。2025 年 12 月草案已将 BESS 列为 NEM 最低成本转型核心组件,并首次将分布式电池渗透预测上调(IEEFA 建议版本)。正式发布后,最优开发路径(ODP)将锁定哪些输电与储能投资属于"可操作(actionable)"项目,直接影响 CIS / ARENA / 州级资金优先级。

→ 对 PG 的影响:06-25 ISP 将确认 NEM 未来 10-20 年储能容量需求曲线;建议 PG 在发布后一周内研读 ODP 中针对目标州(NSW / QLD / SA)的储能缺口指标,以校准项目开发优先级和 Tender 10 竞价策略。

AEMC Package 2(NEM 大型负载接入标准):复杂提交意见或延迟最终规则时间表 · AEMC,2026-05-07 后

AEMC《Improving NEM Access Standards — Package 2》咨询期于 5 月 7 日截止,收到 Tesla、Akaysha、Sungrow、AWS 等多方意见(含 05-12/15 延期提交)。AEMC 已明确声明"如提交内容涉及复杂问题,可能考虑延长最终裁定时间",原"年中出最终规则"的时间表存在推迟风险。核心争议点:数据中心 ride-through 强制要求的技术门槛(AWS 公开反对)和 HVDC 运营商购买第三方系统强度的合同安排。

→ 对 PG 的影响:Package 2 最终规则若推迟至 2026 年下半年,将延缓数据中心强制配储义务的明确时点。PG 在含 AIDC 场景的项目方案制定中,应预留规则不确定性缓冲,避免过度依赖尚未落地的政策义务进行商业案例定性。

Sungrow × Sonnedix:智利 Librillo BESS 643.8 MWh 供货协议(PowerTitan 2.0,Q1 2027 交付) · Energy-Storage.news,2026-05-28

阳光电源与西班牙 IPP Sonnedix 签署 643.8 MWh 储能供货协议,用于智利 Sonnedix Librillo BESS 项目:

(已进表 A:第 20 条,首记 2026-06-03)

→ 对 PG 的影响:Sungrow PowerTitan 2.0 在多大洲商业部署记录持续丰富(沙特 / UAE / 智利),lender 对 PowerTitan 产品线的工程验证文件将持续增厚;若 PG 在澳洲采购 Sungrow 设备,可要求供应商提供智利 / 沙特项目的运营参考案例作为 bankability 材料。

来源:Energy-Storage.news(2026-05-28)

本期 Watchlist 动态(2026-06-02/03 窗口)

2026-06-02/03 搜索窗口内,CATL / BYD / EVE / Hithium / Envision / Trina / REPT / CORNEX / HyperStrong 九家供应商暂无新的海外项目或订单公告(≥100 MWh 门槛)。

今日价格(口径:2026-06-03 北京时间 07:00 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

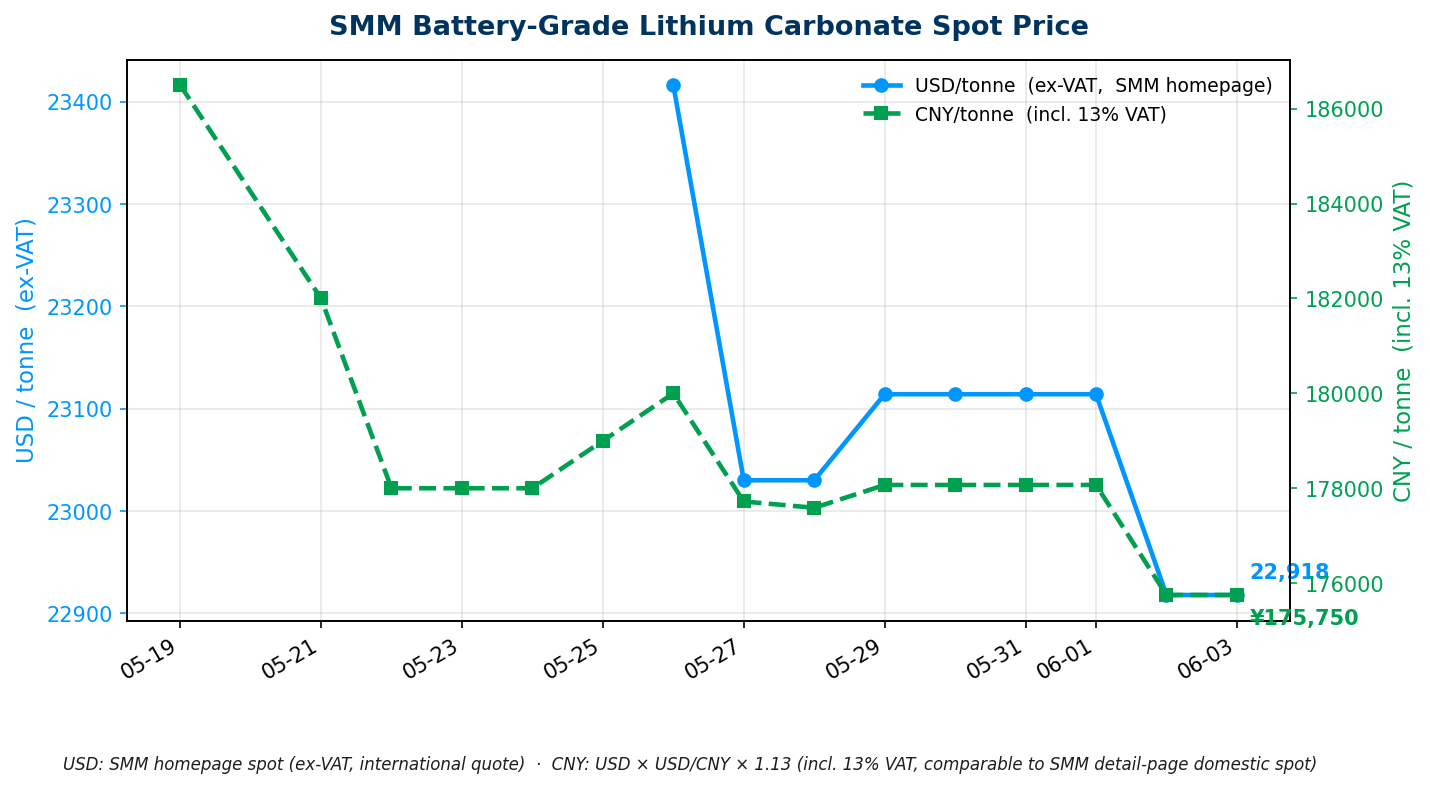

| 电池级碳酸锂(SMM) | USD 22,918.04 / tonne(0,持平)/ CNY 175,750 / 吨 | SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 2 日(SMM 约 10:10 发当日值,7:00 抓为 T-1 是正常);较上周五 USD 23,114 低约 -0.85%;CNY 含 13% VAT 官方精确均价 |

走势分析

06-02 回调驱动因素 - 进口放量与矿端预期双重压制,非趋势逆转

据 CarbonCredits.com(2026-06-02)及 SMM 周评(2026-05-21)综合分析,06-02 碳酸锂现货 -1.82%(USD 22,918 / CNY 175,750)的回调主要由两条压力线主导:

① 进口补货放量:中国 1-4 月累计进口碳酸锂约 116,000 吨(同比 +47%),硫酸锂同比 +121%;智利来源占碳酸锂进口的 65%,进口端持续补库限制了国内现货的反弹空间 ② 矿端复产预期:MinRes 正式宣布重启 Bald Hill(5 月 19 日公告),6 月采矿、7 月首产精矿(5.1% SC,年产能约 165,000 吨干重)、FY2027 Q1 首批 Esperance 港出货,是市场计入 H2 供给增量的重要信号,触发部分获利回吐

SMM 周评的价格情绪判断:"见跌买入、见涨观望"是近期市场主流行为,下游在价格回落时主动补库,上游惜售;短期区间 CNY 174,000-181,000 元/吨。

机构观点

矿端节点(Q3 关键观察)

| 矿山 | 进展 | 来源 |

|---|---|---|

| MinRes Bald Hill(西澳) | 2026-05-19 正式公告重启;6 月采矿,7 月首矿,FY2027 Q1 首批出货,FY2027 Q2 满产 | North Miner |

| Pilbara Minerals Ngungaju(西澳) | Board 2026-02-19 批准重启,7 月初恢复生产(约 200,000 吨/年),时间节点 3 月季报确认不变 | PLS 季报 |

| Core Lithium Finniss(NT) | 2026-03-18 FID,4 月授予采矿合同,5 月起采矿;目标 Q3 CY2026 首产精矿 | Mining Weekly |

| IGO Greenbushes(西澳) | FY2026 产量指引已下调至 1,375-1,425 万吨(此前 1,500-1,700 万吨);Q2 季报(7 月下旬)是下一个关键节点 | Benchmark MI(2026-04-28) |

→ 对 PG 的影响:当前回调属"进口+预期"压制的技术性调整,InfoLink / Benchmark 前向曲线维持 H2 偏多方向。三矿复产实物量 Q3 才显性化,Q2 末至 Q3 初(即 Bald Hill 首批出货数据落地前)为价格最高不确定阶段;PG 采购框架协议锁价时点仍以「Bald Hill 7 月首矿数据落地后」为宜,同步关注 Greenbushes 7 月季报是否有进一步减产信号。

来源:完整台账见 活表 D

Fluence Smartstack 进入 Siemens × Nvidia Vera Rubin AI 数据中心参考架构:BESS 成为 AI 基础设施核心组件 · Siemens / Energy-Storage.news,2026-06-01

Siemens 发布《DSX Vera Rubin AI Factory Reference Design》,专为 Nvidia Vera Rubin NVL72 GPU 架构设计,设施总容量 136 MW(IT 负载 100 MW),通过 34.5 kV 电网接入。Fluence Smartstack BESS 是唯一被指定的储能方案,承担四项系统功能:

背景:Fluence 已与两家超大规模云服务商签署主供货协议(master supply agreements),Fluence 上半财年积压合同额 US$56 亿(同比翻倍)。此次 Siemens × Nvidia 参考架构将 Fluence 定位为 AI Factory 的基础配置,预计澳洲数据中心参与者将快速跟进参考同类架构。

→ 对 PG 的影响:AI 数据中心配储正从"合规柴油替代"升级为"AI 基础设施核心层",商业模式从单次设备采购转向长期系统服务;澳洲 2030 年数据中心容量预测从 1.4 GW 增至 3.2 GW(AEMO),AEMC ride-through 强制规则年中落地后,PG 有机会探索数据中心 co-location 或 BESS-as-a-Service 商业模式,与 Fluence 模式的澳洲本地化版本形成竞争或合作。

来源:Energy-Storage.news(2026-06-01)· Siemens Press

InfoLink Q1 2026 全球储能电芯出货:587Ah 大电芯年底渗透率预计冲 20% · InfoLink Consulting,2026-06

InfoLink Q1 2026 储能电芯数据:全球储能电芯出货量 205.52 GWh(同比 +98.7%,环比 +1.62%),InfoLink 将 2026 全年预测上调至 897 GWh。结构变化:500+ Ah 大电芯 Q1 渗透率约 5%,预计年底突破 20%。587/588 Ah 格式(CATL、Hithium、REPT、EVE 均已量产)正从"旗舰产品"转为"主流格规";CATL 587Ah 济宁基地单颗制造成本较 314Ah 降低 42%,系统 CAPEX 降幅约 10-15%。

→ 对 PG 的影响:587Ah / 6.25 MWh 系统正在成为 20 英尺集装箱大型储能的新工程标准;PG 在 2026-2027 年 RFQ 文件中可将"587Ah 或等效新规格"列入技术规格,以锁定更优 CAPEX,同时预留"314Ah 兼容"以维持竞争面。

NSW EIR LDES 招标新一轮:8 小时以上长时储能,注册窗口已开(注册截止预计 2026-06-22) · ASL / pv-magazine,2026-05

NSW 消费者受托人 ASL 开放新一轮长时储能(LDES)招标,目标采购 8 小时以上储能资产,商业运营目标 2029 年或 2033 年底。评分框架纳入"系统强度与电网服务贡献"正式评分项(原 NSW EIR Tender 6 已验证 VRFB 与 LFP 均可竞标)。注册窗口已开,具体截止日期及采购量待一手来源确认。

注意:本条招标详情(目标容量/截止日期精确数字)来源为二手引用,建议 PG 直接访问 ASL 官网核实最新参数后决定是否注册。

→ 对 PG 的影响:NSW 长时储能招标与联邦 CIS Tender 8 结果预期同步窗口叠加,6 月是澳洲 BESS 政策密度最高时段;PG 若有 NSW 管线项目,须在本周内评估参与可行性并完成 ASL 注册审查。

本期暂缺

本期 Modo Energy 文章抓取工具连接超时;备用搜索亦未在 06-01 之后发现新的澳洲 NEM 相关文章。最近覆盖(Neil Weaver,06-01,NEM 跨市场 BESS 收益结构)已在 2026-06-02 研报完整报道。

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental · Coverage window: 2026-06-02 ~ 06-03 (baseline: 2026-06-02)

Wednesday. Key highlights: Akaysha Orana BESS (NSW, 415 MW / 1,660 MWh) completed commissioning and reached full output for the first time, with COD pending final regulatory and contractual sign-off; BlackRock simultaneously opened a data room for a potential sale of Akaysha, with internal documents forecasting EBITDA exceeding AU$600M by 2029 - the largest M&A signal in the Australian BESS sector in 2026. Queensland's BESS fleet set a new instantaneous record of 79.5% renewables-plus-storage share of consumption on 31 May. On the policy front, SA FERM Tender 1's "4-hour nameplate, 8-hour dispatch" bidding structure was explained in depth, offering direct strategic reference for CIS Tender 8; NSW's Prioritising Renewable Energy Bill passed the lower house and is now before the upper house; the NEM Settlement Cycle Shortening final rule takes effect 2026-08-09; and AEMO's 2026 ISP final version is scheduled for 06-25. On the supply side, Sungrow signed a 643.8 MWh supply agreement for Chile's Librillo BESS project (new Table A entry). SMM lithium carbonate price held at the 06-02 precise value of USD 22,918.04 / CNY 175,750 (T-1, normal), with institutional analysis characterising the recent pullback as a technical correction driven by import volume and mining restart expectations rather than a trend reversal. On the technology front, Fluence Smartstack was formally incorporated into the Siemens × Nvidia Vera Rubin 136 MW AI data centre reference architecture, marking BESS's elevation from peripheral equipment to a core AI infrastructure component.

Supporting live tables (continuously updated by routine): - Australia Projects Supply Chain · Table C — 41 projects ≥100 MWh (1 update this issue: Orana status → "commissioning complete, full output reached, COD pending") - Chinese Suppliers Overseas Projects · Table A — 1 new entry (Sungrow Chile Librillo 643.8 MWh); now 20 entries - Supplier Profiles · Table B — no updates this issue - Lithium Price History · Table D — 06-03 row added (USD 22,918.04; SMM latest date 2 June, T-1 normal); trend chart updated

Full project supply chain BOM: Table C.

Akaysha Orana BESS (415 MW / 1,660 MWh, NSW): commissioning complete, full output reached, COD pending; BlackRock opens sale data room · RenewEconomy, 2026-06-02

Akaysha Energy confirmed that the Orana BESS (415 MW / 1,660 MWh, Tesla Megapack) located in central-western NSW (near Dubbo) reached full output for the first time during the week and completed its hold point testing (commissioning phase complete). The commercial operation date (COD) is pending final regulatory, market and contractual requirements. Akaysha stated the project was "delivered on time and below budget." Financing was underpinned by the AU$650M deal closed in July 2024, with EnergyAustralia holding a 12-year tolling agreement.

M&A development (AFR Street Talk, same day): BlackRock has opened a data room for a potential sale of Akaysha Energy. Internal financial documents project EBITDA exceeding AU$600M by end-2029, driven by: ① Waratah Super Battery (850 MW / 1,680 MWh, NSW, 5.5-year SIPS contract, currently ~50% capacity due to transformer failure, full recovery targeted end-2026); ② Orana (EnergyAustralia 12-year tolling); ③ Elaine (VIC, 311 MW / 1,244 MWh, Snowy Hydro 15-year virtual tolling, under construction); ④ Ulinda Park P2 (QLD, 350 MW / 780 MWh, under construction); ⑤ newly won SA FERM Brinkworth (250 MW / 1,000 MWh nameplate, 15-year FERMA).

→ For PG: BlackRock's move to exit Akaysha signals that Australian BESS assets have reached a capital market "exit window" in the eyes of major financial institutions. The >AU$600M EBITDA forecast (approximately 2-3 GW of operating assets) provides a direct reference point for PG's project valuation and IRR modelling. PG should track the bidder identity closely - a strategic buyer could accelerate Akaysha's pipeline development and intensify competition.

Source: RenewEconomy (2026-06-02)

Eku Energy Griffith BESS (100 MW / 1,000 MWh, 10-hour, NSW): enters federal EPBC queue; 74 objections may trigger NSW IPC review · RenewEconomy, 2026-06-02

UK developer Eku Energy's Griffith BESS (adjacent to Yoogali solar farm, ~7.5 ha, 132 kV TransGrid substation connection) has been submitted to the federal EPBC environmental assessment. The spec has been upgraded from the original LTESA-contracted 100 MW / 800 MWh (8-hour) to a 10-hour (1,000 MWh) configuration. Federal environmental screening found no threatened species, with fire and flood risks assessed as low - federal clearance is expected to be straightforward.

At the NSW state planning level, the project received 74 objections, with only 1 from a genuine local resident within 650 metres (roads/noise concerns); the remainder came from QLD, TAS, VIC and other NSW regions with template-based submissions (including "foreign investment concerns" and false claims). Under NSW planning rules, once the objection threshold is reached, the project is referred to the NSW Independent Planning Commission (IPC) for secondary review, likely adding 3-6 months to the schedule.

→ For PG: The mass template-style distant-objection phenomenon is becoming widespread across Australian BESS approvals. The IPC referral threshold acts as a planning timeline risk. Should NSW's Prioritising Renewable Energy Bill pass the upper house, PEP designation would bypass IPC with no appeal rights - making Griffith-type cases likely early beneficiaries. PG must embed community engagement strategies from the site selection stage to proactively manage objection volumes.

Source: RenewEconomy (2026-06-02)

QLD BESS Fleet: 79.5% instantaneous renewables-plus-storage record on 31 May; first NEM region to exceed 100 GWh monthly dispatch · Energy-Storage.news, 2026-06-02

On 31 May 2026 at 11:20, Queensland's BESS fleet drove the state's renewables-plus-storage instantaneous consumption share to 79.5%, surpassing the previous state record of 78.4% (13 April 2026). At 10:50 the same day, battery storage alone reached 16.9% of instantaneous consumption (vs ~6.4% a year earlier - nearly a threefold increase). May marked the first time any NEM region's BESS fleet dispatched over 100 GWh in a single month.

Revenue comparison: CleanCo Swanbank (250 MW / 500 MWh) generated AU$743k in May revenue, versus the Victorian Big Battery (450 MWh) at AU$306k - a 2.4× gap. However, intraday spreads in QLD are compressing towards AU$110/MWh or below (SA excepted), signalling increasing saturation.

→ For PG: Rapid BESS capacity additions in QLD are compressing intraday arbitrage margins. A purely merchant BESS business case in QLD requires refreshed revenue modelling; overlaying FCAS and CIS contract revenue is becoming necessary rather than optional. The Swanbank vs. Victorian Big Battery revenue contrast reinforces the strategic value of contract income (LTESA/CIS) as a revenue stabiliser in the NSW/VIC markets where PG is more likely to compete.

Source: Energy-Storage.news (2026-06-02)

CIS Tender 8 (4 GW / 16 GWh dispatchable storage): still under assessment, June award expected · DCCEEW, ongoing

DCCEEW's website (last updated 2026-05-22) shows CIS Tender 8 bids remain "under assessment," with an indicative award timeframe of "June 2026." Bids closed 6 February 2026 - assessment has now run approximately four months. CIS Tender 7 (hybrid, 7.9 GWh, 19 projects) was announced on 26 May; CIS Tender 9 (5 GW generation, federal) opened 25 May (registration deadline 22 June). As of today (03 June), no Tender 8 award announcement has been made.

→ For PG: The Tender 8 award list will directly reveal which developers secured the next 16 GWh of NEM firm capacity contracts and at what regional spread - the most important price signal node currently in the pipeline. PG should monitor the DCCEEW Closed Tenders page and immediately assess overlap with its own pipeline upon announcement.

Source: DCCEEW CIS Tenders (ongoing)

SA FERM Tender 1: "4-hour nameplate, 8-hour dispatch" dual-layer bidding structure explained · RenewEconomy, 2026-06-03

RenewEconomy's 3 June analysis revealed the structural detail behind SA FERM Tender 1's awards: the six FERMA projects have a combined nameplate of 1,334 MW / 5,336 MWh but a contracted committed capacity of only 517 MW / 4,136 MWh. The mechanism requires assets to dispatch continuously for at least 8 hours during Forecast Lack of Reserve (LOR) system stress events. Developers achieve this by building a 4-hour nameplate system, then derate to 50% output during LOR events to deliver 8 hours - optimising capital cost while meeting the contractual requirement.

Akaysha Brinkworth (nameplate 250 MW / 1,000 MWh; committed 92 MW / 736 MWh) and ZEBRE Dartmoor (nameplate 144 MW / 576 MWh; committed 50 MW / 400 MWh) both adopted this structure.

→ For PG: The 4h/8h dual-layer structure is directly transferable to CIS Tender 8 and future FERMA/LTESA bidding strategy. PG's engineering team should assess whether operating a 4-hour system at derated power to achieve 8-hour contractual compliance is technically feasible (PCS derating headroom, thermal management margins) - and if so, optimise CAPEX accordingly while avoiding over-engineering.

Source: RenewEconomy (2026-06-03)

NSW Prioritising Renewable Energy Bill 2026: passed lower house (28 May), now before upper house · Dentons, 2026-05-28

NSW's Energy Legislation Amendment (Prioritising Renewable Energy) Bill 2026 passed the lower house with amendments on 28 May and has been sent to the Legislative Council. Core mechanism: the Energy Minister may designate specific BESS / renewable generation / transmission projects as "Priority Energy Projects (PEPs)." PEPs can: ① bypass the standard IPC consultation process, with the Planning Minister making the determination directly; ② carry no merits appeal rights for either applicant or objectors; ③ access an accelerated statutory approval timeline. A 27 May amendment added a mandatory 12-month review of community engagement quality and benefit-sharing equity. The scheme explicitly excludes coal and nuclear-supporting storage.

→ For PG: If the Bill passes the upper house, PEP designation for a PG NSW BESS project could compress the DA timeline from 12-18 months to approximately 3-6 months - materially important for CIS Tender 10 / NSW LTESA windows. PG should engage Norton Rose Fulbright or Baker McKenzie immediately post-passage to clarify PEP eligibility criteria and required pre-application documentation.

Source: Dentons (2026-05-28)

NEM Settlement Cycle Shortening: final rule effective 2026-08-09 (67 days from today) · AEMO

AEMC's final rule (ERC0384) shortening the NEM settlement cycle from ~30 working days to 9 working days takes effect on 9 August 2026 (from billing period 33 onward). AEMO is implementing the corresponding NEM Settlement Revisions Policy and reconfiguring the settlement calendar. The shorter cycle reduces working capital requirements for BESS operators and accelerates revenue realisation - particularly beneficial for independent project companies with short-term liquidity constraints.

→ For PG: Australian BESS operational cash flow timing will improve from August. PG should verify that all operating assets (if any) and relevant contracts are configured for the new settlement mechanism before 09-08.

AEMO 2026 ISP final version: scheduled for release 2026-06-25 · AEMO

AEMO's 2026 Integrated System Plan (ISP) final version is scheduled for release on 25 June 2026 (22 days from today). The December 2025 draft named BESS as the core component of the NEM's lowest-cost transition pathway. Upon release, the Optimal Development Path (ODP) will define which transmission and storage investments are "actionable" projects, directly shaping CIS, ARENA and state-level funding priorities.

→ For PG: The 25 June ISP will confirm the NEM's 10-20 year storage capacity demand curve. PG should review the ODP's storage gap indicators for target states (NSW / QLD / SA) within one week of release and use them to calibrate project development priorities and Tender 10 bidding strategy.

AEMC Package 2 (NEM large load connection standards): complex submissions may delay final rule beyond mid-year · AEMC

The AEMC consultation period for Package 2 (IBL - Inverter-Based Loads technical standards) closed 7 May, receiving submissions from Tesla, Akaysha, Sungrow, AWS and others (some accepted until 12-15 May). AEMC has stated it "may consider extending the final determination timeline if submissions raise complex issues" - putting the original "mid-year final rule" schedule at risk. Key disputes: the technical threshold for mandatory data centre ride-through (AWS publicly objected) and the contractual framework for HVDC operators purchasing system strength from third parties.

→ For PG: A Package 2 delay into H2 2026 would postpone clarity on mandatory data centre storage obligations. PG should build regulatory uncertainty buffers into any AIDC co-location or PPA business cases that rely on Package 2 obligations as commercial drivers.

Australian projects: Table C; non-Australian projects: Table A; supplier profiles: Table B.

Sungrow × Sonnedix: Chile Librillo BESS 643.8 MWh supply agreement (PowerTitan 2.0, Q1 2027 delivery) · Energy-Storage.news, 2026-05-28

Sungrow signed a 643.8 MWh BESS supply agreement with Spanish IPP Sonnedix for the Librillo BESS project in Chile:

(Added to Table A: entry 20, first recorded 2026-06-03)

→ For PG: Sungrow's PowerTitan 2.0/3.0 global deployment track record continues to expand (Saudi Arabia / UAE / Chile), steadily building lender familiarity with the product line. If PG considers Sungrow for Australian projects, these international PPA-backed reference cases can be used as bankability documentation to support lender due diligence.

Source: Energy-Storage.news (2026-05-28)

Watchlist activity (2026-06-02/03 window)

No new overseas project or order announcements (≥100 MWh threshold) from CATL / BYD / EVE / Hithium / Envision / Trina / REPT / CORNEX / HyperStrong in the 2026-06-02/03 window.

Today's price (sourced: 2026-06-03 07:00 Beijing time)

| Product | Latest price | Reference |

|---|---|---|

| Battery-Grade Lithium Carbonate (SMM) | USD 22,918.04 / tonne (unchanged) / CNY 175,750 / tonne | SMM-Li-LC-001 Avg; SMM latest date 2 June (SMM publishes at ~10:10 Beijing; 07:00 capture is T-1 as expected); down ~0.85% from last Friday USD 23,114; CNY inclusive of 13% VAT, official precise average |

Trend Analysis

06-02 pullback drivers - import volume surge and mining restart expectations; not a trend reversal

Per CarbonCredits.com (2026-06-02) and SMM weekly commentary (2026-05-21), the 06-02 -1.82% move (USD 22,918 / CNY 175,750) was driven by two pressure lines:

① Import restocking volume: China's January-April cumulative lithium carbonate imports totalled ~116,000 tonnes (YoY +47%), with lithium sulphate imports +121%; Chile accounts for ~65% of carbonate imports, and continued external restocking limits the upside on domestic spot prices. ② Mining restart expectations: MinRes's formal Bald Hill restart announcement (19 May) - June mining start, July first concentrate, FY2027 Q1 first shipments from Esperance Port - led market participants to front-run H2 supply additions, triggering profit-taking on elevated positions.

SMM's market sentiment assessment: "buy on dips, wait on rallies" is the current dominant pattern - downstream buyers restocking on price weakness while upstream producers hold inventory; short-term range CNY 174,000-181,000/tonne.

Institutional views

Mine restart milestones (Q3 critical observations)

| Mine | Status | Source |

|---|---|---|

| MinRes Bald Hill (WA) | Formally restarted 19 May 2026; June mining, July first concentrate (5.1% SC, ~165kt/yr dry), FY2027 Q1 first Esperance Port shipments | North Miner |

| Pilbara Minerals Ngungaju (WA) | Board approved restart 19 Feb 2026; July production restart (~200kt/yr); March quarterly confirmed unchanged timeline | PLS quarterly |

| Core Lithium Finniss (NT) | FID 18 March 2026; mining contract awarded April; mining underway from May; Q3 CY2026 first concentrate target | Mining Weekly |

| IGO Greenbushes (WA) | FY2026 guidance cut to 1,375-1,425kt (from 1,500-1,700kt); Q2 quarterly report (late July) is the next critical read | Benchmark MI (2026-04-28) |

→ For PG: The current pullback reflects technical selling ("import pressure + restart expectations") rather than a fundamental demand deterioration - InfoLink and Benchmark's forward curve maintain a H2 bullish bias. The three mine restarts' physical volumes only become visible in Q3; Q2 end to early Q3 (before Bald Hill's first shipment data) remains the period of highest price uncertainty. PG's procurement framework agreement lock-in timing - "post Bald Hill July first mine data" - remains appropriate; simultaneously monitor Greenbushes' July quarterly for any further production downside.

Source: Full ledger at Table D

Fluence Smartstack enters Siemens × Nvidia Vera Rubin AI data centre reference architecture: BESS becomes a core AI infrastructure component · Siemens / Energy-Storage.news, 2026-06-01

Siemens released the DSX Vera Rubin AI Factory Reference Design, built for Nvidia's Vera Rubin NVL72 GPU architecture, with a 136 MW total facility capacity (100 MW IT load) via 34.5 kV grid connection. Fluence Smartstack BESS is the only specified storage solution, delivering four system functions:

Context: Fluence has signed master supply agreements with two hyperscale cloud operators; H1 FY2026 backlog reached US$5.6 billion (doubled YoY). Siemens × Nvidia's reference architecture positions Fluence as a default AI Factory configuration - Australian data centre operators are expected to follow similar reference standards.

→ For PG: AI data centre storage is evolving from "regulatory diesel replacement" to "core AI infrastructure layer," shifting the commercial model from one-time equipment procurement to long-term systems services. Australia's data centre capacity is forecast to grow from 1.4 GW to 3.2 GW by 2030 (AEMO). Once AEMC's ride-through mandate takes effect, PG has an opportunity to explore data centre co-location or BESS-as-a-Service models - competing or partnering with the Australian localisation of the Fluence-style model.

Source: Energy-Storage.news (2026-06-01) · Siemens Press

InfoLink Q1 2026 global ESS cell shipments: 587Ah large cells forecast to reach 20% penetration by year-end · InfoLink Consulting, 2026-Q2

InfoLink Q1 2026 ESS data: global ESS cell shipments of 205.52 GWh (YoY +98.7%, QoQ +1.62%); full-year 2026 forecast revised up to 897 GWh. Structural shift: 500+ Ah cells at ~5% penetration in Q1, forecast to exceed 20% by year-end. The 587/588 Ah format (in volume production at CATL, Hithium, REPT and EVE) is transitioning from "flagship product" to "mainstream specification." CATL's 587Ah Jining facility has reduced per-unit manufacturing cost by 42% vs. 314Ah; system-level CAPEX savings estimated at 10-15%.

→ For PG: The 587Ah / 6.25 MWh system is establishing itself as the engineering standard for 20-foot container large-scale storage. PG should include "587Ah or equivalent next-generation specification" in its 2026-2027 RFQ technical specifications to lock in optimised CAPEX, while retaining "314Ah compatible" as a fallback to maintain competitive coverage.

NSW EIR LDES procurement round: 8-hour-plus long-duration storage, registration window open · ASL / pv-magazine, 2026-05

NSW consumer trustee ASL has opened a new round of long-duration energy storage (LDES) procurement, targeting assets with 8+ hours of duration and commercial operation by 2029 or 2033. The evaluation framework formally scores "system strength and grid service contribution." The registration window is open, with precise deadline and capacity targets pending first-party source verification.

Note: Specific capacity figures and registration deadline cited in this entry are from secondary sources. PG is advised to verify directly with ASL's official website before committing to registration.

→ For PG: NSW LDES procurement and the expected CIS Tender 8 award are running in parallel in June, making this the highest-density policy month for Australian BESS in 2026. Any PG NSW pipeline projects must be evaluated for eligibility this week given the upcoming registration window.

Not available this issue

The Modo Energy article retrieval tool timed out this morning; backup search found no new Australia-NEM articles published after 01 June. The most recent coverage (Neil Weaver, 01 June, cross-market BESS revenue structure analysis) was fully reported in the 2026-06-02 research brief.

This research brief is automatically compiled daily by PGSH's internal research system; each item's source is individually cited. Project updates, policy developments, price data, and institutional views presented herein are for internal reference only and do not constitute investment, procurement, or commercial decision advice. For any item of interest or where action is contemplated, please open the corresponding source link directly to verify the accuracy and currency of the information.