类型:增量 · 覆盖窗口:2026-06-01 ~ 06-02(基线 2026-06-01)

周二。本期核心:CDC Data Centres 于 5 月 6 日锁定澳洲史上最大数据中心合同(555 MW,30 年,美国投资级客户),与 AEMC 正在推进的数据中心强制接网 + 配储分级标准草案(Tier 3:≥100 MW 数据中心须满足全工况并网穿越要求)共同构成澳洲 AIDC 储能需求最具体的政策-商业双重催化信号;CIS Tender 8(4 GW / 16 GWh 纯储能,2 月关标)授标结果进入 6 月关键观察窗口,截至本期仍未落地;SMM 碳酸锂连续第二个交易日上涨,6 月 1 日数据 USD 23,345.63(+1.00%),略超 Goldman Sachs 的峰值预估,高位持续时间再度超出主流机构预期;Modo Energy Neil Weaver 6 月 1 日发布跨市场 BESS 收益结构分析,核心结论:NEM 全年月度收益区间约 A$60k-400k/MW-yr(2023-2025),无集中容量机制底托,随储能规模化将加速向现货套利集中,LTESA/CIS 合同是目前 NEM 项目融资的必要条件;天合 Trina 罗马尼亚 Izvoarele 160 MWh 进入安装阶段,Q3 并网目标不变。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 41 个 ≥100 MWh 项目(本期无新增) - 中国供应商海外项目 · 表 A — 本期更新 1 条(Trina 罗马尼亚阶段:硬件交付 → 安装中);当前 19 条 - 供应商档案 · 表 B — 本期无更新 - 锂价历史 · 表 D — 今日已追加 06-02 行(USD 23,345.63;SMM 最新 Date 6 月 1 日,T-1 正常);趋势图已重画

完整项目供应链 BOM 见 活表 C。

CIS Tender 8(4 GW / 16 GWh):授标窗口已开,截至今日结果尚未落地 · DCCEEW,持续跟踪

DCCEEW 的 Capacity Investment Scheme Tender 8 于 2025 年 11 月开放,目标 4 GW / 约 16 GWh 可调度储能(以 ≥4 小时 BESS 为主),覆盖 NEM 四个区域(NSW / VIC / SA / QLD)。投标截止 2026 年 2 月 6 日,官方明确结果预期在 "2026 年 6 月" 公布。截至 2026-06-02(北京时间),DCCEEW 官网仍将 Tender 8 列于"Open CIS Tenders"页,授标公告尚未发出。

背景与对比:Tender 8 属于专项纯储能招标(非 Tender 7 的混合型);Tender 7 于 5 月 26 日公布(7.9 GWh,19 个项目),Tender 9(5 GW 发电,注册截 6/22,投标截 7/20)同期进行。Tender 10 预计今年稍晚开标。DCCEEW 提示,若提交意见复杂,授标公告可能略有推迟。

→ 对 PG:Tender 8 结果一旦落地,将确认 16 GWh 新增合同的区域分布与中标开发商,是今年 NEM 竞争格局变化最大的单点事件。PG 应持续监控 DCCEEW 官网(Closed CIS Tenders 页);结果公布后需立即评估中标项目与自身接入节点的重叠情况,并相应调整 Tender 10 竞价策略(已知 Tender 10 与 8 时间窗口连续)。

来源:DCCEEW CIS Tenders(持续更新)

本期无新增项目进展(2026-06-01 至 06-02 窗口)

2026-06-01(周一晚)至 2026-06-02(周二早)期间,主要澳洲 BESS 开发商、AEMO、各州政府均无新项目 FID / 开工 / 并网 / 授标公告落地。活表 C 维持 41 个项目。

AEMC Package 2(NEM 接入标准):数据中心分级接网强制框架草案,年中最终规则 · AEMC,2026-03-12 草案

AEMC 于 2026 年 3 月 12 日发布《Improving NEM Access Standards — Package 2》草案,咨询期于 2026 年 5 月 7 日截止,目前正处理提交意见,最终规则预期在 2026 年中落地(如提交意见复杂存在延期风险)。核心内容:

澳洲数据中心当前装机约 1.4 GW(2026 估),Oxford Economics 预测 2050 年升至 32 TWh(占全国 12%)。

→ 对 PG:Tier 3 标准若落地,≥100 MW 数据中心接入 NEM 将需配置 BESS 以满足 ride-through 要求;"full power offset" 方向若成规,意味着每个大型 AIDC 捆绑强制储能量,是 PG 获取 co-location 或定向 PPA 合同的结构性新通道。AEMC 最终规则是今年 7 月前最重要的政策节点,PG 应在规则落地前完成 AIDC 客户的初步接触工作。

来源:AEMC Package 2(2026-03-12)· AFR Full Power Offset(2026-05-11)

Trina Storage 罗马尼亚 Izvoarele BESS 进入安装阶段(Q3 2026 COD 目标不变) · Energy Global,2026-06-01

天合储能欧洲首个 DC+AC 一体化方案(Elementa 2 Pro + Electra AC,40 MW / 160.48 MWh,罗马尼亚 Giurgiu 县 LSG 业主)已由 2026 年 4-5 月硬件到场升级至安装施工中,Q3 2026 并网目标维持不变。这是 05-31 研报记录「硬件交付」后的阶段推进,为 Trina × PG 澳洲 5 GWh 供货框架(2025-11)提供当前最新的供货实物进度参考。(台账 A 已更新,阶段栏改为「安装中·Q3 2026 COD」)

→ 对 PG:Trina 从「硬件交付」到「安装中」的进度推进在 3-4 周内完成,节奏正常;Q3 并网若顺利落地,将是 Trina 在欧洲可引用的首个完整运营参考案例,直接加强澳洲供货框架的 bankability 背书材料库。

来源:Energy Global(2026-06-01)· 更新表 A 2026-06-02

本期 Watchlist 动态(2026-06-01/02 窗口)

2026-06-01/02 搜索窗口内,watchlist 十家供应商(CATL / BYD / EVE / Hithium / Envision / Sungrow / Trina / REPT / CORNEX / HyperStrong)暂未披露新的海外项目或订单公告(≥100 MWh 门槛)。

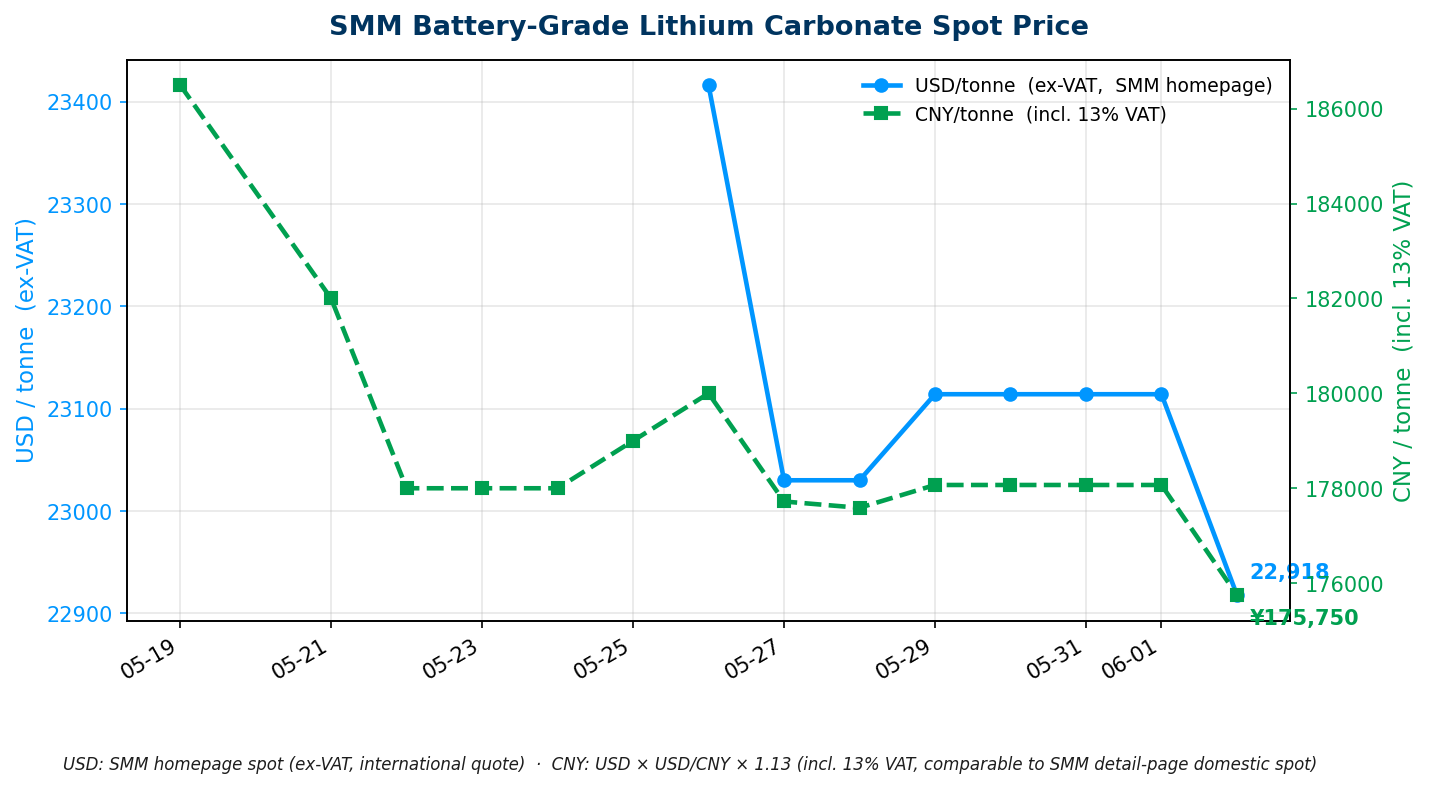

今日价格(口径:2026-06-02 北京时间 07:31 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 23,345.63 / tonne(+231.40,+1.00%)/ CNY 179,828 / 吨 | SMM 首页 SMM-Li-LC-001 Avg;SMM 最新 Date 6 月 1 日(SMM 下午发布当日值,7:30 抓为 T-1 是正常);CNY = 23,345.63 × 6.8167 × 1.13 |

走势分析

价格近况:6 月 1 日 SMM 数据较 5 月 29 日末值(USD 23,114.22)上涨 +231.40(+1.00%),连续第二个交易日正向变动,现货价仍显著高于 Goldman Sachs 此前给出的 H1 2026 峰值预估(约 USD 21,000);UBS 的 5-6 月短期看至 USD 25,000 路径仍在有效射程内。

矿端:三矿复产(MinRes Bald Hill 7 月首矿确认、Pilbara Minerals Ngungaju 7 月重启确认、Core Lithium Finniss Q4 首矿确认)是下半年供给侧最重要的观察节点,实物装船节奏决定 Q3 末至 Q4 的实际供给宽松时点。7 月前卖方底气仍有支撑。

需求端:中国 6 月电芯排产预计 268 GWh(环比 +7.6%,连续第四个月峰值,大东时代 TD,05-26),储能电芯占比首超动力(41.4%),正极厂对 >20 万元/吨高价的采购意愿仍偏谨慎(随用随买)。

本期暂缺:6 月 1-2 日窗口内无新的机构研报(Goldman / UBS / Benchmark / SMM 等)正式发布。最近机构方向已在 05-31 研报中完整覆盖(Benchmark H2 偏多、UBS 上调 18%、Goldman H1 顶部、GFEX 限仓)。

→ 对 PG:价格在三矿实物到岸前维持强势格局,PG Q3 采购框架协议锁价时点判断(以 Bald Hill 7 月首产数据落地后为宜)不变,同步监控 Greenbushes Q2 季报(预计 7 月下旬)是否有运营问题进一步恶化的新信号。

来源:完整台账见 活表 D

CDC Data Centres 锁定澳洲史上最大数据中心合同:555 MW,30 年,美国投资级客户 · Data Center Dynamics / AFR,2026-05-06

ASX 上市基础设施公司 CDC Data Centres 于 2026 年 5 月 5-6 日宣布,与一家未具名美国高评级(investment grade)机构客户签署 555 MW / 30 年数据中心服务合同,是澳洲有史以来规模最大的单笔数据中心商业合同:

→ 对 PG:CDC 555 MW 合同是澳洲 AIDC 需求从规划转向实物的最具体信号,直接拉动 NSW/VIC 区域电网稳定配套需求。AEMC 强制配储规则(年中落地)与 CDC 级别的数据中心合同叠加,意味着 2027-2028 年开工的 BESS 有可能直接对接此类客户的长期配储 PPA。PG 应主动评估在 CDC 数据中心接入节点附近的选址机会。

来源:Data Center Dynamics(2026-05-06)

Alsym Energy × Volta Foundation:NFPP 钠离子路线白皮书,Peak Energy 美国 720 MWh 商业合同落地 · Volta Foundation,2026-05-19

Volta Foundation 发布 2026 年钠离子电池行业综述,要点: - NFPP(钠铁焦磷酸盐)路线被 Alsym 认定为电网储能最优化学路径,宣称可实现 95-98% DoD,不需主动 HVAC 冷却(冷却能耗降低最高 90%);Benchmark MI 预测全球钠电产量从当前 ~70 GWh 增至 2030 年约 400 GWh(CAGR 41.7%) - Peak Energy × Jupiter Power(美国):720 MWh utility-scale 合同已签,另有潜在 4 GWh 追加意向 - 是美国本土非中国钠离子 BESS 的首批规模化落地案例

→ 对 PG:NFPP 无需主动冷却的特性对澳洲高温区域(QLD / WA 内陆)的防火与 HVAC 成本节约有潜在价值,2027 年以后系统报价将出现实质竞争压力。当前 LFP 仍是 2026-28 采购窗口的主流,但 RFQ 文件中可预留「替代化学体系」条款框架。

来源:Volta Foundation(2026-05-19)

今日无新增

「电价走势如何影响储能收益?」跨市场 BESS 收益结构分析(Neil Weaver,2026-06-01)

Modo Energy 6 月 1 日发布跨六大市场 BESS 收益结构报告,涵盖 ERCOT / CAISO / GB / DE / 西班牙 / 澳洲 NEM,核心结论与 NEM 直接相关指标如下:

NEM 核心数据(首次公开): - 月度收益区间:约 A$60k-400k/MW-yr(2023-2025),最好月与最差月相差约 6 倍,体现 NEM 高度波动的 merchant 特性 - 2023-2025 趋势:NEM 收益总体向上(ERCOT / CAISO 因 FCAS 饱和明显下滑,NEM 反向走高) - 结构特征:NEM 是六大市场中唯一既无 Resource Adequacy(美式)又无集中容量市场(欧式)底托的市场,FCAS + 现货套利是全部收入来源

核心机制(全市场适用): - BESS 收益追踪的是日内电价价差(spread)而非电价均值 - 低均价市场若日内价差剧烈,收益可与高均价市场相当 - 随 BESS 装机规模化,FCAS 等可调度性服务收益率因竞争而饱和,收益向现货套利集中是普遍规律(ERCOT 辅助服务占比 2023 年 84% → 2025 年 35%;德国 2030 年预计从 88% 降至 5%) - NEM 已完成这一转轮,当前现货套利为收益主体

五项投资者关注指标(Modo 框架): 1. 辅助服务饱和阶段判断(NEM 已进入中期饱和) 2. 商运时点(COD timing)- 套利峰值区间的并网优先级 3. merchant vs 合约收益比例(NEM 无集中机制,LTESA/CIS 是唯一结构性底托) 4. 位置与电网拥堵暴露度(NEM 的 MLF 效应是最大变量) 5. 需求增长实现率(数据中心负荷预测落地节奏)

→ 对 PG:Modo 数据证实 NEM BESS 月度收益最高可达 A$400k/MW-yr(约年化 A$5M/MW),但最低月仅约 A$60k,标准差极大;这意味着纯 merchant 方案对 PG 的债务融资会遇到银行要求更高的利率溢价(收入不可预测)。LTESA/CIS 合约锁定基础收益底线,是满足贷款方 DSCR 要求的实质路径,而非可选项。位置(MLF)选择次之 - 拥堵带来的套利溢价在 NEM 输电扩张前(EnergyConnect Stage 2 本年 10 月完工)仍有支撑。

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental · Coverage Window: 2026-06-01 ~ 06-02 (Baseline: 2026-06-01)

Tuesday. Key highlights: CDC Data Centres secured Australia's largest-ever data centre contract (555 MW, 30 years, US investment-grade client) on 5 May, which — alongside AEMC's draft tiered mandatory grid-access and co-located storage framework for data centres (Tier 3: ≥100 MW data centres must satisfy full-condition fault ride-through) — represents the clearest dual policy-commercial catalyst yet for AIDC-driven BESS demand in Australia. CIS Tender 8 (4 GW / 16 GWh, closed February) is in its expected June announcement window but remained unpublished as of this issue. SMM battery-grade lithium carbonate rose for the second consecutive trading day: 1 June data shows USD 23,345.63 (+1.00%), again exceeding Goldman Sachs's peak estimate and sustaining a higher-for-longer trajectory. Modo Energy analyst Neil Weaver published a cross-market BESS revenue structure report on 1 June: NEM monthly revenue ranged approximately A$60k-400k/MW-yr (2023-2025); the NEM has no centralised capacity mechanism backstop; as storage scales, revenue will increasingly concentrate in wholesale arbitrage; LTESA/CIS contracts remain a necessary condition for NEM project financing. Trina Storage's Romania Izvoarele 160 MWh project is now in the installation phase, with the Q3 commissioning target intact.

Supporting Live Tables (continuously updated by routine): - Australia Project Supply Chain · Table C — 41 projects ≥100 MWh (no new additions this issue) - China Supplier Overseas Projects · Table A — 1 update this issue (Trina Romania stage: hardware delivered → installation underway); 19 entries total - Supplier Profiles · Table B — no updates this issue - Lithium Price History · Table D — 06-02 row appended (USD 23,345.63; SMM Date 1 June, T-1 normal); price chart updated

Full project supply chain BOM: Table C.

CIS Tender 8 (4 GW / 16 GWh): June announcement window open, no result published as of today · DCCEEW, ongoing

DCCEEW's Capacity Investment Scheme Tender 8 opened in November 2025, targeting 4 GW / ~16 GWh of dispatchable storage (primarily ≥4-hour BESS) across four NEM regions (NSW / VIC / SA / QLD). Bidding closed 6 February 2026; official guidance stated results expected in "June 2026". As of 2026-06-02 (Beijing time), the DCCEEW website still lists Tender 8 under "Open CIS Tenders" — no award announcement has been made.

Context: Tender 8 is a pure storage tender (distinct from Tender 7's hybrid format); Tender 7 results were published 26 May (7.9 GWh, 19 projects). Tender 9 (5 GW generation, registration closes 22 June, bidding closes 20 July) is running concurrently. Tender 10 expected later in the year. DCCEEW has noted that complex submissions may delay the final announcement.

→ For PG: Once Tender 8 results are published, they will reveal the regional distribution of 16 GWh of new contracts and which developers won — the single largest competitive landscape shift of the year. PG should continuously monitor the DCCEEW website (Closed CIS Tenders page); immediately upon announcement, assess overlap between awarded projects and PG's own grid access nodes, and adjust Tender 10 bidding strategy accordingly (Tender 10 timing follows immediately after Tender 8 announcement).

Source: DCCEEW CIS Tenders (continuously updated)

No new project announcements this issue (2026-06-01 to 06-02 window)

Between 1 June (Monday evening) and 2 June (Tuesday morning), no new BESS project FID / construction start / commissioning / award / environmental approval announcements were made by major Australian BESS developers, AEMO, or state governments. Table C remains at 41 projects.

AEMC Package 2 (NEM Access Standards): draft tiered mandatory framework for data centre grid connection, final rule mid-year · AEMC, draft 2026-03-12

AEMC published the Improving NEM Access Standards — Package 2 draft determination on 12 March 2026; consultation closed 7 May 2026; submissions are being processed and the final determination is expected mid-2026 (with possible extension if submissions are complex). Key content:

Australia currently operates ~1.4 GW of data centre capacity (2026 est.); Oxford Economics projects this reaching 32 TWh annually by 2050 (~12% of national electricity).

→ For PG: If Tier 3 standards take effect, ≥100 MW data centres connecting to the NEM will require BESS to satisfy ride-through requirements; if "full power offset" becomes binding, every large AIDC will carry a mandated storage obligation — creating a structural new channel for PG to secure co-location or offtake PPA contracts. The AEMC final rule is the most important policy node before July this year; PG should complete initial AIDC client engagement ahead of the rule's publication.

Sources: AEMC Package 2 (2026-03-12) · AFR Full Power Offset (2026-05-11)

Australia projects: Table C; non-Australia projects: Table A; supplier profiles: Table B.

Trina Storage Romania Izvoarele BESS enters installation phase (Q3 2026 COD target unchanged) · Energy Global, 2026-06-01

Trina Storage's first DC+AC integrated solution in Europe (Elementa 2 Pro + Electra AC, 40 MW / 160.48 MWh, Giurgiu County, Romania; owner: LSG) has progressed from hardware arrival (April-May 2026) to active installation; Q3 2026 grid connection target is unchanged. This is a stage advancement from the "hardware delivered" entry recorded in the 31 May report, providing the most current delivery progress reference for the Trina × PG Australia 5 GWh supply framework (2025-11). (Table A updated: stage column revised to "Installation underway · Q3 2026 COD")

→ For PG: Trina's progression from "hardware delivered" to "installation underway" within 3-4 weeks is on a normal schedule; if Q3 commissioning proceeds smoothly, this becomes Trina's first complete operational reference case in Europe, directly strengthening the bankability evidence package for the Australia supply framework.

Source: Energy Global (2026-06-01) · Table A updated 2026-06-02

Watchlist dynamics this issue (2026-06-01/02 window)

Within the 1-2 June search window, no new overseas project or order announcements (≥100 MWh threshold) were identified for any of the ten watchlist suppliers (CATL / BYD / EVE / Hithium / Envision / Sungrow / Trina / REPT / CORNEX / HyperStrong).

Today's price (captured: 2026-06-02 07:31 Beijing time)

| Grade | Latest price | Source |

|---|---|---|

| Battery-grade lithium carbonate (SMM) | USD 23,345.63 / tonne (+231.40, +1.00%) / CNY 179,828 / tonne | SMM homepage SMM-Li-LC-001 Avg; SMM Date: 1 June (SMM publishes same-day data after afternoon settlement, T-1 at 07:30 is normal); CNY = 23,345.63 × 6.8167 × 1.13 |

Market commentary

Price trend: The 1 June SMM print rose USD 231.40 (+1.00%) from the last reported value (USD 23,114.22 as of 29 May), the second consecutive positive move. Spot prices remain materially above Goldman Sachs's H1 2026 peak estimate (~USD 21,000); UBS's 5-6 June short-term target of up to USD 25,000 remains within range.

Mine supply: Three-mine restart (MinRes Bald Hill July first ore confirmed, Pilbara Minerals Ngungaju July restart confirmed, Core Lithium Finniss Q4 first ore confirmed) represents the most important supply-side inflection window in H2 2026. Physical shipment timing will determine the earliest point at which supply loosening reaches spot markets (estimated Q4 2026 at earliest). Seller pricing leverage remains supported until Bald Hill first-ore data is in hand.

Demand: China's June lithium cell production volume is forecast at 268 GWh (month-on-month +7.6%, fourth consecutive record month, per TD Intelligence, 26 May); storage cells' share exceeded EV cells for the first time at 41.4%. Cathode producers remain in a "buy as needed" mode at >CNY 200,000/tonne prices.

This issue - not available: No new institutional research reports (Goldman / UBS / Benchmark / SMM etc.) were published in the 1-2 June window. The latest institutional views are fully covered in the 31 May report (Benchmark H2 bullish, UBS +18% price revision, Goldman H1 peak, GFEX position limit tightening).

→ For PG: Prices are holding firm ahead of the three-mine physical arrivals. The 06-01 SMM print (+1.00%) reinforces the view that the procurement framework timing (targeting the window after Bald Hill July first-ore data) remains appropriate; additionally monitor Greenbushes Q2 quarterly report (expected late July) for any further deterioration in operational issues.

Source: Full price history at Table D

CDC Data Centres locks in Australia's largest-ever data centre contract: 555 MW, 30 years, US investment-grade client · Data Center Dynamics / AFR, 2026-05-06

ASX-listed CDC Data Centres announced on 5-6 May 2026 that it had signed a 555 MW / 30-year data centre services contract with an undisclosed US investment-grade institutional client — the largest single data centre commercial contract ever signed in Australia:

→ For PG: The CDC 555 MW deal is the clearest evidence yet that Australian AIDC demand has moved from planning to executed contracts, directly stimulating grid stability requirements in NSW/VIC. With AEMC's mandatory co-location rules expected mid-year, projects of this scale will likely need BESS as a precondition. PG should assess site selection near CDC's data centre access nodes as a priority.

Source: Data Center Dynamics (2026-05-06)

Alsym Energy × Volta Foundation: NFPP sodium-ion pathway white paper; Peak Energy × Jupiter Power US 720 MWh commercial contract executed · Volta Foundation, 2026-05-19

Volta Foundation's 2026 sodium-ion industry survey highlights: - NFPP (Sodium Iron Pyrophosphate) chemistry identified by Alsym as the optimal pathway for grid storage: claimed 95-98% DoD, no active HVAC cooling required (cooling energy consumption reduced up to 90%); Benchmark Mineral Intelligence forecasts global sodium-ion production growing from ~70 GWh today to ~400 GWh by 2030 (CAGR 41.7%) - Peak Energy × Jupiter Power (US): 720 MWh utility-scale contract executed, with potential 4 GWh follow-on — the first utility-scale non-Chinese sodium-ion BESS deployment in the US

→ For PG: NFPP's no-active-cooling characteristic has potential cost reduction relevance in Australia's high-temperature regions (QLD / WA inland) from a fire safety and HVAC perspective; commercial pressure on LFP pricing from sodium-ion alternatives will build from 2027 onwards. LFP remains the only mainstream option for the 2026-28 procurement window, but RFQ templates could pre-emptively include an "alternative chemistry" clause.

Source: Volta Foundation (2026-05-19)

No new additions this issue

"How do power prices affect battery storage returns?" — Cross-market BESS revenue structure analysis (Neil Weaver, 2026-06-01)

Modo Energy published a six-market BESS revenue structure report on 1 June, covering ERCOT / CAISO / GB / DE / Spain / Australia NEM. Core findings and NEM-specific data:

NEM key data (first-time disclosure): - Monthly revenue range: approximately A$60k-400k/MW-yr (2023-2025) — best months are ~6x worst months, reflecting the NEM's highly volatile fully-merchant character - 2023-2025 trend: NEM revenue trended upward while ERCOT and CAISO declined due to FCAS/ancillary saturation; this divergence confirms NEM's different stage on the market maturation curve - Structural feature: The NEM is the only market of the six with neither Resource Adequacy (US model) nor a centralised capacity market (European model) as a revenue backstop; FCAS + energy arbitrage constitute the full revenue stack

Core mechanism (applicable across all markets): - BESS returns track intraday price spreads, not average price levels — a low-average-price market can still produce strong battery revenue if its daily price shape is volatile - As BESS fleets scale, dispatchable ancillary services (FCAS) saturate because the grid's ancillary requirement is fixed; revenue therefore concentrates in wholesale arbitrage — a universal pattern (ERCOT ancillary share: 84% in 2023 → 35% in 2025; Germany forecast at 88% → 5% by 2030) - The NEM has completed this rotation; wholesale arbitrage is already the dominant revenue source

Five investor monitoring indicators (Modo framework): 1. Ancillary saturation stage (NEM in mid-stage saturation) 2. Commercial operation timing (COD timing relative to spread peak) 3. Merchant vs. contracted revenue mix (NEM has no centralised mechanism — LTESA/CIS is the only structural backstop) 4. Locational and grid congestion exposure (NEM's MLF effect is the largest single variable) 5. Demand growth delivery rate (data centre load forecast realisation pace)

→ For PG: Modo data confirms NEM BESS monthly revenue can reach A$400k/MW-yr (~A$5M/MW annualised) in peak months, but troughs at ~A$60k — a ~6x swing that makes pure-merchant debt financing difficult (lenders require higher rate premiums for unpredictable revenue). LTESA/CIS contracts locking in a base revenue floor are the practical path to meeting lender DSCR requirements, not an optional enhancement. Location (MLF) is the secondary variable — congestion premium in the NEM remains supported before new transmission infrastructure (EnergyConnect Stage 2 completing October this year) alleviates bottlenecks.

Source: Modo Energy 2026-06-01

This research brief is compiled daily by PGSH's internal research system; all entries are cited individually by source. Project progress, policy developments, price data, and institutional views cited herein are for internal reference only and do not constitute investment, procurement, or commercial decision advice. For any item of interest or intended action, please open the corresponding source link directly to verify accuracy and currency of the information.