类型:增量 · 覆盖窗口:2026-05-31 ~ 06-01(基线 2026-05-31)

周一,6 月首日。本期核心:全球最大锂矿 IGO Greenbushes FY2026 精矿产量指引下调 8-9%(150-170 万吨 → 138-143 万吨),与市场预期的三矿复产方向相反,是对本轮锂价中期叙事影响最大的新扰动;广期所(GFEX)收紧碳酸锂期货持仓限额是 5 月下旬回调的结构性助推因素;6 月电芯排产预计 268 GWh(环比 +7.6%,连续第四个月刷新历史峰值),500+ Ah 大电芯渗透率快速攀升;LG Energy Solution × DTE Energy $16 亿 ESS 合同直接服务 Oracle AI 数据中心,是「AI 数据中心直接拉动 BESS 采购」迄今最清晰的商业案例;澳洲《Prioritising Renewable Energy Bill 2026》赋权能源部长建立 50 工作日快速审批通道;供应商侧补录三条:Hithium 西班牙纳瓦拉 €400M 电池工厂(2027 年投产,西班牙总理见证)、Trina 意大利 Rondissone 1 GWh(CRM 拍卖中标)、BYD 保加利亚 Maritsa East 3 500 MWh(已并网,东欧最大)。

配套活表(持续累积,routine 每日更新): - 澳洲项目供应链 · 表 C — 41 个 ≥100 MWh 项目(本期无新增,周末无公告) - 中国供应商海外项目 · 表 A — 本期新增 3 条(Hithium 西班牙工厂 / Trina 意大利 1 GWh / BYD 保加利亚 500 MWh 补录);当前 19 条 - 供应商档案 · 表 B — 本期无更新 - 锂价历史 · 表 D — 今日已追加 06-01 行(USD 23,114.22;SMM 最新 Date 5 月 29 日,周末休市沿用,下午更新为 6 月 1 日数据);趋势图已重画

完整项目供应链 BOM 见 活表 C。

本期无新增项目进展(2026-05-31 至 06-01 周末窗口)

2026-05-31(周日)至 2026-06-01(周一早上)期间,主要澳洲 BESS 项目方、AEMO、各州政府均无新公告落地。周末期间属正常暂停窗口。

CIS Tender 8(16 GWh 可调度储能):进入 6 月公布观察窗口

DCCEEW 于 2025-11-28 开放、2026-02-06 截标的 CIS Tender 8(目标 4 GW / 约 16 GWh,≥4 小时时长,含首次开放聚合项目通道:同一 NEM 区域内 ≥5 MW 可聚合至 ≥30 MW 投标)结果,官方确认「2026 年 6 月公布」。截至今日(6 月 1 日)尚未落地,本周为关键观察窗口。结果公布将直接揭示 NEM 下一批独立储能合约接受者,是当前管线最重要的价格信号节点。

→ 对 PG:Tender 8 结果落地后,PG 应立即核查中标项目与自身管线的接入节点重叠情况,并据此调整 Tender 10(预计 6 月同期开标)的竞价策略。CIS Tender 10(新一轮可调度容量)时间窗口随 Tender 8 结果公布即开放,需提前 4-6 周准备申报包。

NSW《Prioritising Renewable Energy Bill 2026》:能源部长获快速审批赋权,50 工作日联邦目标 · PV Tech / Norton Rose Fulbright,2026-05-07

NSW 议会 2026-05-07 提案《Prioritising Renewable Energy Act 2026》,核心内容:

→ 对 PG:NSW 快速审批通道若获「优先」认定,BESS 项目 DA 周期从 12-18 个月压缩至 3-6 个月,对 CIS Tender 10 / NSW LTESA T9 这类时间紧迫窗口的项目推进有实质意义。PG 在 NSW 有在研项目的情况下,应向 Norton Rose Fulbright / Baker McKenzie 确认「优先识别」申请路径和前置条件(项目阶段、社区参与文件要求)。

来源:PV Tech(2026-05-07)· Norton Rose Fulbright

CIS Tender 9(5 GW 发电,2026-05-25 开标)时间线倒计时

注册截止:2026-06-22(21 天后);投标截止:2026-07-20;结果预计 2026-11。NSW 不可参与;VIC 纯光伏限额 470 MW(光储混合不受限);First Nations Set Aside 500 MW 专属配额(≥5% 股权 / 收益分享);评审权重:财务价值 35%(原 50%)、可交付性 20%(原 12.5%)、组织 / 融资能力 20%(原 12.5%)、社会价值 25%。

→ 对 PG:6 月 22 日注册窗口倒计时,PG 有意参与的 QLD / SA / VIC / TAS 项目须在本周内完成可行性评估并决定是否注册。First Nations 500 MW 专属池竞争强度显著低于主池,若项目具备 ≥5% 土著合作结构,应优先进入该通道。

Hithium 西班牙纳瓦拉 €400M 电池 Gigafactory 正式签约(电芯制造 + BESS 系统集成双功能工厂) · Energy-Storage.news,2026-04-17

海辰储能(Hithium)与纳瓦拉大区政府签署正式投资承诺协议,西班牙总理 Pedro Sánchez 及纳瓦拉主席出席见证:

已进表 B 的 Hithium 档案(西班牙工厂条目)与此同步确认,bankability 维度从「项目交货记录」升级至「本地固定资产投入」。

→ 对 PG:Hithium 欧洲本地工厂落地后,其电芯在欧洲项目中的供应链认可度(银行尽调、lender 工程师报告)将大幅提升。若 PG 在欧洲有项目(或与欧洲融资方合作),Hithium 将成为 CATL/BYD 之外更具竞争力的备选;若在澳洲采购,Hithium 欧洲工厂可作为「全球供应链稳定性」的额外背书材料。

来源:Energy-Storage.news(2026-04-17)· 首记 2026-06-01(进表 A)

Trina Storage × Aer Soléir 意大利 Rondissone BESS(1 GWh / 250 MW,CRM 拍卖中标) · Trinasolar EU,2026-01-20

天合储能与爱尔兰开发商 Aer Soléir(背后为 Invenergy)签署合同,建设意大利迄今最大 BESS 项目:

→ 对 PG:意大利 CRM 拍卖中标是 Trina Storage 获得欧洲政府容量合同的直接证据 - 与英国 CM、澳洲 FERM/CIS 属同类机制。这份合同使 Trina 在 PG 澳洲供货框架(2025-11 签署)中的政府合同 track record 进一步丰富。建议 PG 向 Trina 要求提供 CRM 合同摘要作为 bankability 证明文件。

来源:Trinasolar EU(2026-01-20)· ESS-News(2026-01-23)· 首记 2026-06-01(进表 A)

【补录】BYD 保加利亚 Maritsa East 3 BESS(500 MWh,东欧最大)已并网 · CNESA,2026-01-08

比亚迪完成欧洲迄今最大储能项目之一:

→ 对 PG:东欧 BESS 市场由中国供应商主导已成既成格局,两案可作为 PG 与 BYD 谈判时引用的供货实证;BYD 保加利亚案例时间比 CATL 早,但媒体曝光度较低,是 PG 向 lender 展示 BYD bankability 时被低估的可用素材。

来源:CNESA(2026-01-26)· 首记 2026-06-01(进表 A,补录)

本期 Watchlist 动态(2026-05-31 / 06-01 窗口)

2026-05-31(周日)至 2026-06-01(周一早)搜索窗口内,watchlist 十家供应商(CATL / BYD / EVE / Hithium / Envision / Sungrow / Trina / REPT / CORNEX / HyperStrong)暂未披露新的海外项目或订单公告(≥100 MWh 门槛)。

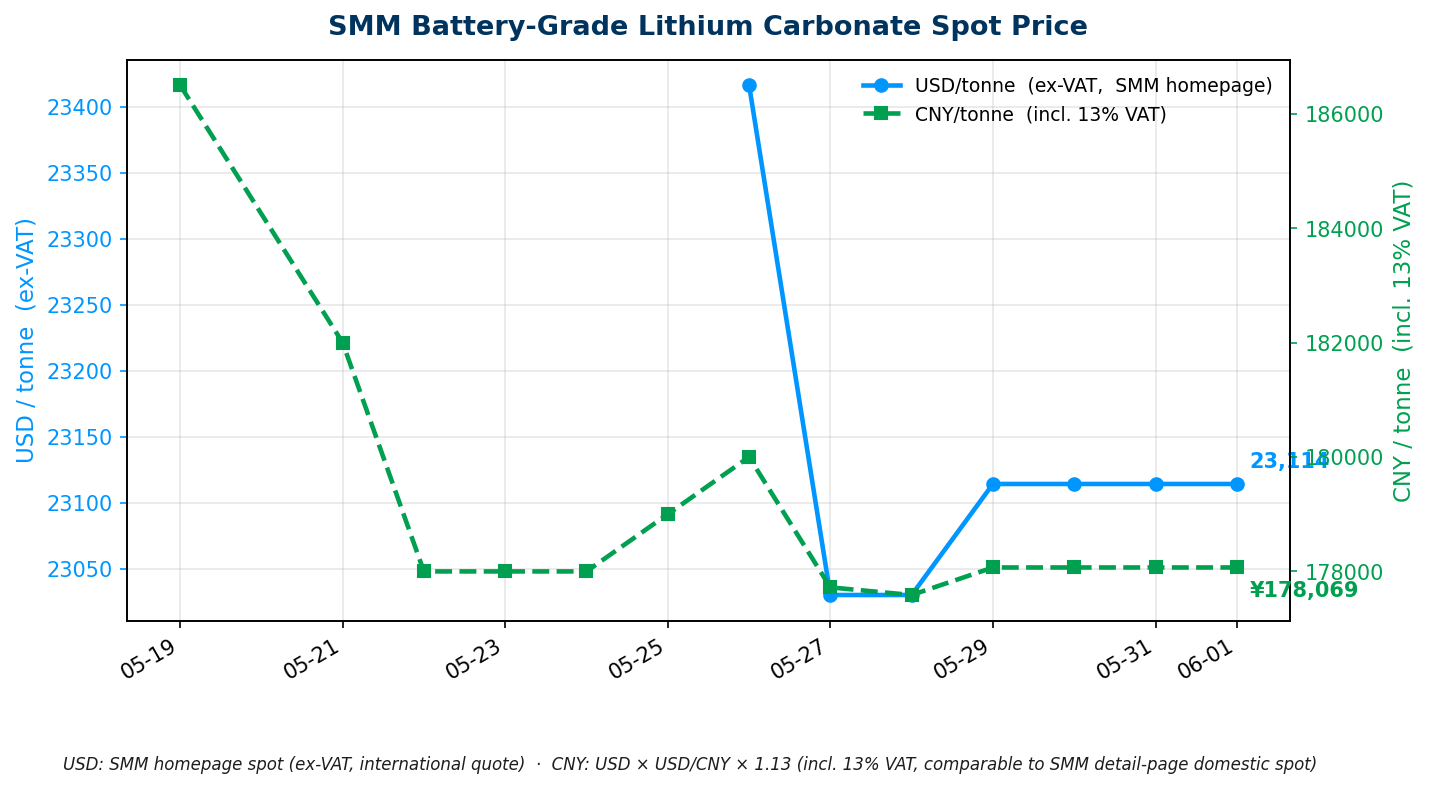

今日价格(口径:2026-06-01 北京时间 07:31 采集)

| 品种 | 最新价 | 口径 |

|---|---|---|

| 电池级碳酸锂(SMM) | USD 23,114.22 / tonne(0,0.0%)/ CNY 178,069 / 吨 | SMM 首页 SMM-Li-LC-001 Avg;SMM 最新 Date 5 月 29 日(周末双休,7:31 抓为 T-3 是正常;下午将更新为 6 月 1 日数据);CNY = 23,114.22 × 6.8176 × 1.13 |

走势分析

矿端新扰动(重要):Greenbushes 全球最大锂矿产量指引下调,Benchmark 估算 H1 少供约 17 万吨 SC

IGO / Greenbushes(全球最大锂辉石矿,澳大利亚西澳,产能约全球 20%)于 2026-04-23 发布季报,将 FY2026 精矿产量指引从此前约 150-170 万吨(dry metric tonnes)下调至约 138-143 万吨,降幅约 8-9%。核心原因:矿石品位下滑速度超出预期(ore grade decline)+ 系统性运营问题(systemic operational issues)。IGO 股价 5 月 21 日再跌 6.3%,市场对运营问题持续性存疑。

Benchmark Mineral Intelligence(2026-04-28)评估:Greenbushes 这次降量意味着 H1 2026 全球锂辉石供给将比原预期少约 17 万吨 SC(spodumene concentrate),在已报的津巴布韦禁矿 + 江西换证双重压力之外,形成第三重供给侧约束。方向与三矿复产(MinRes Bald Hill + Pilbara Ngungaju 7 月、Core Lithium Finniss Q4)相反 - 两组信号叠加使 Q3 供给实物平衡时点的不确定性显著上升。

来源:IGO ASX 季报(2026-04-23)· Benchmark MI(2026-04-28)

广期所(GFEX)收紧碳酸锂期货持仓限额(2026-05-28)

广州期货交易所 5 月 28 日宣布调整规则:自 LC2610 合约起,单边持仓规模 6 万手以下时,非套保账户限额从持仓量的 10% 收窄至 3,000 手;6 万手以上时限额从 10% 降至 5%。产业套保账户不受影响。该政策被市场解读为监管层在价格快速上冲阶段主动介入去杠杆,是 5 月 13 日现货触近两年新高(CNY ~200,500/吨)后连续回调的制度性催化剂之一。

分析:GFEX 限仓 + Goldman Sachs「H1 2026 顶部」判断 + InfoLink 高价下游意愿弱三者协同,解释了 5 月中旬后的价格回调机制;但 Greenbushes 减产 + 三矿复产节奏不确定 + UBS 供给下调,使「回调 = 趋势逆转」的论断仍不成立。

来源:中国证券报(2026-05-28)

需求端:中国 6 月电芯排产预计 268 GWh(环比 +7.6%),500+ Ah 大电芯快速渗透

大东时代智库(TD)5 月 26 日预测,6 月中国锂电(储能 + 动力 + 消费)总排产约 268 GWh(环比 +7.6%),连续第四个月刷新历史峰值;全球预计 281 GWh(+7.3%)。结构亮点:储能电芯占比 41.4%,首次超越动力电芯成为第一大场景。同期,500+ Ah 大电芯(亿纬 628 Ah + CATL 587 Ah)Q1 渗透率约 5%,年底预计接近 20%,带动旧规格(314 Ah)产线出现材料断供风险。排产高增的另一面:上游正极材料供给偏紧,材料端话语权正在向上游再分配。

来源:东方财富(2026-05-26)

机构观点:UBS 上调 2026 年中国锂价预测 18%

UBS 瑞银(2026-05-07/08 研报)将 2026 年中国碳酸锂现货均价预测上调 18% 至 CNY 20 万/吨,预计 5-6 月短期或触及 25 万/吨高点;核心驱动:储能电池需求同比 +60%。GS 同期维持 H1 2026 顶部 + 2026H2-2028 回落路径判断(USD 10,100-16,000),两家对下半年走势仍存在结构性分歧。Benchmark MI(2026-06-25 Webinar 预告)将首次公开发布含锂前向曲线 + 价格风险监测(VaR)工具,届时或提供新的量化锚点。

来源:Moomoo / UBS(2026-05-07/08)

→ 对 PG:Greenbushes 减产是本期最重量级的供给侧新信息,打破了「只有三矿复产,供给必然宽松」的单向叙事。UBS 上调均价预测 + GFEX 限仓引发的价格回调相互叠加,意味着 Q3 实物价格区间(USD 20,000-25,000)可能比 GS 预期更宽。PG 采购框架协议锁价时点仍以「Bald Hill 7 月首产数据落地后」为宜,但须同步监控 Greenbushes 运营问题的 Q2 季报进展(预计 7 月下旬发布)。

来源:完整台账见 活表 D

LG Energy Solution × DTE Energy $16 亿 ESS 合同:AI 数据中心直接拉动电网级 BESS 采购 · Korea Herald,2026-05-28

LG Energy Solution 与密歇根州最大电力公司 DTE Energy 签署 6 GWh / 约 $16 亿(US$) 的 ESS 电芯供货合同(2 年期),是迄今「AI 数据中心 → 电力公司 → 大规模 BESS 采购」链条最完整的商业案例:

→ 对 PG:「电力公司出面采购 BESS → 分配到多个项目 → 其中包括数据中心」的 DTE 模式,提供了澳洲类似结构的参照蓝本。AEMO 数据中心(2030 年 3.2 GW)强制配储政策在 7 月将有 AEMC 方案,届时澳洲有望出现类似的大型合并采购需求。PG 可主动接触 AusNet / TransGrid 等电力公司,探讨「DNSP 或 NSP 集中采购 BESS 为多个数据中心客户服务」的聚合开发路径。

来源:Korea Herald(2026-05-28)

Greenpeace 澳洲《能量吸血鬼》报告:数据中心或占 2040 年澳洲用电量 13%,呼吁暂停审批 · Greenpeace Australia,2026-05-27

Greenpeace 澳洲太平洋发布报告,援引 AEMO 数据:到 2040 年数据中心可能占澳洲全国总用电量的 13%。核心诉求:① 现有数据中心运营商无法实质证明「新增可再生能源」(additionality)主张;② 澳洲已出现数据中心驱动的燃气扩张迹象(单个项目或抹掉 NSW 2028 年全部减排量);③ 呼吁立即实施数据中心开发暂停令,直至完成保障立法。

Greenpeace 立场与 AEMC / DCCEEW(数据中心必须配储,7 月方案)方向相反,可能在公众舆论层面构成数据中心 + 配套可再生项目的审批阻力。

→ 对 PG:澳洲数据中心储能市场的监管和舆论环境正趋复杂。若暂停令诉求引发监管收紧,可能延缓部分 AIDC 开发进程;但若政府只收紧「绿电 additionality 要求」(而非叫停开发),BESS 配储需求反而更刚性。PG 在含数据中心场景的项目方案中,须明确提供「新增可再生能源真实性」证明路径(如专项 PPA + 时间戳匹配),以符合未来可能落地的合规要求。

来源:Greenpeace Australia(2026-05-27)

今日无新增

2026-05-31 至 06-01 窗口内,GFM、电芯规格、系统设计方向暂无新公告落地(已报:CATL ESVL 测试基地 + Sungrow GFM TÜV 双认证 + Trina Elementa 3)。

今日无新增

本期(2026-05-31 ~ 06-01 窗口)Modo 澳洲相关文章检索:无新发布文章。最近两篇(Frances Hallen「NEM 太阳能捕获率」[source_id:23434] 和 Tom Derrick「NEM 市场展望 Q2 2026」[source_id:23436],均为 2026-05-29 发布)已在 2026-05-29 研报中完整覆盖。

本期暂缺

本研报由 PGSH 内部研究系统每日自动汇编,各条目信源已逐条标注。所列项目进展、政策动态、价格数据、机构观点等仅供内部参考,不构成投资、采购或商业决策建议。如对任何条目感兴趣或拟据此行动,请直接打开对应来源链接深入核实信息的准确性与时效性。

Type: Incremental · Coverage window: 2026-05-31 ~ 06-01 (baseline 2026-05-31)

Monday, first day of June. Headlines this issue: the world's largest lithium mine, IGO Greenbushes, cut its FY2026 spodumene concentrate production guidance by 8-9% (1.50-1.70 Mt → 1.38-1.43 Mt) — the opposite direction to the market-expected three-mine restart, and the single most consequential new disturbance to the medium-term lithium-price narrative this cycle. The Guangzhou Futures Exchange (GFEX) tightened lithium carbonate futures position limits, a structural driver behind the late-May pullback. China's June cell production schedule is projected at 268 GWh (+7.6% MoM, a fourth consecutive monthly record high), with 500+ Ah large-format cells penetrating rapidly. The LG Energy Solution × DTE Energy US$1.6bn ESS contract directly serves an Oracle AI data center — the clearest commercial case yet of "AI data centers directly pulling BESS procurement." Australia's Prioritising Renewable Energy Bill 2026 empowers the energy minister to set up a 50-business-day fast-track approval channel. Three supplier additions backfilled: Hithium's €400M battery plant in Navarra, Spain (online 2027, witnessed by the Spanish PM); Trina's Rondissone 1 GWh in Italy (won via CRM auction); and BYD's Maritsa East 3 500 MWh in Bulgaria (grid-connected, the largest in Eastern Europe).

Companion living tables (continuously accumulated, updated daily by the routine): - Australia project supply chain · Table C — 41 projects ≥100 MWh (no additions this issue; no weekend announcements) - China suppliers' overseas projects · Table A — 3 added this issue (Hithium Spain plant / Trina Italy 1 GWh / BYD Bulgaria 500 MWh backfill); now 19 entries - Supplier profiles · Table B — no updates this issue - Lithium price history · Table D — 06-01 row appended today (USD 23,114.22; SMM latest Date May 29, carried over the weekend closure, refreshed to June 1 data in the afternoon); trend chart redrawn

Full project supply-chain BOM in Living Table C.

No new project progress this issue (2026-05-31 to 06-01 weekend window)

Between 2026-05-31 (Sun) and 2026-06-01 (Mon morning), the major Australian BESS developers, AEMO and state governments issued no new announcements. The weekend is a normal pause window.

CIS Tender 8 (16 GWh dispatchable storage): entering the June announcement watch window

Results of CIS Tender 8 (opened by DCCEEW on 2025-11-28, bids closed 2026-02-06; target 4 GW / ~16 GWh, ≥4-hour duration, including the first-ever aggregation pathway: ≥5 MW within the same NEM region can aggregate to a ≥30 MW bid) are officially confirmed to be "announced in June 2026." As of today (June 1) they have not landed; this week is the key watch window. The announcement will directly reveal the next batch of standalone-storage contract recipients in the NEM — the most important pricing signal in the current pipeline.

→ For PG: once Tender 8 results land, PG should immediately check overlap between the winning projects' connection points and its own pipeline, and adjust its bidding strategy for Tender 10 (expected to open around the same June window) accordingly. The CIS Tender 10 (new round of dispatchable capacity) window opens with the Tender 8 announcement; the bid package needs 4-6 weeks of lead-time preparation.

NSW Prioritising Renewable Energy Bill 2026: energy minister granted fast-track powers, 50-business-day federal target · PV Tech / Norton Rose Fulbright, 2026-05-07

The NSW Parliament proposed the Prioritising Renewable Energy Act 2026 on 2026-05-07. Core content:

→ For PG: if the NSW fast-track grants "priority" status, the BESS project DA cycle compresses from 12-18 months to 3-6 months — materially significant for time-critical windows like CIS Tender 10 / NSW LTESA T9. Given PG has projects in development in NSW, it should confirm the "priority identification" application path and prerequisites (project stage, community-engagement document requirements) with Norton Rose Fulbright / Baker McKenzie.

Sources: PV Tech (2026-05-07) · Norton Rose Fulbright

CIS Tender 9 (5 GW generation, bids opened 2026-05-25) timeline countdown

Registration deadline: 2026-06-22 (in 21 days); bid deadline: 2026-07-20; results expected 2026-11. NSW cannot participate; VIC solar-only cap 470 MW (solar+storage hybrids not capped); First Nations Set Aside 500 MW dedicated quota (≥5% equity / benefit sharing); scoring weights: financial value 35% (was 50%), deliverability 20% (was 12.5%), organisational / financing capability 20% (was 12.5%), social value 25%.

→ For PG: with the June 22 registration window counting down, PG's prospective QLD / SA / VIC / TAS projects must complete feasibility assessment within this week and decide whether to register. Competition intensity in the First Nations 500 MW dedicated pool is markedly lower than in the main pool; if a project has a ≥5% Indigenous-partnership structure, it should prioritise that channel.

Australian projects in Living Table C; non-Australian projects in Living Table A; supplier profiles in Living Table B.

Hithium €400M battery Gigafactory in Navarra, Spain formally signed (dual-function plant: cell manufacturing + BESS system integration) · Energy-Storage.news, 2026-04-17

Hithium signed a formal investment-commitment agreement with the Navarra regional government, witnessed by Spanish PM Pedro Sánchez and the Navarra president:

The Hithium profile already in Table B (Spain plant entry) is confirmed in sync; its bankability dimension upgrades from "project delivery record" to "local fixed-asset investment."

→ For PG: once Hithium's local European plant is operational, its cells will gain markedly stronger supply-chain acceptance in European projects (bank due diligence, lender's engineer reports). If PG has European projects (or works with European financiers), Hithium becomes a more competitive alternative beyond CATL/BYD; if procuring in Australia, the European plant serves as additional "global supply-chain stability" backing.

Source: Energy-Storage.news (2026-04-17) · first logged 2026-06-01 (added to Table A)

Trina Storage × Aer Soléir Rondissone BESS in Italy (1 GWh / 250 MW, won via CRM auction) · Trinasolar EU, 2026-01-20

Trina Storage signed a contract with Irish developer Aer Soléir (backed by Invenergy) to build Italy's largest BESS project to date:

→ For PG: the Italian CRM auction win is direct evidence of Trina Storage securing a European government capacity contract — same family of mechanisms as the UK CM and Australian FERM/CIS. This contract further enriches Trina's government-contract track record within PG's Australian supply framework (signed 2025-11). Recommend PG ask Trina for a CRM contract summary as a bankability evidence document.

Sources: Trinasolar EU (2026-01-20) · ESS-News (2026-01-23) · first logged 2026-06-01 (added to Table A)

[Backfill] BYD Maritsa East 3 BESS in Bulgaria (500 MWh, largest in Eastern Europe) grid-connected · CNESA, 2026-01-08

BYD completed one of Europe's largest storage projects to date:

→ For PG: Chinese suppliers dominating the Eastern-European BESS market is now a fait accompli; both cases can be cited as supply evidence when PG negotiates with BYD. The BYD Bulgaria case predates CATL's but has lower media exposure — an underrated asset when PG demonstrates BYD's bankability to lenders.

Source: CNESA (2026-01-26) · first logged 2026-06-01 (added to Table A, backfill)

Watchlist activity this issue (2026-05-31 / 06-01 window)

Within the 2026-05-31 (Sun) to 2026-06-01 (Mon morning) search window, the ten watchlist suppliers (CATL / BYD / EVE / Hithium / Envision / Sungrow / Trina / REPT / CORNEX / HyperStrong) disclosed no new overseas projects or order announcements (≥100 MWh threshold).

Today's price (basis: collected 2026-06-01 07:31 Beijing time)

| Grade | Latest | Basis |

|---|---|---|

| Battery-grade lithium carbonate (SMM) | USD 23,114.22 / tonne (0, 0.0%) / CNY 178,069 / tonne | SMM homepage SMM-Li-LC-001 Avg; SMM latest Date May 29 (weekend closure, the 7:31 capture being T-3 is normal; will refresh to June 1 data in the afternoon); CNY = 23,114.22 × 6.8176 × 1.13 |

Trend analysis

New mine-side disturbance (important): Greenbushes, the world's largest lithium mine, cuts production guidance; Benchmark estimates ~170 kt SC less supply in H1

IGO / Greenbushes (the world's largest spodumene mine, in Western Australia, ~20% of global capacity) released its quarterly report on 2026-04-23, cutting FY2026 concentrate production guidance from ~1.50-1.70 Mt (dry metric tonnes) to ~1.38-1.43 Mt, a drop of ~8-9%. Core reasons: ore-grade decline faster than expected, plus systemic operational issues. IGO shares fell another 6.3% on May 21, with the market questioning the persistence of the operational issues.

Benchmark Mineral Intelligence (2026-04-28) assesses that this Greenbushes cut means global spodumene supply in H1 2026 will be ~170 kt SC (spodumene concentrate) lower than previously expected — a third supply-side constraint on top of the already-reported Zimbabwe export ban + Jiangxi licence renewals. The direction is opposite to the three-mine restart (MinRes Bald Hill + Pilbara Ngungaju in July, Core Lithium Finniss in Q4) — the two sets of signals stacking together materially raise uncertainty over the Q3 physical-balance timing.

Sources: IGO ASX quarterly (2026-04-23) · Benchmark MI (2026-04-28)

GFEX tightens lithium carbonate futures position limits (2026-05-28)

The Guangzhou Futures Exchange announced rule changes on May 28: from contract LC2610, when single-side positions are below 60,000 lots, the non-hedging-account cap narrows from 10% of open interest to 3,000 lots; above 60,000 lots the cap drops from 10% to 5%. Industrial hedging accounts are unaffected. The market read the policy as regulators proactively deleveraging during the rapid price spike — one of the institutional catalysts behind the consecutive pullbacks after spot prices neared a two-year high on May 13 (CNY ~200,500/tonne).

Analysis: GFEX position limits + Goldman Sachs's "H1 2026 top" call + InfoLink's weak downstream willingness at high prices together explain the price-pullback mechanism since mid-May; but the Greenbushes cut + uncertain three-mine restart cadence + UBS supply downgrade mean the claim "pullback = trend reversal" still does not hold.

Source: China Securities Journal (2026-05-28)

Demand side: China's June cell production schedule projected at 268 GWh (+7.6% MoM), 500+ Ah large cells penetrating fast

TD (Tiandong Times think tank) forecast on May 26 that China's total June lithium-battery production schedule (storage + power + consumer) is ~268 GWh (+7.6% MoM), a fourth consecutive monthly record high; global ~281 GWh (+7.3%). Structural highlight: storage cells make up 41.4%, surpassing power cells as the largest scenario for the first time. Meanwhile, 500+ Ah large cells (EVE 628 Ah + CATL 587 Ah) had ~5% Q1 penetration, expected to approach 20% by year-end, driving material-supply-disruption risk on legacy-spec (314 Ah) lines. The flip side of the production surge: upstream cathode-material supply is tight, and pricing power is being redistributed back upstream.

Source: Eastmoney (2026-05-26)

Institutional view: UBS raises 2026 China lithium-price forecast by 18%

UBS (2026-05-07/08 research note) raised its 2026 China lithium carbonate spot-average forecast by 18% to CNY 200,000/tonne, expecting a short-term high of 250,000/tonne in May-June; core driver: storage-battery demand +60% YoY. GS over the same period maintains its H1 2026 top + 2026H2-2028 decline path (USD 10,100-16,000); the two still differ structurally on the H2 outlook. Benchmark MI (2026-06-25 webinar preview) will publish for the first time a lithium forward curve + price risk monitoring (VaR) tool, which may provide a new quantitative anchor.

Source: Moomoo / UBS (2026-05-07/08)

→ For PG: the Greenbushes cut is the heaviest new supply-side information this issue, breaking the one-way narrative that "with only the three-mine restart, supply must loosen." The UBS forecast upgrade + the GFEX-limit-driven pullback stacking together mean the Q3 physical price range (USD 20,000-25,000) may be wider than GS expects. PG's procurement-framework price-lock timing is still best set "after Bald Hill's first July production data lands," but it must concurrently monitor the Q2-report progress of the Greenbushes operational issues (expected late July).

Source: full ledger in Living Table D

LG Energy Solution × DTE Energy US$1.6bn ESS contract: AI data centers directly pulling grid-scale BESS procurement · Korea Herald, 2026-05-28

LG Energy Solution signed a 6 GWh / ~US$1.6bn ESS cell-supply contract (2-year term) with DTE Energy, Michigan's largest utility — the most complete commercial case yet of the "AI data center → utility → large-scale BESS procurement" chain:

→ For PG: the DTE model — "a utility steps in to procure BESS → allocates it across multiple projects → including data centers" — provides a reference blueprint for similar structures in Australia. AEMO's data-center (3.2 GW by 2030) mandatory-storage policy will get an AEMC proposal in July, at which point Australia may see similar large consolidated-procurement demand. PG can proactively approach utilities like AusNet / TransGrid to explore an aggregated-development path of "DNSP or NSP centralized BESS procurement serving multiple data-center customers."

Source: Korea Herald (2026-05-28)

Greenpeace Australia Energy Vampires report: data centers may take 13% of Australia's electricity by 2040, calls for an approval moratorium · Greenpeace Australia, 2026-05-27

Greenpeace Australia Pacific released a report citing AEMO data: by 2040, data centers may account for 13% of Australia's total national electricity use. Core demands: (1) existing data-center operators cannot substantively prove their "additionality" claims of new renewables; (2) Australia is already seeing data-center-driven gas expansion (a single project could wipe out all of NSW's 2028 emissions reductions); (3) it calls for an immediate moratorium on data-center development until safeguard legislation is complete.

Greenpeace's position runs opposite to AEMC / DCCEEW (data centers must include storage, July proposal), and may create approval headwinds for data-center + companion renewable projects at the level of public opinion.

→ For PG: the regulatory and public-opinion environment for Australia's data-center storage market is growing more complex. If the moratorium demand triggers regulatory tightening, it may slow some AIDC developments; but if the government only tightens "green-power additionality requirements" (rather than halting development), BESS storage demand becomes even more rigid. In project proposals involving data-center scenarios, PG must clearly provide a "new-renewables authenticity" proof path (e.g. dedicated PPA + timestamp matching) to meet compliance requirements that may land in future.

Source: Greenpeace Australia (2026-05-27)

No additions today

Within the 2026-05-31 to 06-01 window, no new announcements landed on GFM, cell specs, or system-design direction (already reported: CATL ESVL test base + Sungrow GFM TÜV dual certification + Trina Elementa 3).

No additions today

For this issue's window (2026-05-31 ~ 06-01), the Modo Australia-related article search: no newly published articles. The two most recent (Frances Hallen "NEM solar capture rates" [source_id:23434] and Tom Derrick "NEM market outlook Q2 2026" [source_id:23436], both published 2026-05-29) were fully covered in the 2026-05-29 brief.

None this issue

This brief is auto-compiled daily by the PGSH internal research system, with each item's source cited individually. The listed project progress, policy developments, price data and institutional views are for internal reference only and do not constitute investment, procurement or business-decision advice. If you are interested in any item or intend to act on it, please open the corresponding source link directly to verify the accuracy and timeliness of the information.